CT600 Form UK – Corporation Tax Return Filing & HMRC Guidance

Leave your details and our team will get back to you shortly.

Reviewed by the Audit Consulting Group Corporation Tax Team

The CT600 form is the official HMRC Corporation Tax Return used by UK limited companies to report taxable profits, calculate Corporation Tax liabilities, claim available reliefs, and confirm financial activity for a specific accounting period.

For many company directors, the process initially looks straightforward. HMRC sends a notice to file, accounting software produces figures, and the assumption is often that the return can simply be submitted online in a few minutes.

In reality, CT600 filing problems are far more common than many businesses realise.

Over the years, we have seen companies submit Corporation Tax Returns with incorrectly classified expenses, undeclared director loan balances, duplicated payroll figures after software migrations, missing supplementary schedules, or bookkeeping records that technically balanced but still created tax reporting issues later.

At Audit Consulting Group, we help UK businesses prepare and submit accurate CT600 Corporation Tax Returns while reducing the risk of penalties, HMRC enquiries, incorrect tax calculations, and costly compliance mistakes.

Our team provides professional CT600 Form services, including Corporation Tax filing support, amended returns, accounting adjustments, tax planning, bookkeeping corrections, and HMRC compliance assistance.

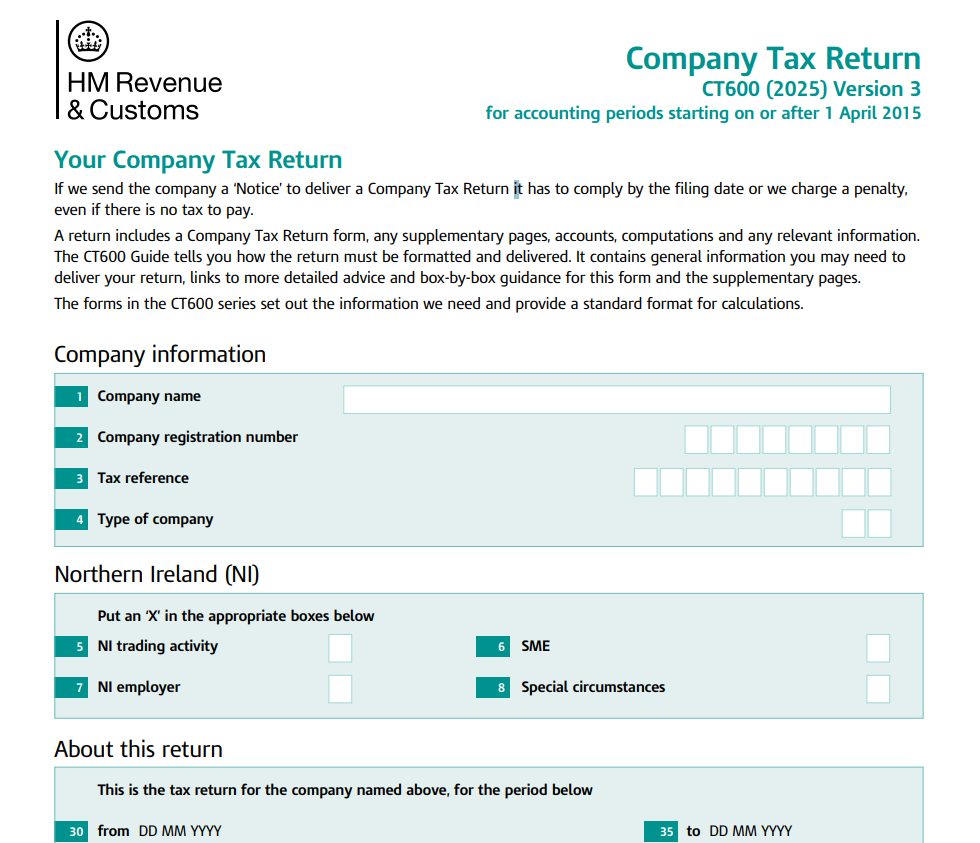

What Is the CT600 Form?

The form CT600 is the main Corporation Tax Return document submitted to HMRC by limited companies operating in the UK. It reports taxable profits, Corporation Tax liabilities, relief claims, losses, and financial activity relating to the company’s accounting period.

However, the actual filing process involves far more than simply entering figures into a form.

HMRC expects the return to align correctly with company accounts, bookkeeping records, payroll submissions, dividend declarations, director loan accounts, VAT activity, and supporting Corporation Tax computations submitted in iXBRL format.

One issue we regularly encounter is directors assuming that bookkeeping software automatically creates a fully compliant Corporation Tax Return. In practice, this is rarely the case. Software can produce accounting figures, but it does not always identify bookkeeping inconsistencies, incorrectly coded expenses, payroll duplication errors, or tax treatment issues that later create compliance risks.

For example, ecommerce businesses often struggle with CT600 submissions because payment platforms, Stripe settlements, PayPal fees, stock adjustments, and marketplace deductions are not always recorded consistently across bookkeeping systems. We have also seen businesses migrate from one accounting platform to another and accidentally duplicate opening balances or payroll journals without noticing until Corporation Tax calculations were already affected.

The CT600 submission may also include supplementary schedules such as:

- CT600A – loans to participators and director loan disclosures

- CT600B – charitable donations and related claims

- CT600C – group and consortium reliefs

For many growing businesses, the CT600 becomes one of the most important annual compliance filings because errors can affect tax liabilities, HMRC risk profiling, finance applications, and future accounting periods.

Who Needs to Submit a CT600 Corporation Tax Return?

Most UK limited companies registered with Companies House must submit a CT600 Corporation Tax Return to HMRC each year.

This usually includes:

- Active trading companies

- Companies temporarily inactive

- Non-UK businesses operating through a UK branch

- Community Interest Companies (CICs)

- Some charities and non-profit organisations with taxable activity

One of the most common misunderstandings we see involves dormant companies.

Directors often assume that because the business stopped trading or generated no profit, no Corporation Tax Return is required. Unfortunately, HMRC and Companies House do not always treat dormant status in exactly the same way.

We regularly assist companies that stopped trading months earlier but still received HMRC filing notices because dormant status had not been properly confirmed or previous accounting periods remained open.

Ignoring these notices usually leads to penalties first, and confusion later.

CT600 Deadlines & Corporation Tax Payment Dates

The filing deadline for the CT600 and the payment deadline for Corporation Tax are separate. Many businesses accidentally confuse the two and assume both dates are identical.

In most cases:

- The CT600 Corporation Tax Return must be submitted within 12 months after the end of the accounting period.

- The actual Corporation Tax payment is normally due 9 months and 1 day after the accounting period end.

Late filing penalties begin automatically from £100, but repeated delays or unresolved filing issues can increase compliance risk significantly.

Interestingly, many late submissions are not caused by directors intentionally ignoring deadlines. More often, businesses discover bookkeeping problems close to the filing date. Missing invoices, unresolved payroll discrepancies, director loan balances, duplicated transactions, or incomplete bookkeeping records can delay the final Corporation Tax computations considerably.

We have also seen situations where directors believed their previous accountant had already filed the return, only to later receive HMRC penalties because the submission was never completed successfully.

Official HMRC deadline guidance – Download CT600 PDF 2025

Why Companies Get CT600 Returns Wrong

After reviewing many Corporation Tax filings over the years, one thing becomes very clear: most CT600 problems are not caused by the form itself.

They usually begin much earlier.

Sometimes the bookkeeping is incomplete. Sometimes directors mix personal and business expenses unintentionally. Sometimes payroll journals are duplicated during software migrations. In other cases, dividends are recorded incorrectly or director loan balances remain unresolved for months without anyone noticing the tax implications.

We have also seen businesses relying entirely on bookkeeping software estimates without reviewing whether the figures actually reflect the commercial reality of the business.

A surprising number of Corporation Tax issues start when businesses grow quickly. More invoices, more payment platforms, more staff, more software integrations, and more transactions often create accounting inconsistencies that only become visible when preparing the CT600 submission.

In practice, many filing problems are discovered only a few days before the deadline, when there is limited time left to investigate discrepancies properly.

How to Submit a CT600 Form Correctly

Most companies now complete their CT600 online filing electronically using HMRC-compatible accounting software or approved filing systems.

However, the submission itself is only one stage of the process.

Before the return can be filed correctly, businesses normally need to:

Prepare company accounts, review bookkeeping accuracy, calculate taxable profits, assess allowable expenses, review payroll and dividend records, generate Corporation Tax computations, and produce iXBRL-tagged supporting documents suitable for HMRC submission.

Even where bookkeeping software appears accurate, manual review is still often required.

We regularly identify issues involving:

- incorrectly coded director expenses

- duplicate payroll journals after software migration

- VAT inconsistencies between bookkeeping systems and filed returns

- director loan balances creating additional tax exposure

- incorrect capital allowance treatment

- missing supporting schedules

HMRC systems can also reject submissions due to formatting issues, incomplete attachments, or inconsistencies between accounts and computations.

For many businesses, the technical filing itself takes only minutes. The real work usually happens before submission.

Common CT600 Filing Mistakes Businesses Make

Some Corporation Tax Return mistakes appear repeatedly across different industries and business sizes.

One recurring issue involves directors assuming that because bookkeeping software generated a profit figure, the CT600 must therefore be correct automatically. Unfortunately, accounting accuracy and tax accuracy are not always the same thing.

Another common problem occurs when businesses claim reliefs without sufficient supporting evidence. HMRC has become increasingly strict around some Corporation Tax relief claims, particularly where documentation is incomplete or expenditure classifications are unclear.

We also regularly see situations where:

- Companies House accounts do not fully match HMRC submissions

- director loans remain overdrawn for extended periods

- payroll liabilities differ from bookkeeping records

- dividends were declared incorrectly

- previous accountants filed incomplete submissions

- businesses miss filing notices after changing registered office addresses

In some cases, businesses discover the problem only after HMRC opens a compliance check or issues estimated Corporation Tax demands.

Real CT600 Filing Examples

Bookkeeping Migration Problem

A retail company migrated from QuickBooks to Xero during the financial year and accidentally duplicated payroll journals and opening balances during the transition. The issue initially went unnoticed because the bookkeeping software still produced balanced reports. During the CT600 preparation process, we identified the inconsistencies, corrected the records, and prevented the company from overpaying Corporation Tax.

Director Loan Account Issue

A small consultancy business had an overdrawn director loan account that had been sitting unresolved for several months. The director assumed the transactions were simply reimbursements. After reviewing the bookkeeping records and bank activity, we identified additional Corporation Tax implications that required adjustment before the CT600 submission could be completed correctly.

R&D Relief Amendment

A London software company approached us after their previous accountant submitted a CT600 without including qualifying development expenditure linked to an internal logistics platform. After reviewing payroll allocation, subcontractor costs and development records, we amended the Corporation Tax Return and secured just over £15,000 in additional R&D tax relief.

FAQ – CT600 Corporation Tax Return

Can HMRC reject a CT600 submission?

Yes. HMRC can reject Corporation Tax Returns where supporting accounts are missing, iXBRL formatting is incorrect, supplementary schedules are incomplete, or figures appear inconsistent.

In practice, businesses are often surprised because the accounting software itself may show no obvious warning before submission.

What happens if my accountant submitted incorrect figures?

This happens more often than many directors expect, especially where bookkeeping problems existed before the return was prepared.

In many cases, the CT600 can still be amended after submission. However, it is important to review the full accounting records properly rather than simply adjusting isolated figures without understanding the underlying issue.

Can I submit a CT600 without an accountant?

Technically yes, particularly for very small or dormant companies. However, many businesses underestimate the complexity involved once bookkeeping adjustments, director loans, payroll reconciliations, dividends, capital allowances, or relief claims become involved.

The filing itself is often the easy part. The accuracy of the supporting records is usually where problems begin.

Does HMRC investigate Corporation Tax Returns?

Yes. HMRC may open compliance checks where figures appear unusual, relief claims seem inconsistent, bookkeeping records do not align correctly, or repeated filing issues occur across multiple accounting periods.

Not every enquiry means wrongdoing. In many situations, HMRC simply wants additional clarification or supporting documentation.

How long should CT600 records be retained?

HMRC generally expects companies to retain accounting records, supporting documents, and Corporation Tax information for at least six years.

Why Businesses Choose Audit Consulting Group for CT600 Filing

At Audit Consulting Group, we support businesses with far more than basic form submission.

Our accountants work closely with directors to identify bookkeeping inconsistencies, review Corporation Tax exposure, resolve filing issues, and ensure the final CT600 submission reflects the actual financial position of the company accurately.

We regularly assist businesses with:

- CT600 Corporation Tax Return preparation and filing

- bookkeeping corrections before submission

- director loan reviews and tax adjustments

- amended Corporation Tax Returns

- Corporation Tax planning and relief claims

- HMRC correspondence and compliance support

- late filing resolution and penalty support

Many clients contact us after discovering problems created earlier in the bookkeeping or filing process. In those situations, the priority is not simply submitting the form quickly — it is making sure the underlying records and tax treatment are actually correct first.

Speak with our accountants today for professional support with your CT600 HMRC Corporation Tax Return.

CT600 Corporation Tax Return Services Cost & Pricing UK

We provide professional and affordable CT600 Corporation Tax Return services for UK limited companies.

Whether you need help with a standard annual filing, amended CT600 submission, late Corporation Tax Return, bookkeeping correction work, or more complex tax adjustments, our accountants can assist.

Our fixed-price CT600 services are designed to help businesses stay compliant, reduce HMRC risk, avoid unnecessary penalties, and gain confidence that their Corporation Tax Return has been prepared correctly.

Official HMRC Corporation Tax Return guidance

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants