Companies House Annual Accounts Filing Services for UK Limited Companies

Leave your details and our team will get back to you shortly.

Filing annual accounts with Companies House is a statutory responsibility for most UK limited companies. While the filing itself may appear straightforward, the process often involves considerably more than submitting a document before a deadline.

The quality of a Companies House filing is usually determined long before submission takes place. Accurate bookkeeping, reconciled accounts, payroll records, director transactions and supporting documentation all contribute to the reliability of the final accounts.

For some businesses, annual accounts filing is a routine compliance requirement. For others, it becomes the point where reporting inconsistencies, missing records or historic bookkeeping issues are identified for the first time.

Companies House obligations continue regardless of whether a company is actively trading, recently incorporated, growing rapidly or dormant. Understanding what must be filed, when it must be filed and what information is required helps directors manage compliance more confidently and avoid unnecessary reporting issues.

Audit Consulting Group supports UK businesses with annual accounts preparation and Companies House filing, helping directors understand their reporting obligations and prepare statutory accounts accurately and on time.

Need support with Companies House annual accounts filing? Speak with our team to discuss your reporting requirements, filing deadlines and the information needed to complete your statutory reporting obligations.

What Companies House Annual Accounts Filing Actually Includes

Many directors view Companies House filing as a submission process. In practice, filing is usually the final stage of a wider year-end reporting exercise.

Before statutory accounts can be submitted, the underlying accounting records generally need to be reviewed to ensure they provide a reliable basis for reporting.

Depending on the circumstances, this may involve:

- reviewing bookkeeping records;

- checking bank reconciliations;

- reviewing director loan accounts;

- confirming payroll information;

- reviewing VAT records where applicable;

- preparing statutory accounts;

- validating reporting requirements;

- submitting annual accounts to Companies House.

One practical reality often overlooked by directors is that Companies House sees only the final accounts. The review work required to prepare those accounts frequently represents the largest part of the engagement.

Where records have been maintained consistently throughout the year, preparation can be relatively straightforward. Where accounting records contain gaps, unresolved balances or inconsistencies, additional review is often required before filing can proceed confidently.

It is also important to understand that Companies House filing and Corporation Tax obligations are separate compliance requirements. Although both rely on financial information, they serve different purposes and follow different reporting processes.

Who Needs To File Annual Accounts?

Most UK limited companies must file annual accounts with Companies House, regardless of company size or turnover.

This commonly includes:

- newly incorporated limited companies;

- micro-entity companies;

- small businesses;

- owner-managed companies;

- consultancy and contractor businesses;

- VAT-registered companies;

- e-commerce businesses;

- property companies;

- growing SMEs;

- dormant companies.

Directors are often surprised to learn that dormant companies may still have reporting obligations despite having little or no trading activity.

Newly incorporated companies frequently face a different challenge. The first filing cycle often introduces unfamiliar concepts such as accounting reference dates, statutory deadlines and reporting periods. Understanding these requirements early generally makes future compliance significantly easier.

Many first-year directors assume filing obligations begin only once the business becomes fully operational. In practice, reporting responsibilities often begin much earlier than expected.

Common Filing Problems & Compliance Risks

Most Companies House filing issues do not begin at the filing stage itself. They usually develop gradually throughout the accounting period and become visible only when annual accounts preparation begins.

Examples commonly encountered during year-end reviews include:

- unreconciled bank accounts;

- missing supplier invoices;

- incomplete bookkeeping records;

- director loan account discrepancies;

- incorrect transaction classifications;

- VAT records that do not align with accounting records;

- payroll information that requires clarification;

- historic balances carried forward without investigation;

- misunderstanding dormant company status.

These issues are not unusual. Most can be resolved once identified. The challenge is that they often emerge when filing deadlines are approaching and time becomes more limited.

Businesses that regularly review their bookkeeping records throughout the year generally experience fewer filing complications than those relying entirely on year-end preparation.

Another common misconception is that filing software automatically guarantees accurate reporting. Modern accounting platforms can simplify reporting processes, but they cannot replace proper review, reconciliation and professional judgement.

Types Of Companies House Accounts

The type of accounts submitted to Companies House depends on the company’s size, reporting status and eligibility for specific reporting frameworks.

The type of accounts submitted to Companies House depends on the company’s size, reporting status and eligibility for specific reporting frameworks.

Micro-Entity Accounts

Many smaller companies qualify to prepare micro-entity accounts under FRS 105.

This framework provides simplified reporting requirements while still requiring accurate accounting records and appropriate financial reporting.

Micro-entity accounts are commonly used by owner-managed businesses, consultants, contractors and smaller trading companies.

Small Company Accounts

Companies that exceed micro-entity thresholds may prepare accounts under FRS 102 Section 1A.

These accounts generally require broader disclosures and may provide a more detailed picture of the company’s financial position and activities.

Dormant Company Accounts

Dormant companies often have simplified reporting obligations. However, simplified reporting should not be confused with the absence of reporting obligations.

One of the most frequent misunderstandings encountered by accountants is the assumption that a dormant company no longer needs to file accounts. In many circumstances, filing obligations continue despite the absence of trading activity.

Full Statutory Accounts

Larger companies and businesses with more complex reporting requirements may need to prepare full statutory accounts containing additional disclosures and supporting information.

As reporting complexity increases, the preparation process typically becomes more detailed and requires a broader review of the underlying accounting records.

Group & Connected Company Reporting

Businesses operating within group structures may face additional reporting considerations.

Related-party transactions, intercompany balances and group reporting requirements can introduce additional layers of review before accounts are finalised and submitted.

These situations often require more detailed preparation than a standard standalone company filing.

Filing Deadlines, Penalties & Director Responsibilities

Companies House applies strict deadlines for annual accounts filing, and responsibility for meeting those deadlines ultimately remains with the company’s directors.

For most private limited companies, annual accounts are generally due within nine months of the financial year-end. First-year reporting periods may operate differently, which is why newly incorporated companies often require additional guidance when approaching their first filing cycle.

Late filing can result in automatic financial penalties. Repeated late filing may lead to increased penalties and can create unnecessary compliance complications for directors.

One practical reality that accountants regularly encounter is that filing deadlines rarely become a problem because the submission itself is difficult. More often, delays occur because records require review, supporting information is missing or reporting questions remain unresolved shortly before the deadline.

For this reason, many businesses benefit from beginning preparation well before filing becomes urgent.

Director Responsibilities & Personal Accountability

Although accountants may prepare and submit annual accounts on behalf of a company, directors remain responsible for ensuring statutory obligations are met.

Although accountants may prepare and submit annual accounts on behalf of a company, directors remain responsible for ensuring statutory obligations are met.

This responsibility typically includes:

- maintaining adequate accounting records;

- retaining supporting documentation;

- approving annual accounts before submission;

- ensuring filing deadlines are met;

- complying with Companies House reporting requirements.

Many first-time directors assume appointing an accountant transfers responsibility entirely. In reality, professional support can assist with compliance, but Companies House continues to regard directors as responsible for the accuracy and timeliness of company filings.

Understanding this distinction helps reduce misunderstandings and encourages stronger reporting practices throughout the year.

Annual Accounts vs Confirmation Statement vs Corporation Tax Return

Many directors encounter confusion when trying to understand the difference between annual accounts, confirmation statements and Corporation Tax returns.

Although all three form part of a company’s reporting responsibilities, they serve different purposes.

Annual accounts provide financial information about the company and are submitted to Companies House.

The confirmation statement confirms that company information held by Companies House remains accurate and up to date.

The Corporation Tax Return (CT600) is submitted to HMRC and relates to the company’s tax position rather than statutory company reporting.

Completing one obligation does not automatically satisfy the others.

A company may successfully file annual accounts while still having outstanding Corporation Tax obligations. Likewise, submitting a CT600 does not replace Companies House filing requirements.

This distinction is particularly important for first-year companies and directors managing compliance responsibilities without internal finance teams.

First-Year Accounts & New Companies

The first annual accounts filing cycle is often the most confusing reporting period a company experiences.

Many directors focus primarily on incorporation, customer acquisition and day-to-day operations during the first year. Reporting obligations often receive attention only once filing deadlines begin approaching.

One area that frequently creates confusion is the accounting reference date. This date determines the company’s financial year-end and influences when annual accounts must be prepared and filed.

Common first-year questions include:

- When does the first filing deadline apply?

- What is an accounting reference date?

- Does a dormant period still need to be reported?

- What happens if the company only traded for part of the year?

- How do Companies House and HMRC deadlines interact?

- Which records should be retained for reporting purposes?

Many first-year reporting issues arise because directors assume filing obligations begin only after trading activity reaches a certain level. In practice, statutory reporting requirements often apply regardless of turnover or trading volume.

Establishing clear bookkeeping procedures during the first year generally makes future annual accounts preparation significantly more straightforward.

Businesses that are still in the early stages of their reporting journey may also benefit from reviewing their company formation requirements and compliance obligations to better understand how filing responsibilities evolve over time.

Why Companies House Filings Get Rejected

Many directors are unaware that Companies House can reject filings where submission requirements have not been met.

Many directors are unaware that Companies House can reject filings where submission requirements have not been met.

Rejections are not necessarily signs of serious compliance failures. In many cases, they result from administrative issues, missing information or inconsistencies within the filing.

Examples may include:

- incomplete submissions;

- incorrect reporting formats;

- invalid filing information;

- missing disclosures where required;

- submission errors;

- data inconsistencies.

It is important to understand that Companies House reviews whether a filing meets submission requirements. It does not assess the commercial purpose of the business or provide assurance that underlying bookkeeping records are correct.

Where a rejection occurs, the filing usually needs to be corrected and resubmitted.

The practical difficulty is that rejections often arise when filing deadlines are already approaching. Businesses that leave preparation until the final days before submission frequently have fewer options available if unexpected issues emerge.

Early preparation provides more flexibility to investigate questions, obtain missing information and address reporting concerns before statutory deadlines become critical.

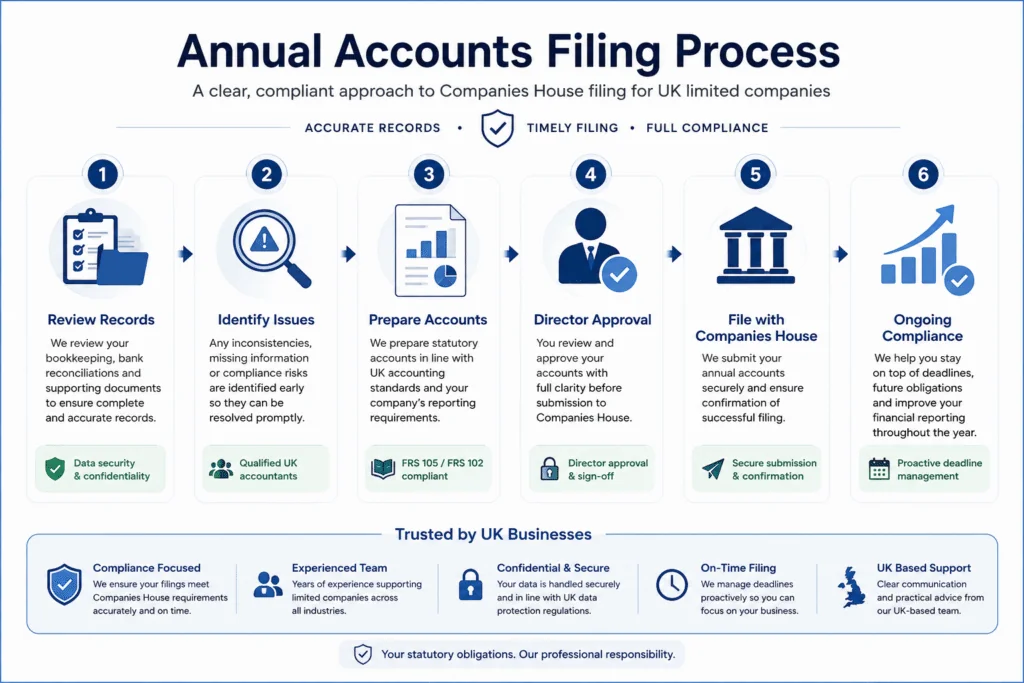

How The Companies House Filing Process Works

Although every business has different reporting requirements, most annual accounts filing projects follow a broadly similar process.

The submission itself is usually the final stage. The majority of work often takes place beforehand, when accounting records are reviewed, reporting issues are identified and statutory accounts are prepared.

Step 1 – Reviewing Existing Records

The process generally begins with reviewing the accounting information available for the reporting period.

This may include bookkeeping records, bank reconciliations, payroll information, VAT records, prior year accounts and supporting documentation.

The objective is not simply to collect data but to determine whether the records provide a reliable basis for statutory reporting.

Step 2 – Identifying Reporting Issues

Where records are incomplete or inconsistent, reporting issues often become visible during the review stage.

Examples may include:

- unreconciled balances;

- missing invoices;

- unclear director transactions;

- historic bookkeeping errors;

- inconsistencies between reporting systems.

Many annual accounts projects involve resolving these matters before statutory accounts can be prepared accurately.

Step 3 – Preparing The Statutory Accounts

Once sufficient information is available, the annual accounts are prepared under the appropriate reporting framework.

This stage converts the underlying accounting records into the statutory format required for Companies House filing.

The complexity of this process depends on the company’s size, reporting requirements and the quality of the records provided.

Step 4 – Director Review & Approval

Before submission, directors should understand the information being reported.

This stage often provides an opportunity to discuss unusual balances, reporting adjustments or compliance questions before the accounts become part of the company’s filing history.

Step 5 – Submission To Companies House

Once approved, the accounts are submitted using the appropriate filing method.

Following acceptance, the filing becomes part of the company’s public reporting record.

Although submission marks the end of the filing process, it frequently highlights opportunities to improve bookkeeping procedures, reporting systems and compliance processes for future years.

Who Handles The Work?

Companies House annual accounts filing often involves more than a simple submission service.

Depending on the circumstances, the process may require expertise across bookkeeping, statutory reporting, Corporation Tax compliance, payroll records, VAT reporting and year-end financial review.

The level of involvement depends largely on the business itself.

A dormant company with minimal activity may require only limited review. A growing business with employees, VAT registration and multiple revenue streams may require considerably more preparation before filing can proceed.

The objective is not merely to submit accounts but to ensure the filing is supported by reliable records and an appropriate understanding of reporting obligations.

Accounting Software, HMRC Systems & Companies House Integration

Modern accounting software has simplified many aspects of year-end reporting. However, software alone does not guarantee accurate annual accounts.

Many filing issues arise because information has been categorised incorrectly, transactions have not been reconciled or records have not been reviewed consistently throughout the year.

Companies House filing projects frequently involve records originating from:

- Xero;

- QuickBooks;

- Sage;

- Dext;

- Hubdoc;

- AutoEntry;

- payroll systems;

- online banking platforms;

- e-commerce platforms;

- payment processing systems.

As businesses grow, maintaining consistency across multiple systems often becomes one of the biggest reporting challenges.

Accountants regularly discover that discrepancies between bookkeeping records, payroll information, VAT reporting and external platforms contribute to year-end reporting issues.

Regular reviews throughout the year generally reduce the likelihood of these discrepancies affecting annual accounts preparation.

Industries & Business Types We Work With

Companies House filing obligations apply across virtually every sector of the UK economy.

Audit Consulting Group supports businesses operating in a wide range of industries, including:

- construction companies and CIS contractors;

- consultants and professional advisers;

- e-commerce businesses;

- technology companies;

- property businesses;

- retail companies;

- service-based businesses;

- startups and growing SMEs;

- owner-managed companies;

- dormant companies.

Each industry creates different reporting considerations.

An e-commerce business processing large transaction volumes through multiple payment providers faces different reporting challenges from a consultancy company issuing a small number of invoices each month. Likewise, property businesses often encounter reporting considerations that differ from those affecting contractors or technology firms.

Understanding these operational differences helps create a more efficient filing process and supports more reliable reporting outcomes.

What Clients Often Underestimate

Many directors expect the filing itself to be the most important part of the process.

In practice, the preparation work behind the filing often has a much greater influence on the final outcome.

One recurring issue encountered during year-end reviews is the assumption that accounting software automatically guarantees accurate reporting. While software can automate many tasks, it cannot replace proper review, reconciliation and professional judgement.

Another frequently underestimated area involves director transactions.

Directors often pay company expenses personally, transfer funds between personal and business accounts or make withdrawals throughout the year without fully appreciating how these movements affect year-end reporting.

These situations are common and usually manageable, but they often require additional review before statutory accounts can be finalised.

Businesses also tend to underestimate how quickly reporting requirements evolve as they grow. Processes that worked effectively during the first year may become less suitable once transaction volumes increase, staff are hired or VAT registration becomes necessary.

Strategic Filing Guidance For Directors

Annual accounts filing should not be viewed purely as a compliance requirement.

The accounts submitted to Companies House often become one of the most important financial records a business produces. They may later be reviewed by lenders, investors, shareholders, finance providers and potential business partners.

For this reason, directors often benefit from considering broader questions alongside filing itself.

- Are accounting records reviewed regularly throughout the year?

- Do reporting systems remain suitable as the business grows?

- Are bookkeeping, VAT and payroll processes working consistently together?

- Would management accounts improve visibility between year-end reporting periods?

- Are future compliance obligations being monitored proactively?

Businesses that treat annual accounts as part of a wider reporting framework often gain more value from the process than those focusing solely on the filing deadline.

Choosing The Right Filing Support For Your Business

Not every company requires the same level of support when preparing and filing annual accounts.

A dormant company with minimal activity may require relatively straightforward filing assistance. A growing business with employees, VAT registration, multiple sales channels and increasingly complex reporting requirements may require a far more detailed review before statutory accounts can be prepared confidently.

When evaluating filing support, directors often benefit from considering:

- whether bookkeeping records are complete and up to date;

- whether previous filings have been reviewed appropriately;

- whether reporting requirements have changed as the business has evolved;

- whether director transactions require additional review;

- whether broader accounting and tax support may also be beneficial;

- whether future growth is likely to increase compliance requirements.

The most suitable solution is not always determined by company size. In many cases, the condition of the accounting records and the complexity of the reporting environment are more important factors.

Businesses often gain the greatest value from support that identifies potential reporting issues before they become filing problems.

Results, Compliance Outcomes & Business Impact

Successful annual accounts filing is not simply about submitting information before a deadline.

Well-managed reporting processes often create wider benefits for the business, including:

- greater confidence in financial records;

- reduced risk of filing errors;

- improved visibility over company performance;

- better preparation for future compliance obligations;

- stronger support for lending and finance applications;

- more reliable year-end reporting;

- improved readiness for future growth.

While every company operates differently, businesses that maintain organised records throughout the year generally spend less time resolving reporting issues when statutory deadlines approach.

The long-term value often comes not from the filing itself but from the quality of the records and reporting processes that support it.

Filing Deadlines to Know

- First-year deadline: 21 months from company incorporation

- Subsequent years: 9 months after your financial year-end

We’ll help you calculate your exact deadlines and send automated reminders.

Improved Case Studies — Companies House Filing

Case 1: Startup Tech Company – Manchester

A newly incorporated app development company in Manchester with £180,000 first-year revenue needed help preparing and filing their first statutory accounts. Their bookkeeping records were incomplete, and the Companies House deadline was approaching in less than three weeks.

Audit Consulting Group handled the full Companies House annual accounts filing process.

Our work included:

• Reviewing and reconciling 12 months of financial transactions

• Preparing micro-entity statutory accounts under FRS 105

• Coordinating corporation tax calculations for HMRC

• Submitting accounts via Companies House digital filing system

• Providing director approval and filing confirmation

Results:

• Accounts prepared and filed within 5 working days

• Avoided late filing penalty of £150–£375

• Identified £2,800 in allowable expenses

• Delivered clear financial summary for investors

Director feedback:

“We were close to missing our first filing deadline. Audit Consulting Group took over and handled everything quickly and professionally.”

Case 2: Dormant Company – Bristol

A holding company in Bristol with no trading activity needed to file dormant company accounts. The directors were unaware that filing was still required and had only 48 hours before the Companies House deadline.

Audit Consulting Group prepared and filed dormant company accounts.

Our work included:

• Preparing dormant statutory accounts

• Verifying company status and financial inactivity

• Submitting accounts through Companies House WebFiling

• Providing confirmation statement reminder

Results:

• Accounts filed within 24 hours

• Avoided £150 late filing penalty

• Ensured continued compliance with Companies House

• Provided future deadline tracking

Director feedback:

“We didn’t realise dormant companies still had to file. They handled everything within a day and saved us from penalties.”

Case 3: E-commerce Brand – London

An online retail company in London with £650,000 annual turnover had fallen behind on Companies House filings and missed one previous deadline. They required catch-up filing for two accounting periods and correction of previously submitted data.

Audit Consulting Group performed a full catch-up filing.

Our work included:

• Reconciling 2 years of bookkeeping data

• Preparing statutory small company accounts (FRS 102)

• Amending previously filed accounts

• Submitting updated accounts to Companies House

• Coordinating corporation tax filings with HMRC

Results:

• Filed two years of overdue accounts within 10 days

• Reduced risk of £750–£1,500 penalties

• Improved financial reporting accuracy

• Restored Companies House compliance status

Owner feedback:

“We were worried about penalties and compliance issues. Audit Consulting Group got everything back on track quickly.”

What Happens After Annual Accounts Are Filed?

For many directors, filing marks the end of the reporting process. From a business perspective, however, it often becomes the starting point for the next reporting cycle.

The completed accounts provide a structured overview of the company’s financial position and may influence future planning, budgeting, borrowing decisions, dividend planning and broader business strategy.

Many businesses use the year-end review process to identify opportunities to improve record keeping, strengthen reporting procedures or introduce additional financial controls.

Others choose to enhance visibility through services such as Management Accounts, improve record quality through Bookkeeping Services or review tax obligations through Corporation Tax Services.

Viewed in this context, annual accounts filing becomes more than a statutory requirement. It becomes an opportunity to strengthen future financial reporting and decision-making.

Communication, Deadlines & Ongoing Compliance Support

Compliance obligations rarely remain static.

A company that initially requires only annual accounts filing may later become VAT registered, hire employees, expand operations or introduce more sophisticated reporting requirements.

As businesses evolve, different compliance areas often become increasingly connected.

Bookkeeping affects annual accounts. Payroll affects year-end reporting. VAT influences financial accuracy. Corporation Tax reporting relies on many of the same underlying records used for statutory accounts preparation.

Regular communication and proactive review help reduce the likelihood of unexpected reporting issues appearing shortly before important deadlines.

Many directors find that ongoing support becomes increasingly valuable as reporting requirements become more complex over time.

Why Businesses Choose Audit Consulting Group

Companies House annual accounts filing rarely exists in isolation. In most businesses, it sits alongside bookkeeping, payroll, VAT reporting, Corporation Tax compliance and wider financial management responsibilities.

Audit Consulting Group supports UK companies across these areas, allowing directors to view annual accounts filing within the broader context of business reporting rather than as a standalone submission requirement.

One practical observation we see regularly is that filing issues are often identified during the review process rather than during submission itself. Unreconciled balances, historic bookkeeping inconsistencies, director transaction questions and reporting misunderstandings frequently emerge while preparing the accounts rather than while filing them.

This is why our approach focuses not only on submitting accounts but also on understanding the records, processes and compliance responsibilities that support them.

Clients value clear communication, realistic guidance and support that helps them understand what is required, why it matters and how future reporting obligations can be managed more effectively.

Frequently Asked Questions

What is the deadline for filing annual accounts with Companies House?

For most private limited companies, annual accounts are generally due within nine months of the financial year-end. Different timelines may apply during the first reporting period.

Can late annual accounts still be filed?

Yes. Although late filing penalties may apply, annual accounts can generally still be submitted. The most appropriate approach depends on the company’s circumstances and reporting position.

Can previously filed accounts be corrected?

In certain situations, amended accounts may be submitted where errors are identified after filing.

What documents are usually needed to prepare annual accounts?

Requirements vary, but commonly include bookkeeping records, bank statements, invoices, payroll information, VAT records and details of significant financial transactions.

Do dormant companies need to file annual accounts?

In most circumstances, yes. Dormant companies generally remain subject to Companies House reporting obligations.

Is a confirmation statement the same as annual accounts?

No. A confirmation statement and annual accounts are separate Companies House filing requirements that serve different purposes.

What happens if Companies House rejects a filing?

The reason for rejection generally needs to be addressed before the filing can be resubmitted. Early preparation often reduces the likelihood of deadline pressure if issues arise.

Can you help if bookkeeping records are incomplete?

Yes. Many annual accounts projects involve reviewing incomplete records, identifying missing information and establishing the most practical route towards accurate reporting.

Do you also assist with Corporation Tax reporting?

Yes. We support businesses with Corporation Tax compliance and related accounting reporting requirements where required.

Official guidance on Companies House annual accounts filing:

Companies House accounts guidance:

https://www.gov.uk/annual-accounts

Late filing penalties:

https://www.gov.uk/

Filing deadlines:

https://www.gov.uk/file-your-company-accounts-and-tax-return

Discuss Your Companies House Filing Requirements

Whether you are approaching your first filing deadline, managing a dormant company, reviewing historic reporting issues or preparing annual accounts for a growing business, understanding your Companies House obligations is an important part of maintaining compliance.

Audit Consulting Group supports UK limited companies with annual accounts preparation, statutory reporting, Companies House filing, bookkeeping, Corporation Tax compliance and wider accounting services.

If you would like to discuss your reporting obligations, filing deadlines or the information required to prepare your annual accounts, our team can help you identify the most practical next steps for your business.

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants