LTD Company Annual Accounts Services for UK Limited Companies

Leave your details and our team will get back to you shortly.

Annual accounts are one of the most important financial reporting responsibilities for a UK limited company. While many directors associate annual accounts with Companies House deadlines, the accounts themselves serve a much broader purpose. They provide a structured picture of the company’s financial position, explain how the business performed during the accounting period and form the foundation for several key compliance obligations.

Preparing annual accounts is rarely just an administrative exercise. The process often involves reviewing bookkeeping records, reconciling balances, analysing director transactions, assessing financial performance and ensuring that the company’s records accurately reflect what happened during the year.

For some businesses, annual accounts preparation is relatively straightforward. For others, particularly companies that have grown quickly, changed systems, hired employees, registered for VAT or experienced bookkeeping challenges, the year-end review can uncover issues that require investigation before the accounts can be finalised.

Audit Consulting Group supports UK limited companies with annual accounts preparation, statutory financial reporting and year-end compliance requirements. Our role is not simply to prepare financial statements, but to help directors understand what the accounts show, what reporting obligations apply and what practical issues may need attention before year-end reporting is completed.

Need help preparing your annual accounts? Speak with our team to discuss your company’s reporting requirements, financial records and year-end obligations.

What LTD Company Annual Accounts Actually Include

Many directors assume annual accounts are produced by exporting figures from accounting software and submitting them at year-end. In practice, preparing reliable annual accounts often involves significantly more review and analysis.

Many directors assume annual accounts are produced by exporting figures from accounting software and submitting them at year-end. In practice, preparing reliable annual accounts often involves significantly more review and analysis.

The final accounts are based on the information recorded throughout the accounting period. Before those figures can be relied upon, accountants typically review the quality of the underlying records and assess whether the financial statements accurately represent the company’s activities.

Depending on the business, annual accounts preparation may involve:

- reviewing bookkeeping records and year-end balances;

- checking bank reconciliations and control accounts;

- reviewing income, expenditure and trading activity;

- assessing assets, liabilities and outstanding obligations;

- reviewing director loan account movements;

- considering dividends and shareholder transactions;

- preparing statutory financial statements;

- applying the appropriate accounting framework;

- supporting Corporation Tax and Companies House reporting requirements.

Annual accounts are also used beyond compliance reporting. Banks, lenders, investors, suppliers and potential business partners may review annual accounts when assessing a company’s financial position and stability.

For this reason, accurate preparation is important. The accounts often become one of the most widely referenced financial documents a business produces during the year.

Who This Service Is For

Annual accounts preparation is relevant to most UK limited companies, regardless of turnover, industry or stage of growth.

This service is commonly used by:

- newly incorporated limited companies;

- owner-managed businesses;

- consultants and contractors;

- micro-entity companies;

- small companies;

- growing SMEs;

- e-commerce businesses;

- property companies;

- professional service firms;

- dormant companies.

Some directors need support because they are preparing annual accounts for the first time. Others seek assistance because their reporting requirements have become more complex as the company has grown.

Annual accounts are equally important for established companies. As transaction volumes increase and reporting obligations become more interconnected, the year-end review process often requires greater attention than directors initially expect.

Even dormant companies may still need annual accounts prepared under the appropriate reporting framework and remain subject to statutory reporting obligations.

Common Year-End Reporting Problems & Compliance Risks

Most annual accounts challenges do not originate at year-end. More commonly, they develop gradually throughout the accounting period and only become visible once a detailed review begins.

Examples frequently identified during annual accounts preparation include:

- incomplete bookkeeping records;

- unreconciled bank accounts;

- missing invoices or supporting documentation;

- unclear director loan account balances;

- incorrect transaction coding;

- unresolved VAT adjustments;

- historic bookkeeping errors;

- balances carried forward without review;

- misunderstanding dormant company reporting obligations.

These issues are not unusual. Many can be resolved once identified. The challenge is that they often appear when directors are already focused on year-end deadlines and reporting requirements.

One observation accountants frequently make is that annual accounts preparation rarely becomes difficult because accounting standards are complex. More often, the challenge lies in understanding what has happened throughout the year and ensuring the records tell a complete and accurate financial story.

Businesses that maintain organised bookkeeping records throughout the year generally experience a more efficient year-end process than those attempting to reconstruct financial information shortly before reporting deadlines.

Types Of Annual Accounts For Limited Companies

The type of annual accounts prepared depends on the company’s size, eligibility and reporting requirements.

The type of annual accounts prepared depends on the company’s size, eligibility and reporting requirements.

Not every limited company follows the same reporting framework, which is why understanding the correct category is an important part of the preparation process.

Micro-Entity Accounts

Many smaller companies qualify to prepare micro-entity accounts under FRS 105.

This framework simplifies certain reporting requirements while still requiring accurate accounting records and appropriate financial reporting.

Micro-entity reporting is commonly used by consultants, contractors, owner-managed businesses and smaller limited companies.

Small Company Accounts

Companies that exceed micro-entity thresholds often prepare accounts under FRS 102 Section 1A.

These accounts generally require broader disclosures and provide a more detailed picture of the company’s financial position.

As businesses grow, the preparation process often becomes more detailed because additional reporting considerations may apply.

Dormant Company Accounts

Dormant companies can often benefit from simplified reporting requirements, but this should not be confused with having no reporting obligations at all.

One of the most common misconceptions among directors is that a dormant company no longer requires annual accounts. In many situations, dormant companies remain subject to statutory reporting obligations and Companies House requirements.

Full Statutory Accounts

Larger companies and businesses with more complex reporting requirements may need to prepare full statutory accounts with additional disclosures and supporting information.

The complexity of the reporting process generally increases alongside the complexity of the business itself.

Group & Related Company Reporting

Companies operating within group structures may face additional reporting considerations.

Intercompany balances, related-party transactions and group reporting requirements often require further review before annual accounts can be finalised accurately.

These situations typically involve a broader assessment than a standard standalone limited company engagement.

What Accountants Commonly Discover During Year-End Reviews

One area that directors often underestimate is how much insight a year-end review can provide into the quality of a company’s financial records.

It is not unusual for annual accounts preparation to identify issues that were not obvious during day-to-day trading. These may include duplicate transactions, unreconciled balances, incorrect VAT treatment, historical bookkeeping adjustments or director transactions that require clarification.

Many of the issues identified during year-end reviews are not serious compliance failures. More often, they are routine record-keeping inconsistencies that have accumulated gradually throughout the year and only become visible when the financial records are examined as a whole.

In many cases, the purpose of the review is not simply to produce financial statements. It is to ensure the figures presented within those statements are supported by records that are accurate, consistent and appropriate for statutory reporting.

This review process often provides value beyond compliance. It can help directors understand where reporting processes may be improved before the next accounting period begins.

Typical Pricing & Fee Expectations

The cost of preparing LTD company annual accounts depends on the activity, complexity and record quality of the company.

A small limited company with reconciled bookkeeping records, clear transaction history and limited adjustments will usually require less preparation work than a business with incomplete records, director loan movements, VAT activity, payroll records or multiple income streams.

Common factors that affect annual accounts preparation fees include:

- transaction volume during the accounting period;

- whether bookkeeping records are complete and reconciled;

- whether the company is dormant, micro-entity, small or more complex;

- whether VAT, payroll or CIS records need review;

- whether director loan accounts or dividends require clarification;

- whether previous year balances need investigation;

- whether Corporation Tax reporting is required alongside the accounts.

Many directors initially compare annual accounts services by price alone. In practice, the largest difference between one engagement and another is often the condition of the records behind the accounts.

Clean records usually make preparation more efficient. Incomplete or inconsistent records can increase the review work required before reliable annual accounts can be finalised.

Deadlines, Timelines & Reporting Requirements

Limited companies have reporting responsibilities with both Companies House and HMRC. These responsibilities are connected, but they are not the same.

For most private limited companies, annual accounts are generally filed with Companies House within nine months of the company’s financial year-end. Corporation Tax returns are usually submitted to HMRC within twelve months of the end of the accounting period, while Corporation Tax payment is normally due earlier.

Although annual accounts support both Companies House and HMRC reporting obligations, preparing the accounts and filing the accounts are separate stages within the wider compliance process.

First-year companies often face additional uncertainty because accounting reference dates, incorporation dates and trading dates may not align in the way directors expect.

The preparation process should usually begin before statutory deadlines become urgent. Annual accounts may require bookkeeping review, reconciliations, year-end adjustments, director approval and coordination with Corporation Tax reporting before the final position is complete.

Leaving preparation until the final weeks can reduce the time available to resolve missing information, unusual balances or record-keeping issues.

Annual Accounts vs Corporation Tax Return vs Management Accounts

Annual accounts, Corporation Tax returns and management accounts are often connected, but they serve different purposes.

Annual accounts are formal financial statements prepared at the end of an accounting period. They explain the company’s financial position and support statutory reporting.

A Corporation Tax Return is submitted to HMRC and reports the company’s taxable position. It is connected to the annual accounts but remains a separate tax obligation.

Management accounts are internal reports usually prepared monthly or quarterly to help directors monitor performance during the year.

This distinction matters because annual accounts are mainly retrospective. They show what happened during a completed reporting period. Management accounts help directors understand what is happening while there is still time to make operational decisions.

Many growing businesses use both. Annual accounts satisfy statutory reporting requirements, while management accounts improve financial visibility between year-end periods.

Documents Commonly Needed Before Annual Accounts Preparation

One of the most useful ways to make annual accounts preparation smoother is to understand what information is normally required before the work begins.

The exact documents depend on the company, but accountants commonly request:

- business bank statements;

- sales invoices and income records;

- supplier bills and expense records;

- payroll reports where applicable;

- VAT returns and VAT workings where applicable;

- details of director loans and withdrawals;

- dividend records and board minutes where relevant;

- asset purchase information;

- loan or finance agreements;

- previous year accounts if changing accountant.

Providing clear information at the start of the process usually reduces delays and helps identify reporting questions earlier.

Where information is missing, annual accounts can often still be prepared, but additional review and clarification may be required before the accounts can be finalised accurately.

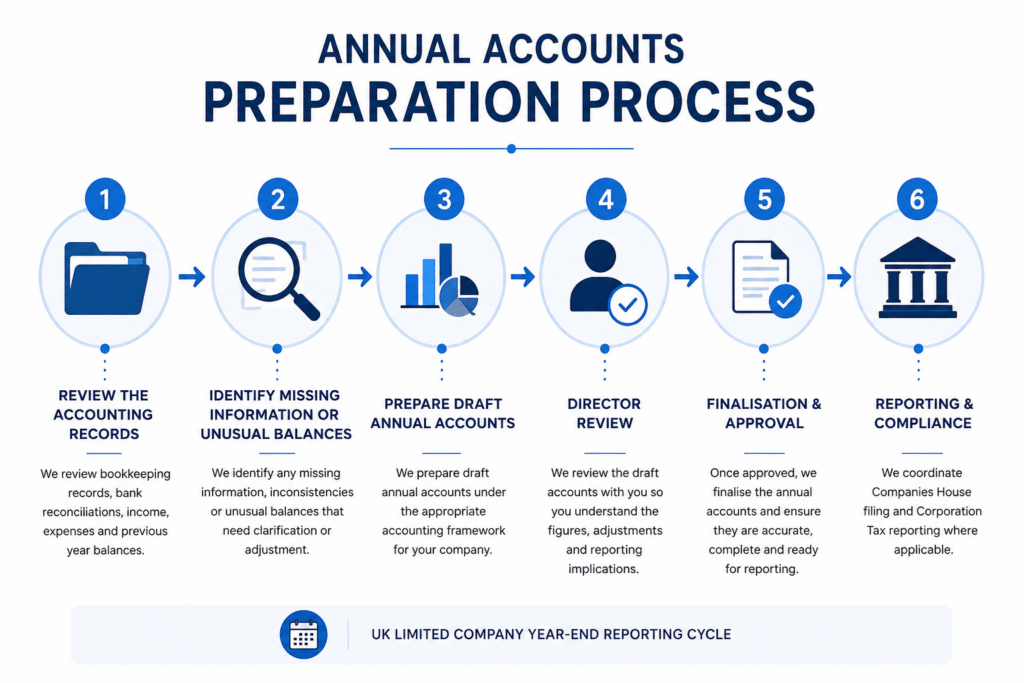

How The Annual Accounts Preparation Process Works

The annual accounts preparation process usually starts with understanding the records available for the accounting period.

The objective is to determine whether the records are complete, whether important balances are supported and whether year-end adjustments are required before the accounts can be finalised.

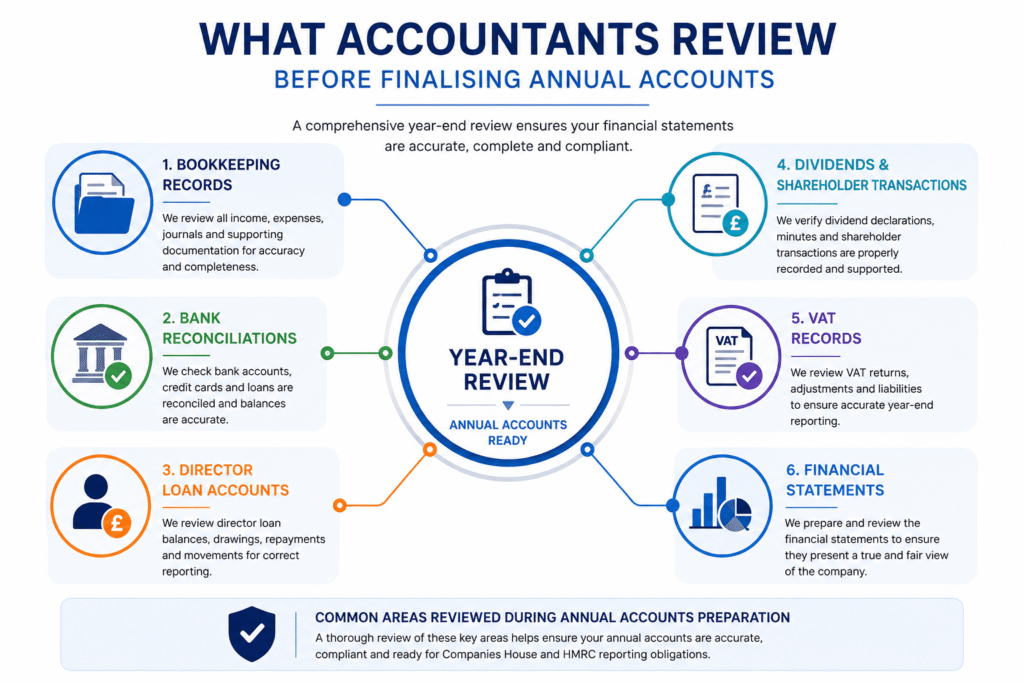

Step 1 – Review The Accounting Records

The process begins with reviewing bookkeeping records, bank reconciliations, income, expenses, payroll data, VAT records and prior year balances where relevant.

Step 2 – Identify Missing Information Or Unusual Balances

Where records are incomplete or inconsistent, additional information may be required. This may involve missing invoices, unexplained transactions, director loan movements, historic balances or entries that need reclassification.

Step 3 – Prepare Draft Annual Accounts

Once the records have been reviewed, draft annual accounts are prepared under the appropriate accounting framework for the company.

Step 4 – Director Review

The draft accounts are reviewed with the director so that key figures, year-end adjustments and reporting implications are understood before finalisation.

Step 5 – Finalisation & Reporting Coordination

Once approved, the accounts can be finalised and used to support Companies House filing and Corporation Tax reporting where applicable.

A strong annual accounts process is not simply about working quickly at the end of the year. It allows enough time to review records properly, resolve issues and ensure the final accounts reflect the company’s financial position accurately.

Who Handles The Work?

Annual accounts preparation may involve several areas of accounting and tax knowledge.

Depending on the company, the work may require understanding of bookkeeping, statutory accounts, Corporation Tax, VAT, payroll, director loan accounts, dividends and Companies House reporting requirements.

A dormant company may require a limited review. A growing company with employees, VAT registration and multiple income streams may need a broader year-end assessment before the accounts can be prepared properly.

Audit Consulting Group supports limited companies by reviewing the available records, identifying reporting issues, preparing annual accounts and explaining the year-end position in practical language.

The aim is not only to produce compliant accounts. It is also to help directors understand what the figures mean and how the year-end position connects with wider business reporting.

Accounting Standards, Financial Statements & Reporting Frameworks

Annual accounts are prepared according to specific accounting frameworks rather than a single standard format. The framework used depends on the company’s size, reporting eligibility and statutory requirements.

Many directors focus primarily on deadlines and compliance obligations, but the accounting framework chosen can significantly influence what information appears within the final accounts and what disclosures may be required.

FRS 105 – Micro-Entity Reporting

FRS 105 is commonly used by qualifying micro-entity companies.

The framework provides simplified reporting requirements while still requiring accurate accounting records and appropriate financial reporting.

Micro-entity reporting is frequently used by consultants, contractors, owner-managed businesses and smaller limited companies.

FRS 102 Section 1A – Small Companies

Companies that exceed micro-entity thresholds often prepare annual accounts under FRS 102 Section 1A.

This framework generally requires broader disclosures and may provide a more detailed picture of the company’s financial position and activities.

As businesses grow, reporting requirements often become more sophisticated and may require additional review before annual accounts can be finalised.

What Financial Statements Are Included?

Although the exact format varies, annual accounts commonly include:

- a balance sheet;

- a profit and loss account;

- supporting notes and disclosures where required;

- director-related reporting information;

- additional statements depending on the reporting framework used.

Together, these financial statements provide a structured summary of how the company performed during the accounting period and what financial position existed at year-end.

For directors, annual accounts are often one of the clearest opportunities to step back from day-to-day operations and assess the overall financial health of the business.

Accounting Software, Financial Records & Reporting Systems

The quality of annual accounts is heavily influenced by the quality of the records maintained throughout the year.

Modern accounting software has simplified many aspects of bookkeeping and financial reporting. However, software alone does not guarantee accurate annual accounts.

During year-end reviews, accountants frequently discover issues caused by incomplete bookkeeping, incorrect transaction coding, unreconciled balances or inconsistencies between different reporting systems.

Records used during annual accounts preparation often originate from:

- Xero;

- QuickBooks;

- Sage;

- Dext;

- Hubdoc;

- AutoEntry;

- online banking platforms;

- payroll software;

- e-commerce systems;

- payment processing platforms.

As businesses grow, maintaining consistency across multiple systems becomes increasingly important. Small discrepancies can accumulate over time and become more visible during year-end reporting.

This is one reason companies that regularly review their bookkeeping records often experience a more efficient annual accounts preparation process.

Industries & Business Types We Work With

Annual accounts preparation is relevant across virtually every sector of the UK economy.

Audit Consulting Group supports a wide range of businesses, including:

- limited companies;

- startups;

- SMEs;

- consultants and contractors;

- construction businesses;

- e-commerce companies;

- property companies;

- professional service firms;

- family-owned companies;

- dormant companies.

Although the underlying reporting principles remain broadly similar, different industries often create different year-end challenges.

A contractor company may require greater focus on dividends and director remuneration. An e-commerce business may involve multiple payment platforms and higher transaction volumes. A property company may face different reporting considerations relating to rental income, financing arrangements and asset ownership structures.

Understanding these operational realities helps create a more efficient and accurate annual accounts preparation process.

What Directors Often Underestimate Before Year-End

Many directors assume annual accounts are simply a compliance requirement that needs to be completed once each year.

In reality, annual accounts often reveal much more than a filing obligation. They provide insight into profitability, cash position, liabilities, director transactions and the overall financial health of the company.

One area frequently underestimated is the impact of director transactions.

Throughout the year, directors may pay company expenses personally, withdraw funds from the company, transfer money between personal and business accounts or declare dividends. Individually these transactions may seem routine. Collectively they can have a significant impact on year-end reporting.

Another common misconception is that accounting software automatically guarantees accurate records. Software can improve efficiency, but it cannot replace proper review, reconciliation and professional judgement.

Many year-end adjustments arise not because software failed, but because transactions were recorded incorrectly, inconsistently or without sufficient supporting information.

Director Loan Accounts, Dividends & Year-End Realities

Director loan accounts are one of the most common areas requiring attention during annual accounts preparation.

In owner-managed businesses, money often moves between the company and the director throughout the year. Without accurate records, it can become difficult to determine whether those movements represent loans, reimbursements, dividends, salary payments or business expenses.

Accurate records help support the appropriate reporting treatment and reduce uncertainty when year-end reviews take place.

Dividends create similar challenges.

Many directors understand that dividends can be tax-efficient when used appropriately. However, dividends should normally be supported by sufficient profits and documented correctly.

During year-end reviews, accountants frequently encounter situations where:

- director withdrawals have not been classified clearly;

- dividend records are incomplete;

- loan account balances require reconciliation;

- personal and business transactions have become mixed;

- historic balances need clarification.

These situations are common and often manageable. The key is identifying them early enough for the appropriate review and reporting treatment to be applied.

Why Similar Annual Accounts Projects Often Become Difficult

Most year-end reporting difficulties do not arise because annual accounts themselves are unusually complex.

More often, challenges develop because issues accumulate gradually throughout the year and are only discovered when the annual accounts review begins.

Common causes include:

- incomplete bookkeeping records;

- unreconciled bank accounts;

- missing documentation;

- unclear director loan balances;

- historic bookkeeping errors;

- late record collection;

- misunderstanding reporting obligations;

- lack of periodic financial review.

One practical observation is that many year-end problems could have been identified significantly earlier through regular financial reviews and stronger record-keeping procedures.

Businesses that maintain organised records throughout the year generally experience fewer surprises when annual accounts preparation begins.

Strategic Annual Accounts Guidance For Company Directors

Annual accounts should not be viewed solely as a statutory reporting requirement.

They also provide a valuable opportunity to assess the financial position of the company and identify areas where reporting processes may need improvement.

Directors reviewing their year-end reporting process often benefit from considering:

- whether accounting records accurately reflect business activity;

- whether bookkeeping systems remain suitable for the size of the company;

- whether director transactions are being recorded consistently;

- whether financial visibility is sufficient throughout the year;

- whether regular reporting could reduce year-end pressure.

Many growing businesses eventually supplement annual accounts with management accounts to improve visibility between year-end reporting periods.

Viewed strategically, annual accounts become more than a compliance document. They become an important reporting tool that helps directors understand how the business is performing and where future improvements may be needed.

Results, Compliance Outcomes & Business Impact

Well-prepared annual accounts provide benefits that extend beyond statutory reporting requirements.

While annual accounts are often viewed primarily as a compliance obligation, they also create an opportunity to assess the financial position of the company, review reporting processes and identify areas that may require attention before the next accounting period begins.

Businesses that maintain accurate records and prepare annual accounts properly often benefit from:

- greater confidence in financial reporting;

- improved visibility over business performance;

- more reliable year-end financial records;

- better preparation for Corporation Tax reporting;

- improved lender and finance readiness;

- reduced reporting uncertainty;

- stronger financial decision-making.

For many directors, the most valuable outcome is not simply receiving completed accounts. It is gaining a clearer understanding of how the business performed during the year and where future improvements may be required.

Accurate annual accounts also support wider business activities. Financial statements are often reviewed during lending applications, investment discussions, supplier due diligence processes and strategic planning exercises. Reliable reporting can therefore contribute to stronger operational decision-making as well as compliance.

Improved Case Studies — LTD Company Annual Accounts

Case 1: Micro-Entity Design Studio – Glasgow

A two-person design studio in Glasgow operating as a limited company with £145,000 annual turnover needed help preparing their first micro-entity annual accounts. Their bookkeeping was handled in spreadsheets and the Companies House filing deadline was approaching in less than two weeks.

Audit Consulting Group prepared and filed their LTD company annual accounts.

Our work included:

• Reviewing and reconciling 12 months of transactions

• Preparing micro-entity statutory accounts under FRS 105

• Calculating corporation tax for CT600 submission

• Filing accounts with Companies House

• Providing digital approval and confirmation

Results:

• Accounts prepared and filed within 4 working days

• Avoided late filing penalty of £150–£375

• Identified £3,100 in allowable business expenses

• Delivered clear year-end financial summary

Director feedback:

“They handled everything quickly and made the process incredibly simple for our first filing.”

Case 2: Online Retailer – Manchester

A growing e-commerce limited company in Manchester with £520,000 annual revenue and 1,200+ monthly transactions needed professional support preparing statutory annual accounts. Their Xero data required reconciliation before year-end reporting.

Audit Consulting Group completed full year-end accounts preparation.

Our work included:

• Reconciling 1,200 monthly transactions across payment gateways

• Preparing small company accounts under FRS 102 Section 1A

• Corporation tax calculation and submission to HMRC

• Companies House filing via approved software

• Financial reporting for director review

Results:

• Reduced year-end preparation time by 15+ hours

• Ensured full compliance with Companies House deadlines

• Identified £6,400 in tax-deductible expenses

• Delivered profitability insights for next financial year

Owner feedback:

“We finally had accurate year-end accounts and clear numbers for growth planning.”

Case 3: Dormant Holding Company – Reading

A dormant holding company with no trading activity needed to file statutory dormant accounts. The director was unaware of the requirement and had 72 hours before the filing deadline.

Audit Consulting Group prepared and submitted dormant LTD company annual accounts.

Our work included:

• Preparing dormant statutory accounts

• Verifying company inactivity

• Submitting accounts via Companies House WebFiling

• Setting up future deadline reminders

Results:

• Accounts filed within 24 hours

• Avoided £150 late filing penalty

• Maintained Companies House compliance

• Provided ongoing compliance tracking

Director feedback:

“I didn’t realise dormant companies still had to file. They sorted it within a day.”

What Happens After Annual Accounts Are Prepared?

Preparing annual accounts is often viewed as the end of the reporting process. In reality, it frequently becomes the starting point for the next financial year.

The completed accounts provide a structured overview of the company’s financial position and may influence future planning, borrowing decisions, dividend strategies, budgeting and broader business decisions.

Many businesses use the year-end review process to identify opportunities to strengthen bookkeeping procedures, improve reporting systems and increase financial visibility.

Others introduce additional support services such as Management Accounts to improve ongoing reporting or Bookkeeping Services to improve record quality throughout the year.

Annual accounts can also support wider compliance responsibilities, including Corporation Tax reporting and Companies House filing obligations.

Viewed this way, annual accounts become more than a compliance requirement. They become a valuable reporting tool that supports better business decisions and stronger financial management.

Communication, Ongoing Support & Future Reporting

Annual accounts preparation forms only one part of a company’s wider financial reporting framework.

As businesses evolve, financial reporting responsibilities often become increasingly interconnected.

Bookkeeping influences annual accounts. Annual accounts support Corporation Tax reporting. Payroll, VAT and director transactions can all affect the accuracy of year-end financial statements.

For this reason, many directors benefit from periodic financial reviews rather than focusing solely on year-end deadlines.

Regular communication and ongoing reporting support can help identify issues earlier, maintain stronger financial records and reduce the likelihood of unexpected problems emerging during annual accounts preparation.

Businesses that take a proactive approach to financial reporting often experience a smoother year-end process than those attempting to address reporting concerns only when statutory deadlines approach.

Why Businesses Choose Audit Consulting Group

Annual accounts preparation requires more than technical accounting knowledge. It requires an understanding of how financial records, reporting obligations and business activity interact throughout the year.

Audit Consulting Group supports UK limited companies with annual accounts preparation, bookkeeping, Corporation Tax compliance, financial reporting and wider accounting requirements.

One practical observation we encounter regularly is that many year-end reporting issues originate long before annual accounts preparation begins. Incomplete records, unreconciled balances, unclear director transactions and inconsistent reporting procedures often develop gradually throughout the year and become visible only during the year-end review.

This is why our approach focuses not only on preparing annual accounts but also on understanding the records behind them and helping directors identify areas where future reporting processes can be improved.

Clients value practical guidance, clear explanations and support that helps them understand both their compliance obligations and the financial information contained within their annual accounts.

Frequently Asked Questions

What are annual accounts for a limited company?

Annual accounts are financial statements prepared at the end of an accounting period that summarise a company’s financial position, financial performance and reporting position.

Are annual accounts the same as a Corporation Tax Return?

No. Annual accounts and Corporation Tax returns are separate reporting requirements. However, the financial information contained within the annual accounts is often used to support tax reporting.

What records are needed to prepare annual accounts?

Requirements vary but commonly include bookkeeping records, bank statements, invoices, payroll information, VAT records, dividend information and details of director transactions.

Do dormant companies need annual accounts?

In many circumstances, yes. Dormant companies often remain subject to statutory reporting requirements even where trading activity is limited or absent.

Can annual accounts be prepared if bookkeeping records are incomplete?

Often yes, although additional review, clarification and reconciliation work may be required before the accounts can be finalised accurately.

How long does annual accounts preparation take?

The timeframe depends on the complexity of the company, the quality of the records provided and whether additional review work is required.

Do annual accounts include director loan accounts and dividends?

Where relevant, director loan account balances, dividends and related transactions may form part of the annual accounts preparation process.

Do I need an accountant to prepare annual accounts?

Not every company is legally required to appoint an accountant. However, many directors choose professional support to help ensure reporting obligations are met and financial statements are prepared accurately.

Are annual accounts submitted to Companies House?

Annual accounts often form part of a company’s Companies House reporting obligations, although the preparation of annual accounts and the filing process are separate activities.

Official guidance for LTD company annual accounts:

Companies House annual accounts:

https://www.gov.uk/annual-accounts

Filing deadlines:

https://www.gov.uk/file-your-company-accounts-and-tax-return

Late filing penalties:

https://www.gov.uk/

Discuss Your Limited Company Annual Accounts

Whether you are preparing annual accounts for the first time, managing a growing business, reviewing year-end financial records or seeking support with statutory reporting requirements, understanding your obligations is an important part of running a limited company.

Audit Consulting Group supports UK limited companies with annual accounts preparation, bookkeeping, Corporation Tax reporting and wider financial compliance requirements.

If you would like to discuss your annual accounts, reporting responsibilities or the information required for year-end preparation, our team can help you understand the next steps and the most appropriate approach for your business.

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants