UK Real Estate Market 2026–2040

Full Analytical Report with Forecasts for 2, 5, 10, and 15 Years

The article was prepared by Serhii Kryvoviaz, Head of the Analytical and Marketing Department

Executive Summary

The UK property market in 2026 is entering a transitional cycle shaped by interest rate volatility, inflationary pressures, structural housing shortages, demographic shifts, and climate-related risks. Market data from major consultancies suggests modest short-term growth followed by stronger medium-term appreciation.

For example, Savills expects UK house prices to grow by roughly 2% in 2026 and nearly 25% cumulatively by 2030, indicating moderate short-term stability followed by long-term expansion.

Meanwhile, the Office for Budget Responsibility projects average house price growth of approximately 2.5% annually between 2025 and 2030, reinforcing expectations of gradual appreciation rather than rapid inflation.

However, macroeconomic uncertainty remains elevated. Recent economic developments — including rising mortgage rates above 5% and downgraded GDP forecasts — are already affecting affordability and buyer activity.

This report provides:

- Full analysis of the current UK real estate market

- Residential and commercial sector breakdown

- Regional performance outlook

- Investment strategy recommendations

- Forecasts for 2, 5, 10 and 15 years

- Risk assessment and scenario modelling

1. The Current State of the UK Property Market (2026)

The UK housing market in 2026 reflects a period of recalibration after rapid growth during the pandemic and subsequent interest rate tightening. Demand remains resilient but constrained by affordability challenges, especially for first-time buyers.

Recent forecasts suggest house price growth will remain modest in the short term. Savills expects approximately 2% growth in 2026, following weaker momentum in 2025.

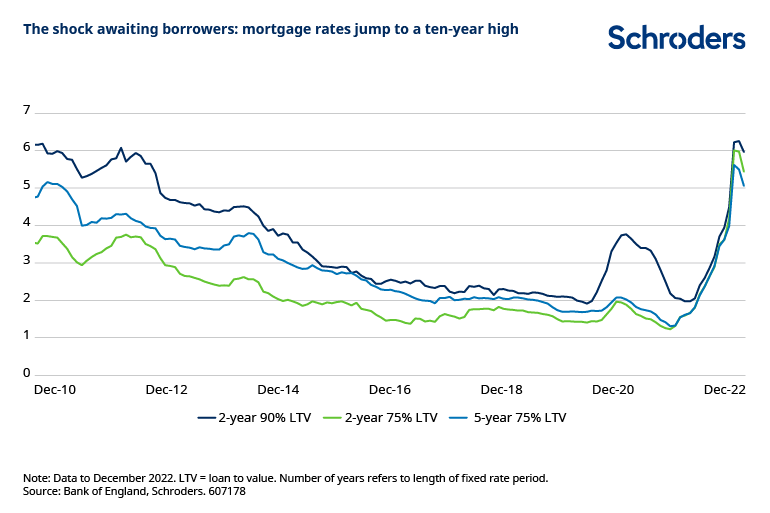

Additionally, market sentiment has been affected by rising borrowing costs. Mortgage rates climbed above 5% in early 2026, significantly reducing purchasing power for households and increasing monthly repayment burdens.

At the same time, economic growth expectations have weakened. The OECD downgraded UK GDP growth for 2026 to 0.7%, highlighting slowing investment and consumer demand.

These conditions create a “soft landing” environment — characterized by limited price growth, lower transaction volumes, and cautious investor activity.

Key Market Indicators (2026)

| Indicator | Value | Trend |

|---|---|---|

| Average house price growth | ~2% | Stable |

| Mortgage rates | 5%+ | Rising |

| GDP growth forecast | 0.7% | Slowing |

| Inflation | ~4% expected | Rising |

| Demand | Moderate | Cooling |

Sources: Savills, OECD, Bank of England, Nationwide

2. Structural Drivers of the UK Housing Market

Despite short-term headwinds, the UK property market remains fundamentally supported by structural factors:

2.1 Housing Supply Shortage

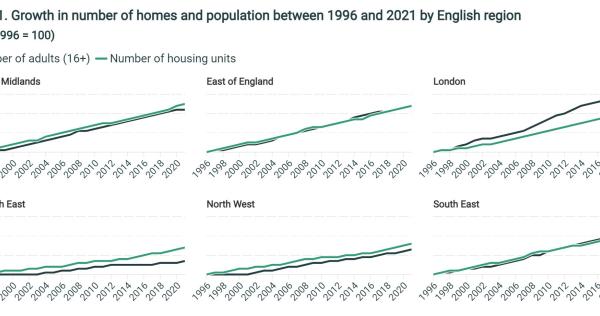

The UK continues to face a chronic undersupply of housing. Planning reforms are expected to increase housebuilding by approximately 170,000 homes by 2029–30, slightly boosting the housing stock.

However, this increase remains insufficient relative to population growth and household formation.

2.2 Population Growth and Migration

Population expansion — driven by immigration and demographic changes — continues to increase housing demand, particularly in:

- London

- South East England

- Manchester

- Birmingham

- Leeds

These urban centers are expected to outperform national averages over the long term.

2.3 Rental Market Pressure

Rental costs continue to rise due to:

- Landlord exits

- Regulation changes

- Higher financing costs

- Limited housing supply

This trend supports investment demand for buy-to-let assets.

3. Regional Market Performance

The UK property market is increasingly fragmented geographically.

London

London has underperformed in recent years due to affordability constraints. Prices fell by 1.8% in 2025, but forecasts suggest recovery from 2027 onward.

Knight Frank estimates cumulative London growth of 13.6% between 2026 and 2030.

Northern England and Midlands

Northern regions are forecast to outperform, with projected growth of 20–25% over five years according to Savills projections.

These regions benefit from:

- Lower entry prices

- Infrastructure investment

- Urban regeneration

- Remote work migration

Scotland and Wales

Both markets are expected to see strong growth due to affordability advantages and regional economic development.

Savills forecasts overall UK price growth of around 22% over five years, with northern England, Wales and Scotland leading performance.

4. Mortgage Market and Interest Rates

Interest rates remain the single most important driver of short-term housing performance.

Recent data shows:

- Mortgage rates above 5%

- Reduced availability of low-cost lending

- Withdrawal of hundreds of mortgage products

These developments reduce buyer affordability and slow transaction activity.

However, market expectations suggest rate stabilization over the medium term, supporting recovery.

5. Investment Sentiment

Investor activity in 2026 is characterized by:

- Shift from capital growth to yield focus

- Increased interest in regional cities

- Institutional investment in build-to-rent

- Growth in ESG property strategies

Rental demand remains strong, supporting long-term investment fundamentals.

6. Risk Factors Impacting the Market

Key risks include:

Economic Risks

- Inflation persistence

- Slow GDP growth

- Interest rate volatility

Climate Risks

Flooding could impact up to 430,000 UK households by 2050, potentially reducing property values in high-risk areas by over 20%.

Policy Risks

- Planning regulation changes

- Taxation reforms

- Rental market legislation

7. UK Property Price Forecast (Short-Term View)

Consultancies expect moderate growth:

| Year | Forecast Growth |

|---|---|

| 2026 | ~2% |

| 2027 | ~4% |

| 2028 | ~5% |

| 2029 | ~5.5% |

| 2030 | ~4% |

These projections imply cumulative growth of over 22% within five years.

Market Trend Summary

Short-term outlook:

- Stable prices

- Lower transaction volume

- Gradual recovery

Medium-term outlook:

- Growth acceleration

- Regional divergence

- Investor demand increase

The UK real estate market in 2026 is transitioning from a high-growth cycle to a stabilization phase. While affordability constraints and economic uncertainty limit short-term price growth, structural housing shortages, demographic demand, and investment inflows support long-term appreciation.

8. Residential Property Market Analysis

The residential sector remains the backbone of the UK real estate market, accounting for the majority of transactions and investment activity. Despite rising mortgage rates, demand for housing continues to be supported by structural undersupply and population growth.

According to data from Office for National Statistics, the average UK house price increased modestly in early 2026 following a slowdown in 2025, reflecting stabilization rather than rapid expansion. The agency reports that price growth varies significantly by region, with northern England outperforming London due to affordability dynamics.

Key Drivers of Residential Demand

- Population growth and net migration

- Supply constraints

- Wage growth in regional cities

- Remote work trends

- Rental affordability pressures

Mortgage affordability remains a limiting factor. Data from Bank of England shows that average mortgage repayments as a share of income are near their highest levels since 2008, reducing purchasing power for first-time buyers.

Residential Price Trends (2020–2026)

Between 2020 and 2022, UK house prices surged due to ultra-low interest rates and pandemic-driven demand. The market cooled in 2023–2025 as rates increased, followed by stabilization in 2026.

Average UK House Price Growth

| Year | Average Price Growth |

|---|---|

| 2020 | 7.4% |

| 2021 | 10.8% |

| 2022 | 8.6% |

| 2023 | 1.2% |

| 2024 | -0.5% |

| 2025 | 0.8% |

| 2026 | 2.0% (forecast) |

Sources: ONS, Nationwide, Halifax

9. Rental Market Analysis

The UK rental market is experiencing one of the strongest demand periods in decades. Limited supply, landlord exits, and increased immigration are pushing rents upward.

According to Rightmove, average UK rents increased by approximately 8–10% year-on-year in many regions during 2025–2026.

Meanwhile, data from Zoopla shows that rental demand continues to exceed supply by nearly two to one, especially in major cities.

Rental Growth by Region (2026)

| Region | Annual Rent Growth |

|---|---|

| London | 7% |

| North West | 9% |

| Yorkshire | 10% |

| Midlands | 8% |

| Scotland | 9% |

| Wales | 8% |

This strong rental performance supports buy-to-let investment strategies, particularly in regional markets.

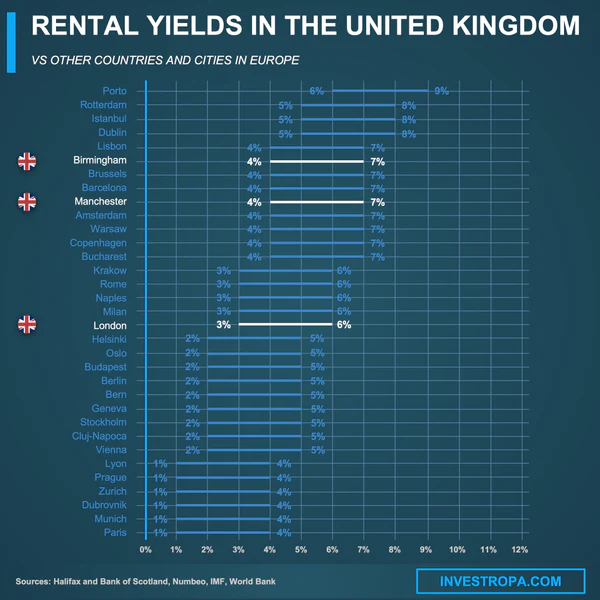

10. Buy-to-Let Investment Yields

Rental yield remains a key metric for investors. While capital growth has slowed, rental income has improved.

Average gross rental yields (2026):

| Region | Yield |

|---|---|

| London | 4.5% |

| Manchester | 6.5% |

| Birmingham | 6.2% |

| Liverpool | 7.2% |

| Leeds | 6.4% |

| Glasgow | 6.8% |

Regional cities offer significantly higher yields compared to London, explaining the shift in investor focus.

11. Commercial Real Estate Market

The UK commercial property sector is undergoing structural transformation, driven by hybrid working, e-commerce growth, and logistics demand.

Three segments dominate:

- Office

- Retail

- Industrial / Logistics

Office Market

Office demand has changed significantly following remote work adoption. Central London prime offices remain resilient, while secondary office space faces declining demand.

Research from CBRE indicates that Grade A office space in London continues to attract tenants, particularly ESG-compliant buildings.

Trends include:

- Downsizing of office footprints

- Demand for flexible workspace

- Premium for sustainable buildings

- Vacancy increase in secondary offices

Retail Property Market

Retail continues to recover after pandemic-driven declines. However, structural changes toward online shopping limit growth.

Shopping centres and high streets are being repurposed into:

- Residential units

- Mixed-use developments

- Leisure and hospitality spaces

Industrial and Logistics

This segment remains the strongest performing commercial sector. Growth is driven by:

- E-commerce expansion

- Supply chain restructuring

- Urban logistics demand

Prime logistics rents increased significantly between 2021 and 2025 and continue to grow moderately.

Commercial Property Performance Comparison

| Sector | Outlook | Risk Level |

|---|---|---|

| Logistics | Strong | Low |

| Residential | Strong | Low |

| Offices | Mixed | Medium |

| Retail | Weak/Stable | High |

12. Build-to-Rent Sector

Institutional investment in Build-to-Rent (BTR) is accelerating. Pension funds and asset managers increasingly view rental housing as a stable income asset.

Drivers:

- Rising rental demand

- Institutional capital inflow

- Long-term income stability

- Professional property management

The BTR sector is expected to expand significantly by 2030.

13. Regional Investment Hotspots

Top-performing cities for investment:

Manchester

- Strong population growth

- Infrastructure investment

- High rental yields

Birmingham

- HS2 development

- Corporate relocations

- Growing financial sector

Leeds

- Financial services hub

- Affordable entry prices

Liverpool

- High yields

- Regeneration projects

Glasgow

- Strong rental demand

- Limited supply

UK Regional Investment Comparison

These regional markets are expected to outperform London in percentage growth over the next decade.

14. Housing Supply vs Demand

The UK continues to build fewer homes than required.

Estimated demand: ~300,000 homes per year

Actual construction: ~200,000–230,000 homes per year

This structural gap supports long-term price growth.

15. Affordability Analysis

Affordability remains stretched:

- House price to income ratio: ~8.3x

- London ratio: ~11x

- Mortgage costs: ~35–40% of income

These factors limit short-term growth but increase rental demand.

UK Real Estate Market 2026–2040

Macroeconomic Drivers & 2-Year Forecast (2026–2028)

16. Macroeconomic Environment Shaping the UK Property Market

The performance of the UK real estate market is closely tied to macroeconomic indicators such as inflation, interest rates, wage growth, employment, and GDP. In 2026, these factors collectively indicate a transitional period with moderate risk and gradual recovery.

The UK economy is experiencing slower growth compared to the post-pandemic rebound. Data from Office for Budget Responsibility suggests that economic growth will remain subdued in the near term before strengthening toward the end of the decade.

Key Macroeconomic Indicators (2026)

| Indicator | Forecast | Impact on Property |

|---|---|---|

| GDP Growth | 0.7–1.0% | Weak demand |

| Inflation | 3.5–4.0% | Pressure on affordability |

| Interest Rate | 4.5–5.25% | Mortgage cost increase |

| Wage Growth | 3–4% | Partial support |

| Unemployment | ~4.5% | Stable |

These indicators suggest that while affordability remains constrained, economic stability reduces the risk of a major property market correction.

17. Inflation and Housing Market Relationship

Inflation plays a dual role in real estate:

Positive effects:

- Asset price protection

- Rental growth

- Construction cost increases

Negative effects:

- Higher interest rates

- Reduced affordability

- Lower transaction volumes

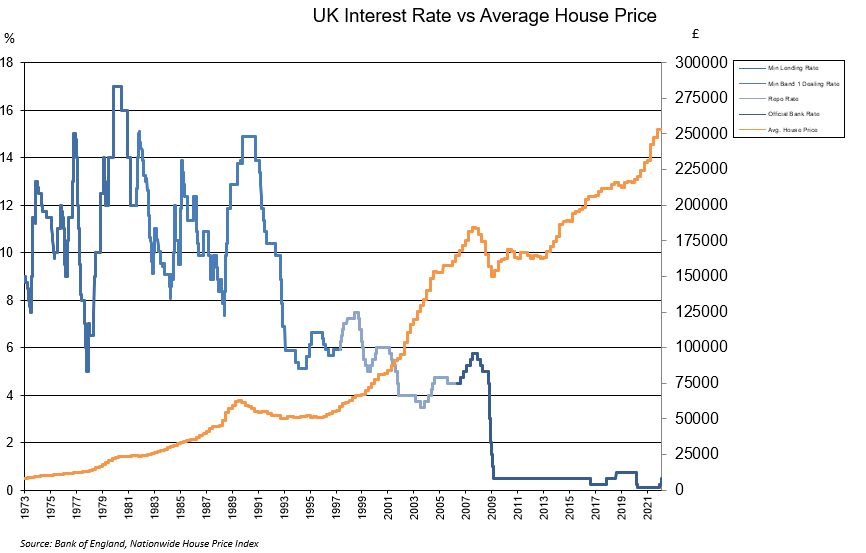

The UK inflation rate peaked above 10% in 2022 and has gradually declined. However, persistent inflation keeps interest rates elevated, affecting borrowing capacity.

Interest Rate vs House Price Relationship

Historically, rising interest rates slow property price growth rather than causing large declines, especially when supply shortages exist.

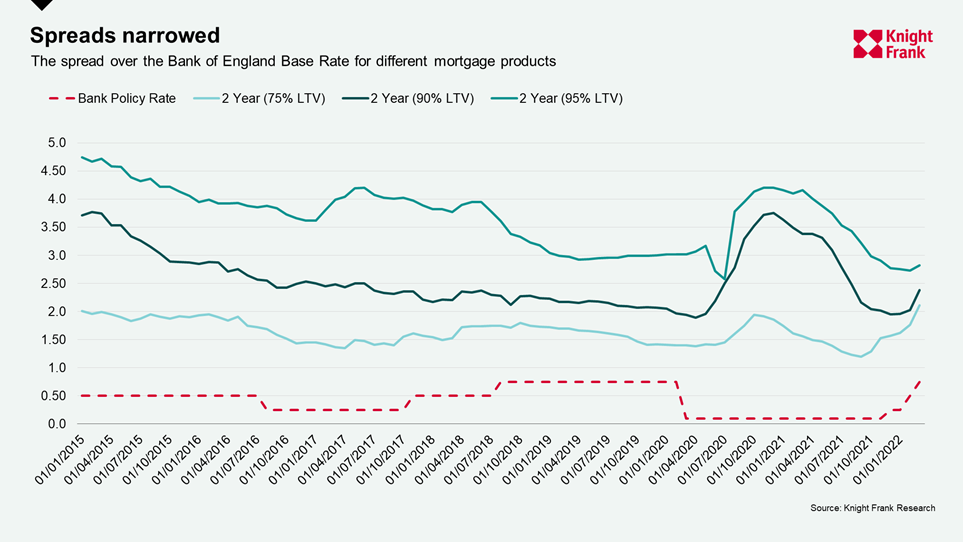

18. Bank of England Monetary Policy Outlook

The Bank of England remains focused on controlling inflation. The base rate increased significantly between 2022 and 2024 and remains relatively high in 2026.

Expected rate trajectory:

| Year | Expected Base Rate |

|---|---|

| 2026 | 4.75% |

| 2027 | 4.25% |

| 2028 | 3.75% |

Gradual rate reductions are expected to improve affordability and stimulate demand.

19. Wage Growth and Affordability

Wage growth remains moderate but insufficient to fully offset high house prices.

Average UK salary growth:

- 2024: 5.2%

- 2025: 4.1%

- 2026 forecast: 3.8%

This creates a gradual improvement in affordability over time.

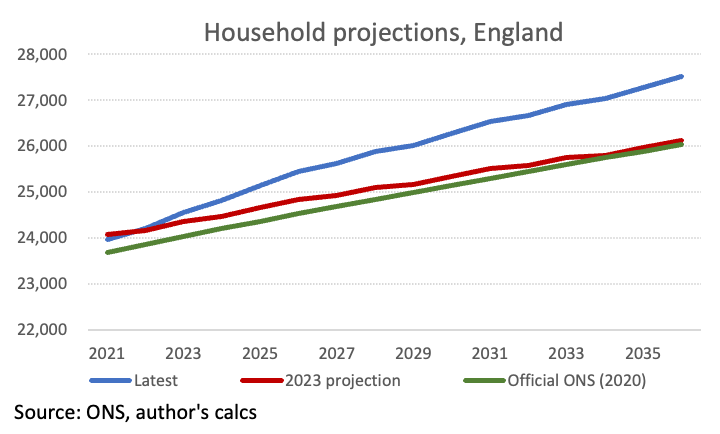

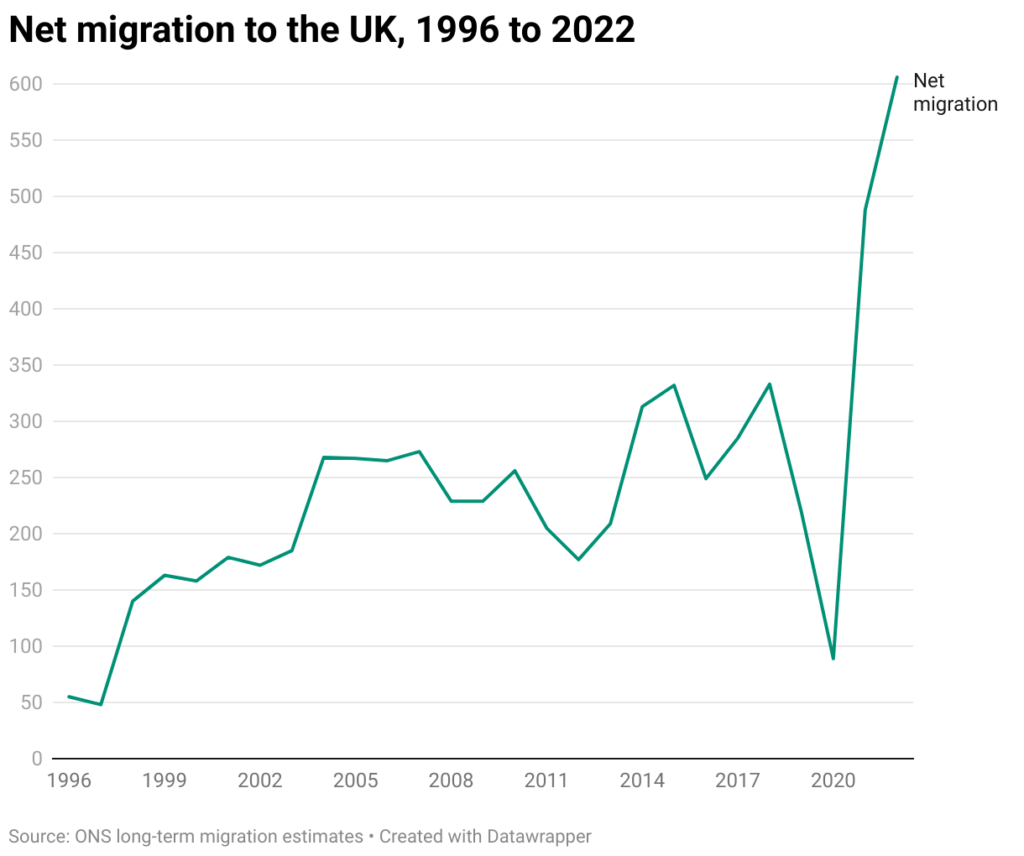

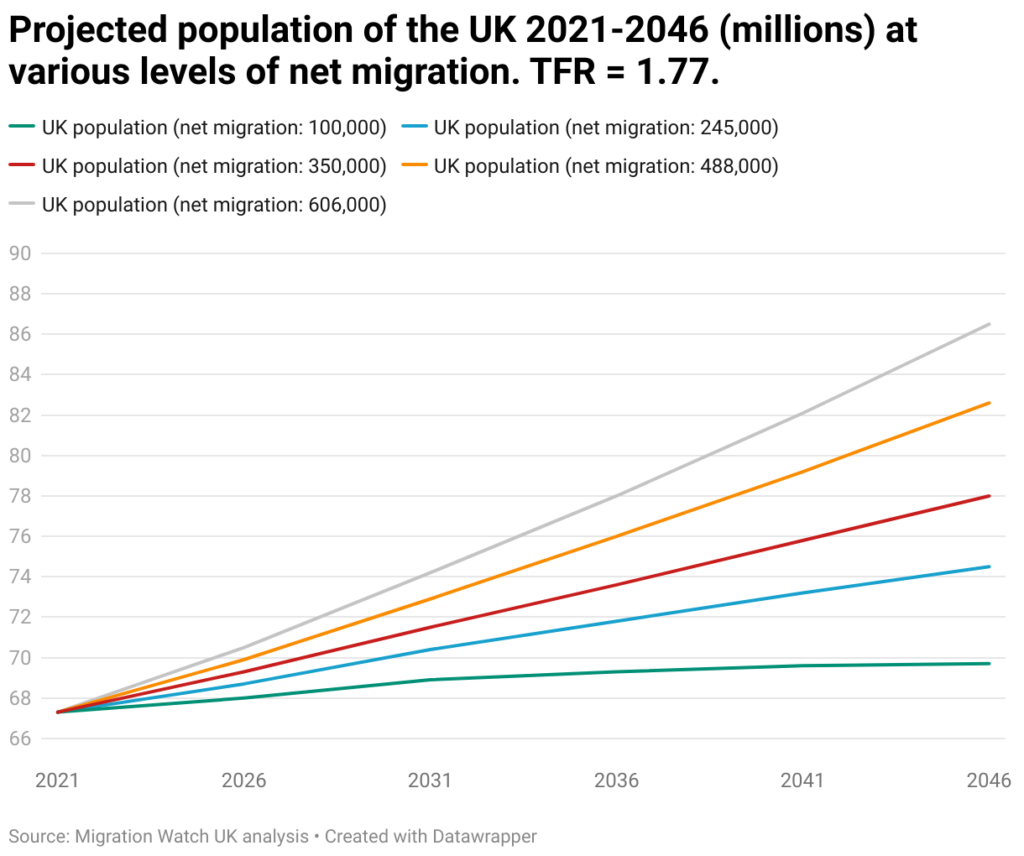

20. Demographic Trends Driving Housing Demand

Population growth is a major long-term driver of housing demand. The UK population continues to expand due to:

- Net migration

- Household formation

- Urbanization

The UK population is projected to exceed 72 million by 2035.

Population Growth vs Housing Supply

Demand continues to outpace new construction, supporting price growth.

21. Migration Impact on Housing Market

Net migration remains high, particularly in:

- London

- South East

- Manchester

- Birmingham

Migration increases demand for:

- Rental properties

- Affordable housing

- Urban apartments

This trend supports both rental growth and long-term capital appreciation.

22. Construction Costs and Housing Supply

Construction costs increased significantly due to:

- Labour shortages

- Material inflation

- Energy costs

- Planning delays

These factors limit new housing supply and support existing property values.

23. Mortgage Market Trends

Mortgage lending volumes declined during 2023–2025 but are stabilizing in 2026.

Key trends:

- Fixed-rate mortgages dominate

- Longer-term mortgages increasing

- First-time buyer activity constrained

- Cash buyers increasing share

These developments support gradual market recovery.

24. 2-Year Property Market Forecast (2026–2028)

Short-term outlook reflects moderate growth with improving conditions.

Forecast Assumptions

- Interest rates gradually decline

- Inflation stabilizes

- Wage growth improves

- Supply remains limited

UK House Price Forecast 2026–2028

| Year | Growth Forecast | Market Condition |

|---|---|---|

| 2026 | 2% | Stabilization |

| 2027 | 3.5–4% | Recovery |

| 2028 | 4.5–5% | Expansion |

Cumulative growth (2 years): approx. 7–9%

Regional Growth Forecast (2026–2028)

| Region | Expected Growth |

|---|---|

| London | 5% |

| South East | 6% |

| Midlands | 8% |

| North West | 9% |

| Scotland | 8% |

| Wales | 7% |

Regional cities are expected to outperform London in percentage growth.

25. Rental Market Forecast (2 Years)

Rental demand is expected to remain strong due to:

- Limited housing supply

- Affordability constraints

- Migration

Rental growth forecast:

| Year | Rent Growth |

|---|---|

| 2026 | 7% |

| 2027 | 6% |

| 2028 | 5% |

This supports buy-to-let investment strategies.

26. Investment Outlook (Short-Term)

Best-performing segments (2026–2028):

- Regional residential property

- Build-to-rent developments

- Logistics real estate

- Student accommodation

- Co-living developments

27. Risk Scenario Analysis (2-Year)

Base Scenario

- Moderate growth

- Stable demand

- Gradual recovery

Optimistic Scenario

- Faster rate cuts

- Strong wage growth

- 10% price growth over 2 years

Pessimistic Scenario

- Persistent inflation

- Rate increases

- Flat prices

5-Year Forecast, Investment Strategy, Regional Outlook & Commercial Real Estate (2026–2031)

28. The 5-year UK property market outlook

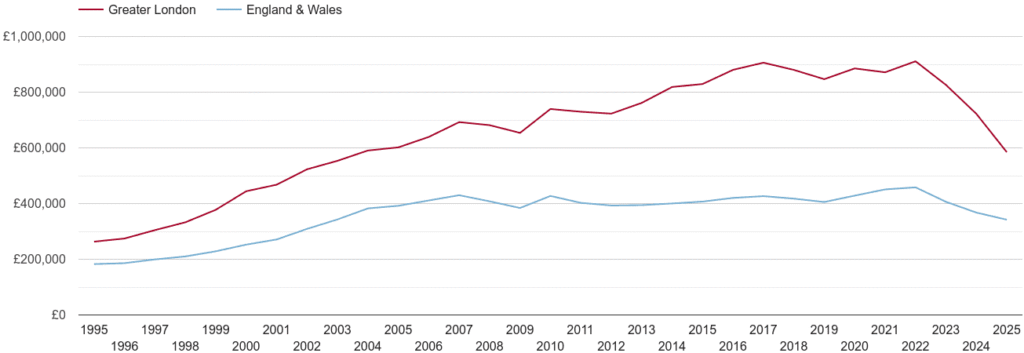

Over the next five years, the UK property market looks more like a recovery-and-normalisation story than a boom cycle. The most credible central case is modest near-term growth, followed by firmer gains as borrowing conditions ease and the structural undersupply of housing reasserts itself. The OBR expects the average UK house price to rise from about £260,000 in 2024 to just under £305,000 in 2030, with house prices growing by just under 3% in 2025 and then averaging about 2.5% a year from 2026.

That official view is broadly consistent with private-sector research, though broker forecasts tend to be a little more bullish on the medium term. Savills’ 2026–2030 mainstream residential outlook positions 2026 as a softer year before a stronger later-period recovery, while CBRE says house price growth should slow in 2026 because of stock levels and mortgage-rate uncertainty, then strengthen across the remaining forecast period as the economy improves and undersupply continues.

29. Base-case forecast for 2026–2031

For a practical planning framework for Audit Consulting Group readers, the most sensible base case is:

| Year | Base-case UK house price growth | Main market driver |

|---|---|---|

| 2026 | 1.5%–2.5% | affordability still tight |

| 2027 | 2.5%–3.5% | gradual rate relief |

| 2028 | 3.0%–4.0% | stronger transactions |

| 2029 | 3.0%–4.0% | supply-demand imbalance |

| 2030 | 2.5%–3.5% | mature expansion phase |

| 2031 | 2.5%–4.0% | wage growth + limited stock |

This range is an inference built from the OBR’s official medium-term forecast, the Bank of England rate backdrop, and CBRE/Savills commentary on improving affordability and persistent undersupply. It implies cumulative nominal growth over five years that is meaningful, but still well below the ultra-fast appreciation seen in 2020–2022.

30. Why the next five years should be firmer than 2025–2026

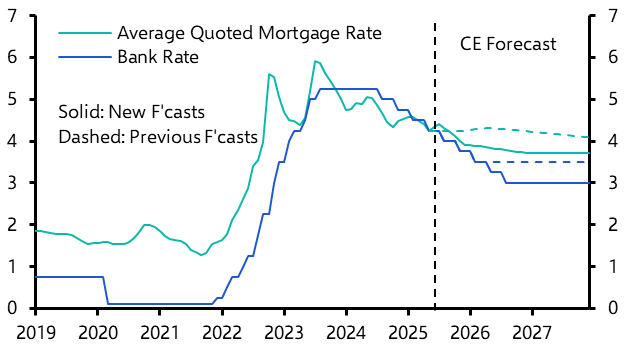

Three forces support the medium-term case. First, the Bank of England held Bank Rate at 3.75% in February 2026, with four MPC members voting for a cut, which signals that policy is no longer on a tightening path and that the next leg is more likely to be easing than further restriction. Second, OBR expects residential investment growth to accelerate to around 7% in 2027 and 2028 as monetary policy loosens and planning reforms take effect. Third, even with some improvement in construction, the UK’s stock shortfall remains too large to remove pricing pressure.

A useful near-term reality check is mortgage activity. Bank of England data for January 2026 shows net mortgage approvals for house purchases at 60,000, below the previous six-month average of about 64,100, while the effective rate on newly drawn mortgages was 4.09%. That says the market is functioning, but still below full strength.

31. 5-year transactions outlook

The transactions story matters as much as prices. OBR expects residential property transactions to rise from just under 1.1 million in 2024 to around 1.3 million in 2029. That is important because a market can deliver decent price growth with weak liquidity, but healthier transaction volumes usually signal broader confidence, better mortgage access and more reliable valuation conditions.

For advisers, developers and investors, this suggests that 2026 is more likely to be a positioning year than an exit year. Acquisition opportunities should remain better in the near term than they will be once transaction momentum improves more materially in 2027–2029. This is an inference from the combination of subdued approvals now and the OBR’s rising medium-term transactions path.

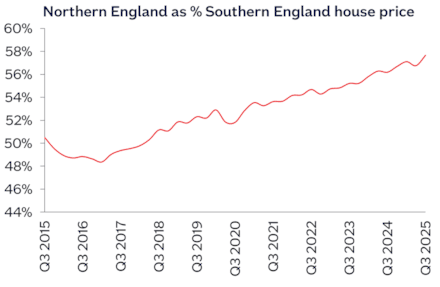

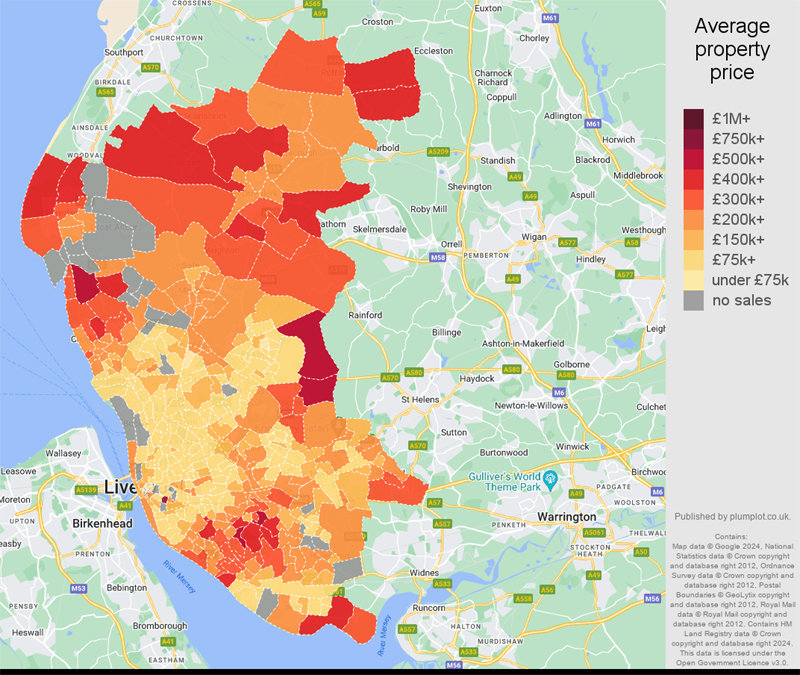

32. Regional price projections: who should outperform?

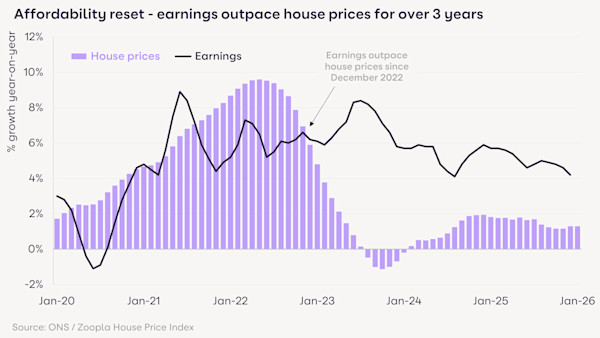

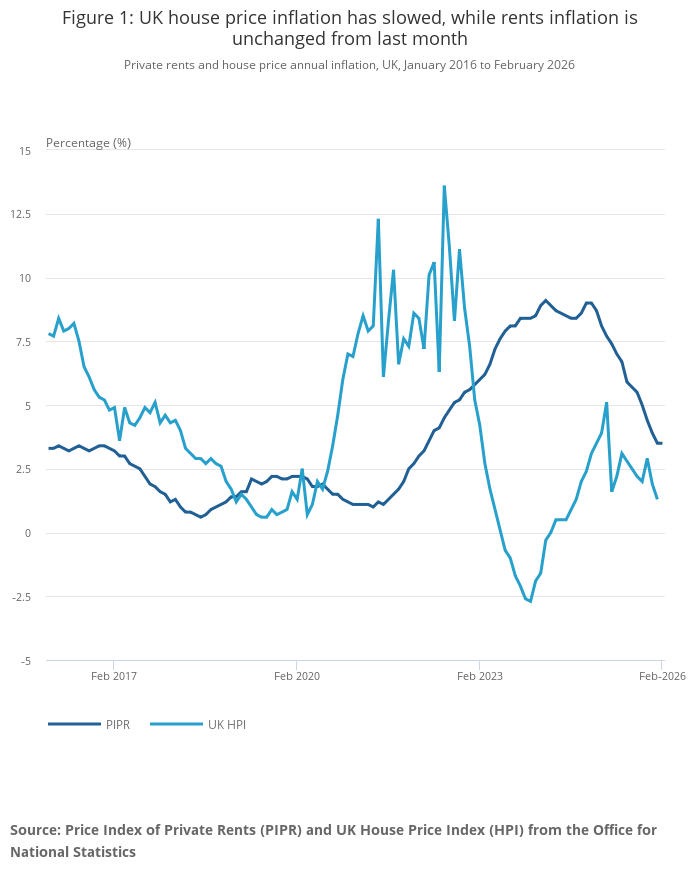

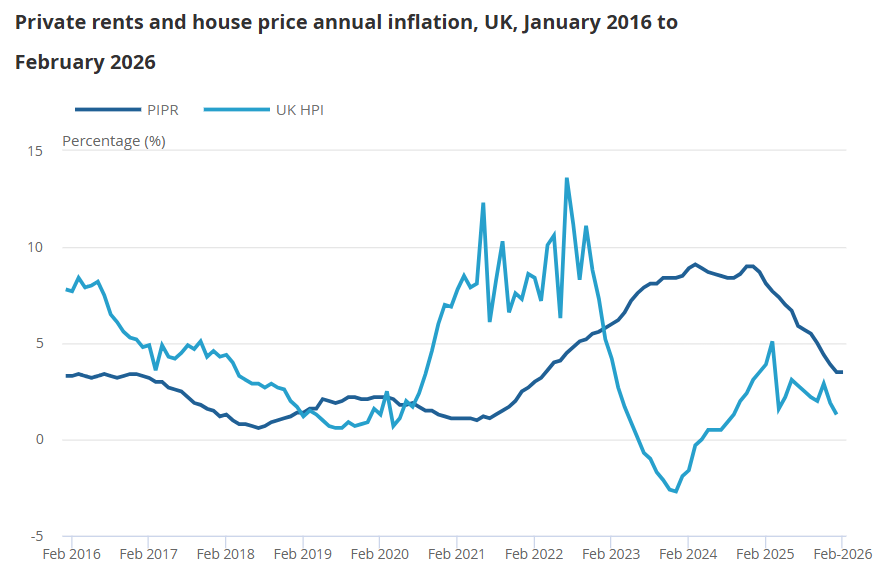

The regional hierarchy is likely to remain familiar: London may recover, but percentage growth is more likely to be stronger in relatively affordable cities and regions. ONS data for March 2026 shows that London was still the weakest part of the UK by annual house price inflation, with prices down 1.7% in the 12 months to January 2026, marking the sixth consecutive month of annual decline. By contrast, Wales and Scotland were still posting positive annual growth in the latest official release.

That does not make London unattractive. It means London is starting from a softer base. Prime-market commentary from Savills says 2026 should be a year of greater stability followed by a gradual recovery across prime markets, after prime central London values fell 4.8% in 2025.

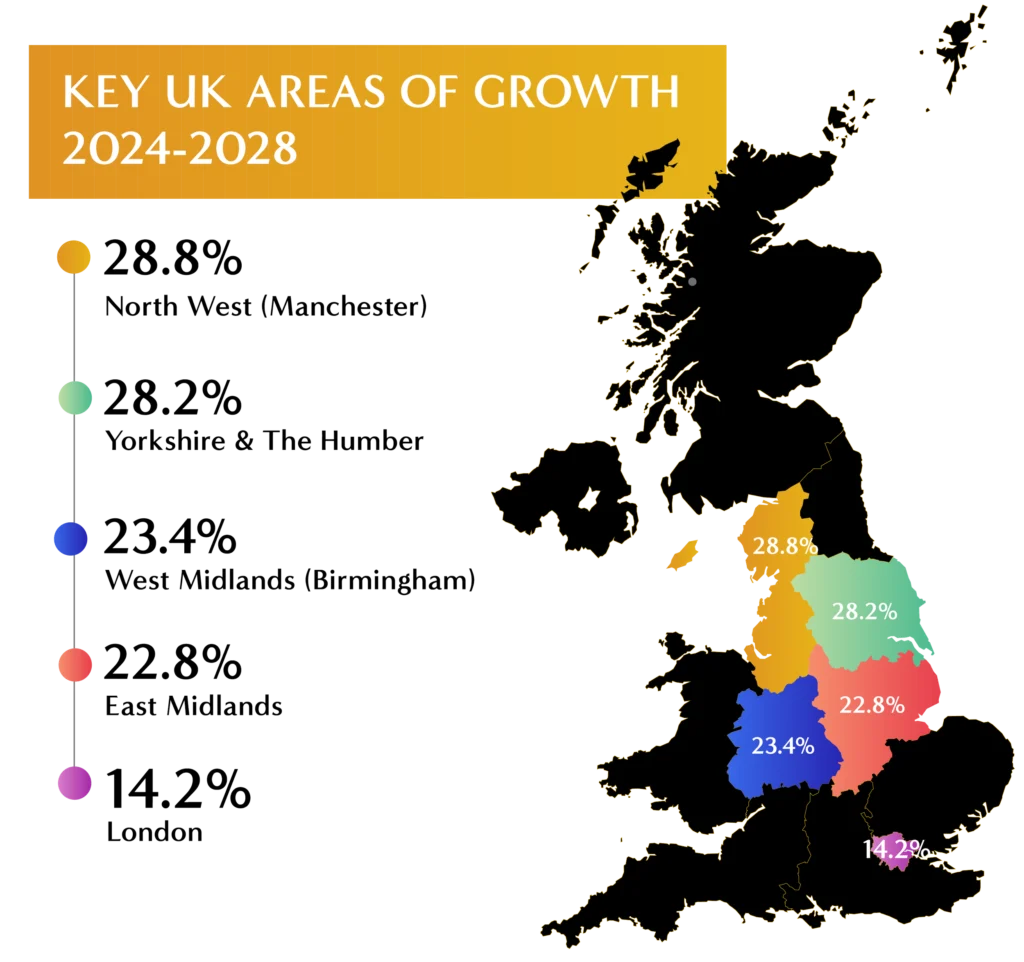

A reasonable five-year regional base case is:

| Region / market | 2026–2031 base view | Commentary |

|---|---|---|

| London | Moderate recovery | weaker starting point, global capital support |

| South East | Moderate | affordability still a constraint |

| North West | Strong | yield + affordability + urban demand |

| West Midlands | Strong | regeneration and business relocation |

| Yorkshire & Humber | Strong | lower entry pricing, rental resilience |

| Scotland | Moderate to strong | relative affordability |

| Wales | Moderate to strong | better value base, positive rent growth |

This ranking is consistent with the latest ONS regional pricing patterns, ONS rent data showing stronger rental inflation in some regions than in London, and CBRE/Savills emphasis on supply constraints and stronger value in regional markets.

33. Rental outlook through 2031

The rental market remains one of the strongest pillars under UK real estate. Official ONS data shows the average UK private rent reached £1,374 per month in February 2026, up 3.5% year on year. England’s average rent was £1,430, Wales £828, Scotland £1,022, and Northern Ireland £875 on the latest available basis. London’s rent growth was modest, but some other regions remained much stronger.

Private-sector data points in the same direction, though with different methodologies. Zoopla reported the average rent for new lets at £1,319 in March 2026, up 1.9% year on year, and said the market is cooling compared with the extremes of recent years, but still constrained by limited supply. Zoopla also noted that 52% of local authorities across Great Britain now have average rents above £1,000 per month, versus 23% in 2020.

For investors, the message is clear: rental growth is no longer explosive, but it remains positive and structurally supported. That is especially relevant for build-to-rent, student housing and income-focused portfolios. CBRE explicitly expects macroeconomic conditions to support the Living sector and boost investment into Build-to-Rent and Purpose-Built Student Accommodation, with yields expected to be stable in 2026 and potential for yield compression later in the year if transactions strengthen.

34. Investment strategy by buyer type

For owner-occupiers, the best strategy over the next five years is likely to be a financing-led strategy, not a market-timing strategy. Mortgage rates have eased from their peaks but remain meaningful; the Bank of England’s January 2026 data still showed newly drawn mortgage rates at 4.09%. Buyers who can refinance later may be better placed than buyers waiting for a dramatic price fall that official forecasts do not currently support.

For private landlords, the opportunity is selective rather than universal. The case is strongest where rent-to-price ratios are healthier, supply is tight, and there is strong employment-led tenant demand. That points more toward northern cities and selected Midlands markets than toward prime southern family housing. This is supported by stronger regional rent inflation in ONS data and by CBRE/Savills emphasis on income growth, not just capital growth, as the main return driver.

For institutional investors, the most interesting buckets remain Living, logistics, operational real estate and selected high-quality offices. CBRE expects investment to increase in alternatives such as healthcare and data centres, while also forecasting continued strength in Build-to-Rent and PBSA. Savills says 13 UK property sub-sectors are forecast to deliver annualised returns of over 8% between 2026 and 2030 in its cross-sector outlook.

35. Commercial real estate: the 2026–2031 picture

Commercial real estate is no longer a single story. It is a set of different markets moving at different speeds. CBRE’s 2026 outlook is especially useful here because it distinguishes clearly between sectors. The broad theme is that high-quality, well-located space should perform better, while weaker secondary stock remains challenged.

Offices

Offices are becoming a “flight to quality” market. CBRE says tight supply of high-quality stock is supporting renewals, regears and prime rent growth, while older and secondary offices, especially outside the best locations, remain under pressure. In the London office outlook, CBRE notes 9.1% prime rental growth in the City core and 18.8% in the West End core in 2025, with further growth expected in 2026.

That means the next five years for offices should not be framed as “good” or “bad”; they should be framed as “prime versus obsolete.” ESG compliance, amenity quality and location will matter more than ever. CBRE also warns that sustainability is increasingly affecting pricing and lending across sectors, not just offices.

Logistics and industrial

This remains one of the strongest sectors. CBRE expects occupier demand to stay consistent in 2026, with net absorption of 11.4 million sq ft in 2025, and says regions such as the North West and Yorkshire/North East should continue to see rental growth because vacancy and development supply remain tight.

Over a five-year horizon, logistics still benefits from e-commerce, supply-chain resilience and demand for modern, energy-efficient warehousing. Returns may not be as explosive as in the pandemic era, but the structural case remains strong.

Retail

Retail is better than it was, but still polarised. CBRE expects shortages of supply in sought-after locations but ongoing challenges outside the top tier, with many multi-site retailers continuing to optimise their portfolios. That suggests prime retail and retail warehousing may hold up, while weaker secondary high street assets remain vulnerable unless they can be repositioned.

36. Capital markets outlook and return expectations

For commercial investors, one of the most important current signals is that the return model is shifting back toward income plus gradual repricing. CBRE expects gradual growth in capital values in 2026, driven more by rising rents than by major yield compression, and forecasts aggregate prime net total returns of about 8.5% for 2026 across sectors. It also expects a more sustained improvement in investment activity, helped by lower debt costs and more competition among lenders.

Savills is directionally similar. Its December 2025 cross-sector outlook raised its total return forecast for 2026–2030 to 7.8%, and highlighted development viability constraints as a reason prime assets could remain scarce, supporting rental growth.

Taken together, that suggests the next five years are likely to reward portfolios built around asset quality, income resilience and ESG readiness, rather than highly leveraged yield-chasing.

37. Institutional capital trends

A major theme for 2026–2031 is broader and deeper institutional participation. CBRE expects increased deployment into real estate by defined contribution and local government pension schemes, supported by policy efforts to channel more capital into UK private markets. It also expects more activity from domestic core capital and cross-border capital, especially after larger transactions started to reappear toward the end of 2025.

This matters because institutional capital tends to prefer professionally managed, scalable sectors: build-to-rent, PBSA, healthcare, logistics, data centres and other operational real estate. CBRE explicitly says new sources of capital are targeting healthcare, hotels, hospitality and infrastructure-like sectors, while AI-driven demand continues to support data-centre development.

38. 5-year scenario analysis

Here is a practical scenario framework for 2026–2031:

| Scenario | House prices | Rents | Transactions | Best-performing assets |

|---|---|---|---|---|

| Optimistic | strong mid-single-digit annual growth by late period | steady growth | strong recovery | regional housing, BTR, logistics, prime offices |

| Base | low-to-mid single-digit annual growth | positive but moderating | gradual rise | regional residential, living sectors, logistics |

| Pessimistic | flat to low growth | still positive in most regions | subdued | defensive income assets, prime-only selective buying |

The optimistic case depends on faster monetary easing, falling mortgage costs and better real-income growth. The base case follows current OBR, Bank of England and CBRE/Savills signals. The pessimistic case would come from sticky inflation, slower rate cuts, weaker GDP or policy shocks affecting transactions and sentiment.

39. Strategic conclusion for 2026–2031

The five-year outlook for UK real estate is constructive, but selective. Residential should keep benefiting from undersupply and improving affordability over time. Rental assets should remain fundamentally strong, though growth is cooling from extreme levels. Commercial real estate should continue to reward quality and penalise obsolescence, especially in offices and retail. Logistics, Living and selected alternatives still offer the clearest medium-term case.

For Audit Consulting Group’s audience, the practical conclusion is this: the next five years are likely to favour disciplined buyers who prioritise asset quality, regional economics, tenant demand and financing structure over short-term speculation. The UK is unlikely to deliver a straight-line boom, but it does still offer a credible medium-term real estate growth story.