Annual Accounts Services & Year-End Reporting Support in the UK

Leave your details and our team will get back to you shortly.

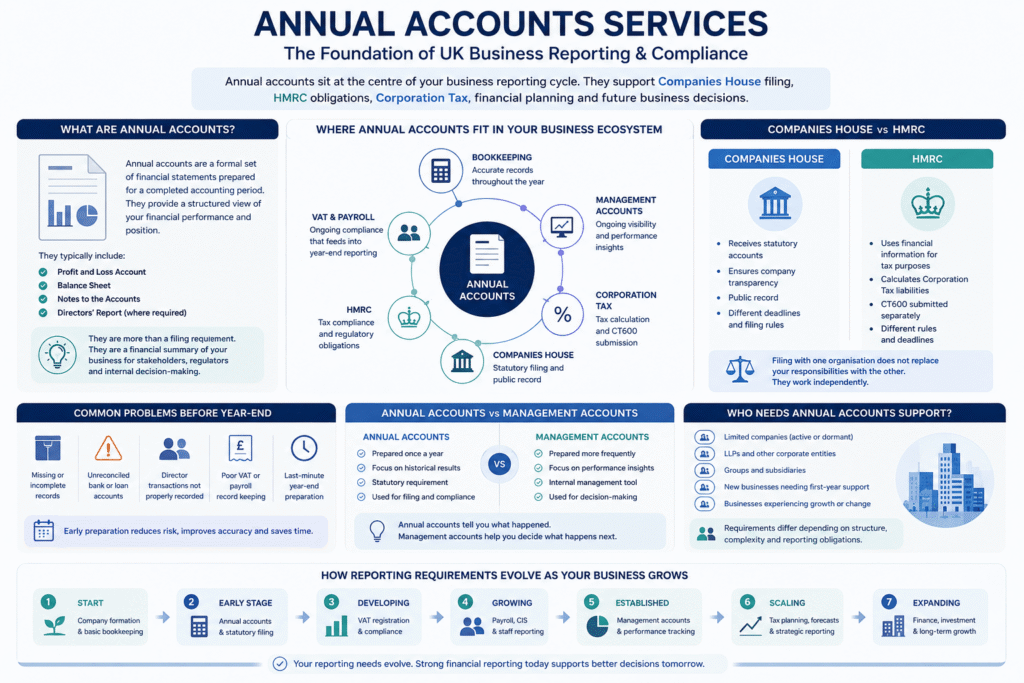

Annual accounts sit at the centre of a company’s financial reporting responsibilities. While many directors first encounter them as a Companies House requirement, annual accounts influence far more than a single filing deadline. They affect Corporation Tax reporting, dividend planning, lending applications, investor discussions, business valuations and the overall visibility directors have into company performance.

For some businesses, annual accounts are relatively straightforward. For others, they become the point where bookkeeping records, payroll data, VAT returns, director transactions and tax obligations all come together. The larger and more established a business becomes, the more interconnected these reporting requirements tend to be.

This guide explains how annual accounts fit within the wider UK accounting, tax and compliance ecosystem. It explores the different types of accounts businesses may need, how reporting obligations evolve over time, and how annual accounts connect with Companies House, HMRC, Corporation Tax, bookkeeping and ongoing financial management.

What Annual Accounts Actually Cover

Annual accounts are formal financial statements prepared for a specific accounting period. They provide a structured overview of a company’s financial position and form the foundation of statutory reporting for most UK limited companies.

Although often associated with compliance, annual accounts serve several purposes simultaneously. They help satisfy legal reporting obligations, support Corporation Tax calculations, provide transparency for shareholders and create a financial record that may later be reviewed by lenders, investors, auditors or potential buyers.

Depending on the reporting framework used and the size of the business, annual accounts may include:

- balance sheets;

- profit and loss statements;

- notes to the accounts;

- director-related disclosures;

- information regarding assets, liabilities and retained earnings;

- supporting schedules used within year-end reporting processes.

What many directors discover is that annual accounts rarely begin at year-end. The final statements depend heavily on decisions made throughout the year. Transaction categorisation, VAT treatment, payroll processing, asset purchases, loan movements and dividend decisions can all influence the accuracy of the final accounts.

As a result, annual accounts often become a reflection of the overall quality of a company’s financial records rather than simply a year-end exercise.

Where Annual Accounts Fit in the Business Reporting & Compliance Cycle

Annual accounts form part of a wider reporting cycle rather than an isolated filing event.

Most companies begin with incorporation and basic bookkeeping. As the business develops, additional obligations may appear. Some businesses register for VAT. Others begin employing staff and introduce payroll. Contractors may become subject to CIS requirements. Growing companies often implement management reporting to gain better visibility over performance between year-end periods.

Annual accounts bring these activities together into a single reporting framework.

A simplified lifecycle often looks like this:

- Company formation and Companies House registration;

- Bookkeeping and financial record keeping;

- VAT registration and VAT reporting where applicable;

- Payroll administration and PAYE reporting where applicable;

- Management reporting and internal financial reviews;

- Year-end adjustments and reconciliations;

- Annual accounts preparation;

- Corporation Tax calculation and HMRC reporting;

- Companies House filing obligations;

- Strategic planning for the next financial year.

This progression helps explain why annual accounts often reveal issues that originated months earlier. A discrepancy in bookkeeping, a payroll posting error or an unreconciled bank account may remain unnoticed until year-end reporting begins.

For directors, understanding this relationship is important because annual accounts do not exist independently of the systems and processes that support them.

Who Needs Annual Accounts Support?

Annual accounts are relevant to a wide range of UK companies, but the reasons for seeking support often vary.

Annual accounts are relevant to a wide range of UK companies, but the reasons for seeking support often vary.

Some directors simply want confidence that their reporting obligations have been handled correctly. Others need assistance because the business has become more complex than it was in previous years. In many cases, annual accounts preparation becomes part of a wider review of the company’s financial records.

Businesses that commonly seek annual accounts support include:

- newly incorporated limited companies approaching their first filing deadlines;

- owner-managed businesses with growing transaction volumes;

- companies operating across multiple sales channels or payment platforms;

- VAT-registered businesses requiring year-end reconciliation;

- employers with payroll obligations;

- dormant companies maintaining statutory compliance;

- groups of connected companies with intercompany transactions;

- businesses preparing for lending, investment or acquisition discussions;

- companies transitioning from basic bookkeeping towards more structured financial reporting.

Annual accounts can also become particularly important during periods of change. A company preparing for expansion, seeking finance or considering a future sale often requires a clearer understanding of its financial position than compliance reporting alone provides.

Types of Annual Accounts and Reporting Requirements

Not every company prepares the same type of annual accounts. Reporting requirements vary depending on company size, activity, accounting standards and statutory eligibility.

This distinction is important because many directors assume all companies follow the same reporting format. In practice, different businesses may qualify for different frameworks and disclosure requirements.

Micro-Entity Accounts

Many small owner-managed companies qualify for micro-entity reporting under FRS 105. These accounts are designed to simplify statutory reporting while still meeting Companies House requirements.

Although the filing format may be simplified, the underlying accounting records still require proper review. The reduced reporting format does not remove the need for accurate bookkeeping or year-end adjustments.

Small Company Accounts

Companies that exceed micro-entity thresholds may prepare accounts under FRS 102 Section 1A. These accounts generally involve broader disclosure requirements and often provide a more detailed picture of the business.

For directors, this can offer greater visibility into performance, retained profits and longer-term financial trends.

Dormant Company Accounts

Dormant companies remain subject to Companies House obligations even when trading activity is absent.

Many directors underestimate this point. A company may not be actively trading, but filing requirements can still continue. Understanding dormant status correctly is often more important than the filing itself.

Full Statutory Accounts

Medium-sized and larger businesses may require more detailed statutory reporting, particularly where lenders, investors, auditors or shareholders require greater financial transparency.

As companies grow, reporting expectations often increase alongside operational complexity.

Group Reporting Considerations

Where companies operate within a group structure, additional reporting considerations can arise. Intercompany balances, related party transactions and consolidation requirements frequently require a different level of review compared with a standalone business.

These situations rarely fit into a standard year-end process and often require broader consideration of how different entities interact financially.

Annual Accounts vs Management Accounts: Understanding the Difference

One of the most common misconceptions is that annual accounts and management accounts serve the same purpose.

They do not.

Annual accounts are primarily retrospective. They summarise what happened during a completed accounting period and support statutory reporting obligations.

Management accounts are forward-looking operational tools. They are usually prepared monthly or quarterly and help directors monitor performance throughout the year rather than waiting until year-end.

A business relying solely on annual accounts may identify issues after they have already affected profitability or cash flow. A business using management accounts can often spot trends earlier and make decisions before those issues become significant.

This is why many growing companies eventually move beyond basic annual reporting and introduce management accounts as part of their wider financial management process.

The two reporting functions are closely connected. Strong management reporting often leads to cleaner year-end accounts, while accurate annual accounts provide a stronger foundation for future management reporting.

Annual Accounts, Corporation Tax and Companies House: What Is the Difference?

Many directors use the terms annual accounts, Corporation Tax return and Companies House filing interchangeably. In practice, they refer to different reporting obligations involving different organisations, deadlines and purposes.

Annual accounts are the financial statements prepared for a completed accounting period. They form the foundation of year-end reporting and provide the figures used for both statutory reporting and tax calculations.

Companies House and HMRC then use this information in different ways.

Companies House is primarily concerned with statutory reporting and corporate transparency. HMRC focuses on taxation and the calculation of Corporation Tax liabilities.

This distinction becomes particularly important as businesses grow. A company may meet its Companies House filing obligations while still having separate Corporation Tax responsibilities with HMRC. Likewise, submitting a CT600 does not automatically satisfy Companies House requirements.

Understanding these differences helps directors avoid a surprisingly common problem: assuming that one filing automatically covers the other.

Businesses seeking detailed guidance on statutory filing obligations can explore Companies House Annual Accounts Filing, while companies specifically reviewing limited company reporting requirements may find LTD Company Annual Accounts more relevant.

Companies House vs HMRC Responsibilities

One of the biggest sources of confusion for new directors is understanding who receives what information and why separate deadlines exist.

One of the biggest sources of confusion for new directors is understanding who receives what information and why separate deadlines exist.

Companies House acts as the UK’s registrar of companies. Its role is to maintain official company records and ensure businesses meet their statutory reporting obligations.

HMRC is responsible for tax administration. Its focus is not corporate transparency but taxation, tax calculations and compliance with tax legislation.

Although annual accounts contribute to both processes, the organisations use the information differently.

In practical terms:

- Companies House receives statutory accounts;

- HMRC receives Corporation Tax returns and tax computations;

- Companies House focuses on filing compliance;

- HMRC focuses on tax compliance;

- directors remain responsible for ensuring both obligations are met.

As businesses become more complex, these reporting streams often become increasingly interconnected. Bookkeeping quality affects both statutory reporting and tax reporting. Payroll affects year-end figures and tax calculations. VAT reporting may influence reconciliations and financial disclosures.

This is why annual accounts preparation often sits at the intersection of accounting, compliance and tax rather than belonging exclusively to any one area.

Common Problems Businesses Face Before Year-End

Very few year-end issues appear suddenly. Most develop gradually throughout the accounting period and only become visible once annual accounts preparation begins.

Accountants frequently encounter situations where the bookkeeping appears complete at first glance but requires significant review before reliable accounts can be produced.

Common challenges include:

- unreconciled bank accounts;

- missing supplier invoices;

- duplicate transactions;

- incorrect VAT treatment;

- director loan accounts that have not been monitored consistently;

- payroll figures that do not align with accounting records;

- dividend payments lacking supporting documentation;

- asset purchases recorded as ordinary expenses;

- historic balances carried forward without investigation.

None of these issues are unusual. In fact, many occur within otherwise well-managed businesses.

The challenge is that they tend to surface at the point where filing deadlines are approaching and decisions need to be made quickly.

The earlier discrepancies are identified, the easier they are to resolve. Businesses that review their records regularly throughout the year often experience a far smoother annual accounts process than those relying entirely on a year-end review.

How to Choose the Right Annual Accounts Support

The level of support required is not always determined by company size.

A relatively small business may have multiple revenue streams, VAT obligations, payroll responsibilities and director transactions that create significant reporting complexity. Meanwhile, a larger company with well-maintained systems may require comparatively little intervention.

When evaluating annual accounts support, directors often benefit from considering several questions:

- Are bookkeeping records fully reconciled?

- Do VAT returns agree with accounting records?

- Are payroll figures recorded correctly?

- Have director loans been monitored throughout the year?

- Are there dividends or shareholder transactions requiring review?

- Will the accounts be used for lending, investment or strategic planning?

- Has the company experienced significant growth or structural changes?

The answers often determine whether straightforward preparation is sufficient or whether a broader year-end review becomes necessary.

Businesses frequently discover that annual accounts preparation becomes most valuable when it provides clarity rather than simply producing a filing.

Accounting Systems, Records and Software

Software has transformed how businesses maintain accounting records, but technology alone does not guarantee accurate reporting.

Software has transformed how businesses maintain accounting records, but technology alone does not guarantee accurate reporting.

Most year-end issues arise not because software failed, but because information was entered incorrectly, categorised inconsistently or left unreconciled.

Annual accounts preparation commonly involves reviewing information from systems such as:

- Xero;

- QuickBooks;

- Sage;

- Dext;

- Hubdoc;

- AutoEntry;

- payroll software;

- bank feeds;

- e-commerce platforms;

- payment processors.

As businesses grow, the challenge often shifts from collecting data to ensuring multiple systems work together consistently.

An e-commerce business, for example, may process transactions through several payment providers while maintaining separate inventory systems and VAT reporting requirements. A company with employees may need payroll records, pension information and year-end accounting figures to align correctly.

The more systems involved, the greater the importance of reconciliation and periodic review.

Timelines, Deadlines & Compliance Requirements

Annual accounts obligations are closely linked to statutory deadlines, but directors often underestimate how much preparation work may be required before filing becomes possible.

For most private limited companies, annual accounts must generally be filed with Companies House within nine months of the financial year-end. Corporation Tax returns are usually submitted to HMRC within twelve months of the end of the accounting period, while Corporation Tax itself is normally payable earlier.

The deadlines themselves are relatively straightforward. The challenge is that many of the tasks supporting those deadlines take place beforehand.

Bookkeeping reviews, reconciliations, payroll checks, VAT reviews, director loan analysis and year-end adjustments all need to be completed before reliable accounts can be finalised.

First-year companies often find this process particularly confusing because Companies House and HMRC may operate on different reporting timelines. Understanding how accounting periods, filing dates and tax deadlines interact is often more important than remembering the dates themselves.

Businesses that leave preparation until the final weeks before filing frequently encounter unnecessary pressure. Missing records, unresolved bookkeeping issues or incomplete reconciliations become far more difficult to address when statutory deadlines are approaching.

Good annual accounts preparation is rarely about working faster. More often, it is about allowing enough time for proper review and informed decision-making.

What Businesses Often Underestimate About Annual Accounts

Directors rarely underestimate the filing deadline itself. What is underestimated far more often is everything that sits behind the final set of accounts.

Annual accounts are frequently viewed as an end-of-year administrative task. In reality, they are the result of hundreds or thousands of decisions made throughout the accounting period. How transactions were categorised, whether bookkeeping was maintained consistently, how director withdrawals were recorded, whether VAT was applied correctly and how payroll was managed can all affect the final position.

This becomes particularly apparent in growing businesses. A company may begin the year with straightforward reporting requirements and finish the year operating across multiple sales channels, employing staff, using several software platforms and managing a wider range of financial obligations.

Another area that often surprises directors is the level of scrutiny annual accounts may receive beyond compliance purposes. Lenders, investors, grant providers, potential buyers and even prospective business partners frequently review year-end financial information before making decisions.

For this reason, annual accounts are often one of the most important business documents a company produces, even when they were initially prepared simply to satisfy statutory requirements.

How Annual Accounts Influence Business Decisions

Strong annual accounts do more than explain what happened during the previous financial year. They often shape decisions about what happens next.

Strong annual accounts do more than explain what happened during the previous financial year. They often shape decisions about what happens next.

Many directors use year-end reporting to assess whether current pricing remains sustainable, whether staffing levels are appropriate, whether borrowing remains affordable or whether additional investment is realistic.

Annual accounts can also highlight patterns that are difficult to see during day-to-day operations. Revenue may be increasing while margins decline. Turnover may look healthy while cash flow becomes more restricted. Costs may gradually rise without attracting attention until the full year is reviewed.

In practice, some of the most valuable conversations around annual accounts occur after the reporting has been completed. Directors begin asking questions about profitability, reserves, future tax exposure, dividend capacity and long-term planning.

This is often where annual accounts transition from a compliance exercise into a business management tool.

Annual Accounts and Dividend Planning

Dividend decisions are closely connected to year-end reporting, yet this relationship is often misunderstood.

Many owner-managed businesses operate with a combination of salary and dividends. While dividends can be an efficient way of extracting profits from a company, they must be supported by sufficient distributable reserves.

Annual accounts help establish whether those reserves exist and provide the financial evidence needed to support dividend decisions.

Where bookkeeping records are incomplete or management reporting is limited, directors can sometimes make assumptions about available profits that do not fully reflect the company’s true financial position.

This does not mean dividend planning should only happen at year-end. In many businesses, regular reporting throughout the year helps directors make more informed decisions long before annual accounts are finalised.

However, the year-end accounts remain one of the most important reference points when reviewing dividend strategy and retained earnings.

What Accountants Commonly Discover During Year-End Reviews

Every company is different, but certain themes appear repeatedly during year-end reviews.

One common example involves director loan accounts. Directors may pay company expenses personally, withdraw funds at different times throughout the year or transfer money between personal and business accounts without fully documenting the movements.

Another recurring issue involves software-generated bookkeeping records. Modern accounting platforms automate many processes, but automation can sometimes create a false sense of accuracy. Transactions may be processed efficiently while still being categorised incorrectly.

Businesses that grow quickly often encounter a different challenge. Processes that worked when turnover was modest may no longer provide enough control once transaction volumes increase. Reconciliation routines become more important, reporting becomes more complex and financial oversight requires greater structure.

Year-end reviews also regularly identify timing differences between bookkeeping, VAT reporting, payroll records and bank transactions. These are rarely signs of serious problems, but they often require investigation before reliable annual accounts can be produced.

Experienced accountants expect to encounter these issues. Their existence is not unusual. The important factor is identifying and resolving them before statutory filings are completed.

Why Similar Annual Accounts Processes Sometimes Go Wrong

When annual accounts preparation becomes stressful, the root cause is rarely the accounts themselves.

More often, difficulties arise because information arrives late, records have not been reviewed during the year or key decisions were made without sufficient documentation.

Businesses sometimes assume that bookkeeping, VAT, payroll and year-end reporting operate independently. In reality, weaknesses in one area often create consequences elsewhere.

A payroll discrepancy may affect year-end accounts. A bookkeeping issue may affect Corporation Tax calculations. An unreconciled balance may delay statutory filing.

Another common problem is waiting until a deadline is close before beginning the review process. At that stage, there is often limited time to investigate unusual balances, obtain missing records or address historical inconsistencies.

Well-managed annual accounts processes tend to involve regular record reviews throughout the year rather than relying entirely on a final deadline-driven exercise.

Strategic Buyer Guidance

Businesses evaluating annual accounts support often focus initially on filing requirements. While compliance is important, it is rarely the only consideration.

Directors may benefit from asking broader questions when reviewing support options:

- Will the accounts simply be prepared, or will the underlying records be reviewed?

- How are bookkeeping issues identified and resolved?

- Will Corporation Tax implications be considered alongside statutory reporting?

- Can the reporting process support future planning and decision-making?

- How will communication work if questions arise during the review?

- Are related services available if reporting requirements become more complex?

The most appropriate solution depends on the business itself. Some companies need straightforward filing assistance. Others require a wider review of accounting records, reporting systems and compliance processes.

Understanding this distinction often helps directors choose support that remains useful beyond a single filing deadline.

Real-World Client Scenarios & Outcomes

A Newly Incorporated Company Approaching Its First Reporting Cycle

A director launched a limited company and focused primarily on sales, customer acquisition and operational setup during the first year. Accounting records existed, but they had been maintained alongside the pressures of building the business.

As the first annual accounts deadline approached, questions emerged regarding accounting periods, Companies House obligations, Corporation Tax reporting and which records were required for year-end preparation.

The situation involved more than simply producing accounts. Bookkeeping records needed review, several transactions required clarification and reporting obligations needed to be mapped against the company’s first filing cycle.

The outcome was not just successful filing. The business entered its second year with a clearer reporting structure and a better understanding of future compliance requirements.

A Growing Company Moving Beyond Basic Bookkeeping

A business that had operated successfully for several years experienced significant growth. Revenue increased, staff numbers expanded and VAT registration had already become necessary.

Annual accounts preparation revealed that multiple systems were now contributing financial data, including bookkeeping software, payroll records and external sales platforms.

The challenge was not a lack of information but ensuring consistency between those information sources.

The review process highlighted several reconciliation issues that would have become increasingly difficult to resolve in future years. It also demonstrated that the company had reached the point where management reporting would provide additional value between year-end periods.

The broader lesson was that reporting requirements often evolve alongside business growth, even when day-to-day operations appear to be functioning smoothly.

A Dormant Company Maintaining Long-Term Compliance

Not every annual accounts engagement involves active trading.

Some directors retain dormant companies for future commercial opportunities, intellectual property ownership, investment activities or group structures.

Although activity may be limited, statutory responsibilities continue. Filing obligations remain, company records must be maintained appropriately and deadlines still require monitoring.

In these cases, the challenge is often understanding which obligations continue to apply despite the absence of trading activity.

With the correct reporting approach, compliance can usually remain straightforward while preserving flexibility for future use of the company.

Explore Related Annual Accounts Services

Annual accounts are often one part of a broader reporting and compliance framework. Depending on the size of the business, the quality of existing records and the complexity of reporting requirements, directors may also require support with related accounting and tax functions.

Businesses looking for more specific guidance can explore:

- Companies House Annual Accounts Filing for statutory filing obligations, submission requirements and filing deadlines.

- LTD Company Annual Accounts for reporting requirements specific to UK limited companies.

These services provide deeper coverage of individual reporting areas while this page remains focused on the wider annual accounts ecosystem and how different obligations connect throughout the business lifecycle.

Related Accounting & Tax Services

Annual accounts rarely exist in isolation. In most businesses, they rely on information generated throughout the year by other accounting, tax and compliance processes.

Related services commonly include:

- Bookkeeping Services to maintain accurate accounting records throughout the year;

- Corporation Tax Services for tax calculations, CT600 submissions and year-end tax compliance;

- Management Accounts for ongoing financial visibility and business performance monitoring;

- Payroll Services where employee or director remuneration affects reporting requirements;

- VAT Services where VAT registration and reporting form part of the accounting cycle;

- Company Formation Services for newly established businesses entering their first reporting period.

As companies evolve, it is common for reporting requirements to move across multiple service areas rather than remaining within a single compliance function.

What Happens After Annual Accounts Are Prepared?

For many directors, filing marks the end of the annual accounts process. From a business perspective, however, it is often the beginning of a new planning cycle.

The completed accounts provide a structured view of profitability, retained earnings, operating costs, liabilities, assets and overall financial performance. This information frequently influences decisions regarding recruitment, investment, borrowing, tax planning and future growth.

Some businesses use annual accounts as the foundation for management reporting in the following year. Others use the information to review dividend strategies, improve bookkeeping processes or prepare for external finance applications.

The most valuable outcome is often not the filing itself but the clarity the reporting provides.

When annual accounts are accurate and supported by reliable records, directors are generally in a stronger position to make informed decisions throughout the next financial year.

Communication, Deadlines & Ongoing Support

Annual accounts preparation rarely happens in a vacuum. Questions arise during the review process, additional records may be required and reporting obligations can change as a business develops.

This is particularly common during periods of growth, structural change or regulatory change.

A company that previously required only bookkeeping and year-end reporting may later need VAT support, payroll administration, management reporting or additional Corporation Tax planning.

Regular communication helps identify these changes before they become compliance issues.

It also helps businesses prepare for upcoming deadlines rather than reacting to them at the last moment. Filing deadlines, tax deadlines and reporting obligations become significantly easier to manage when viewed as part of a continuous process rather than isolated events.

Why Businesses Choose Audit Consulting Group

Businesses approach annual accounts from very different starting points. Some arrive with well-maintained records and established reporting systems. Others are dealing with their first filing cycle, historic bookkeeping issues or changing reporting requirements.

Audit Consulting Group works across accounting, tax and compliance disciplines, allowing directors to view annual accounts within the wider context of business reporting rather than as a standalone filing exercise.

This broader perspective often becomes valuable when annual accounts intersect with Corporation Tax, payroll, VAT, bookkeeping reviews, director remuneration planning or future growth objectives.

Our role is not simply to help businesses submit information. It is to help directors understand the reporting obligations behind that information, how different compliance requirements interact and where additional support may become relevant as the business evolves.

Because accounting requirements rarely remain static, many clients value having access to support that extends beyond a single reporting deadline.

Practical Reporting & Compliance Considerations

Annual accounts preparation is rarely just about producing a final set of figures. In many cases, the most important work happens before reporting begins. Reviewing bookkeeping records, reconciling balances, understanding director transactions and identifying inconsistencies often has a greater impact on reporting quality than the filing process itself.

Businesses also tend to experience different challenges depending on their stage of growth. A newly incorporated company may need guidance on deadlines and reporting responsibilities, while an established company may be focused on reporting quality, financial visibility and long-term planning.

Understanding these differences helps directors approach annual accounts as part of a wider reporting framework rather than a standalone compliance event.

Frequently Asked Questions

What are annual accounts?

Annual accounts are formal financial statements prepared for a completed accounting period. They support statutory reporting, Corporation Tax calculations and broader financial review.

Do all limited companies need annual accounts?

Most UK limited companies have annual accounts filing obligations, including many dormant companies.

Are annual accounts and Corporation Tax returns the same thing?

No. Annual accounts provide financial information. Corporation Tax returns are submitted separately to HMRC and are used to calculate tax liabilities.

Who receives annual accounts?

Companies House receives statutory accounts as part of corporate reporting obligations. HMRC may also use financial information as part of Corporation Tax reporting, but the reporting processes remain separate.

Can annual accounts be prepared if bookkeeping records are incomplete?

In many cases, yes. However, additional review, reconciliation and correction work may be required before reliable accounts can be produced.

What is the difference between annual accounts and management accounts?

Annual accounts focus on completed reporting periods and statutory obligations. Management accounts are typically prepared more frequently to support ongoing business decisions.

Do dormant companies still need to file accounts?

In most circumstances, yes. Dormant companies usually continue to have Companies House reporting obligations despite having little or no trading activity.

When should annual accounts preparation begin?

Many businesses benefit from beginning the review process well before statutory deadlines. Early preparation provides more time to resolve discrepancies and review reporting positions properly.

Can annual accounts help with business finance applications?

Yes. Lenders, investors and finance providers often review annual accounts when assessing applications, making accuracy and clarity particularly important.

UK filing requirements are governed by official regulatory bodies. You can review the requirements here:

Companies House filing deadlines:

https://www.gov.uk/annual-accounts

Corporation tax filing guidance:

https://www.gov.uk/file-your-company-accounts-and-tax-return

Making Tax Digital and digital records:

https://www.gov.uk/

Discuss Your Annual Accounts Requirements

Whether you are approaching your first reporting deadline, managing a growing company or reviewing year-end compliance responsibilities, understanding how annual accounts connect with bookkeeping, Corporation Tax, Companies House and wider business reporting can make future decisions considerably easier.

Audit Consulting Group supports UK businesses with annual accounts preparation, statutory reporting, Corporation Tax compliance and related accounting services. If you would like to discuss your reporting requirements or understand which obligations apply to your circumstances, our team can help you identify the next practical steps.

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants