HMRC CHV1 Form Assistance – Customs Value Declaration Support for UK Importers

Leave your details and our team will get back to you shortly.

When businesses import goods into the UK, HMRC expects the customs value of those goods to be declared accurately. That value directly affects how much import duty and import VAT will be charged during customs clearance.

Where valuation is straightforward, the customs declaration itself may be enough. However, when imports involve related companies, non-standard pricing, royalties, licensing arrangements, discounts or complex commercial structures, HMRC may require additional customs valuation information through the CHV1 HMRC form.

The HMRC CHV1 is used to explain how the customs value has been calculated and why that value should be accepted for customs and VAT purposes.

For many importers, customs valuation becomes more complicated as import activity grows. The customs value is not always the same as the supplier invoice price. Freight, insurance, commissions, royalties, licensing fees and related-party arrangements can all affect how HMRC reviews import duty and VAT exposure.

Proper completion of the HMRC CHV1 form is crucial for accurate import duty and VAT calculation in the UK. Customs Value Declaration Importance.

Quick Summary – What the HMRC CHV1 Actually Does

The CHV1 HMRC form helps HMRC understand and verify the customs value declared for imported goods entering the UK.

It may be required where the value is not straightforward, where HMRC needs more detail, or where the declared customs value could be affected by commercial arrangements between the importer and supplier.

The information provided through the HMRC CHV1 can affect import duty calculations, import VAT exposure, customs clearance decisions, HMRC reviews and future customs compliance risk.

Incorrect customs valuation can lead to underpaid duties, delayed imports, retrospective assessments or wider HMRC compliance investigations.

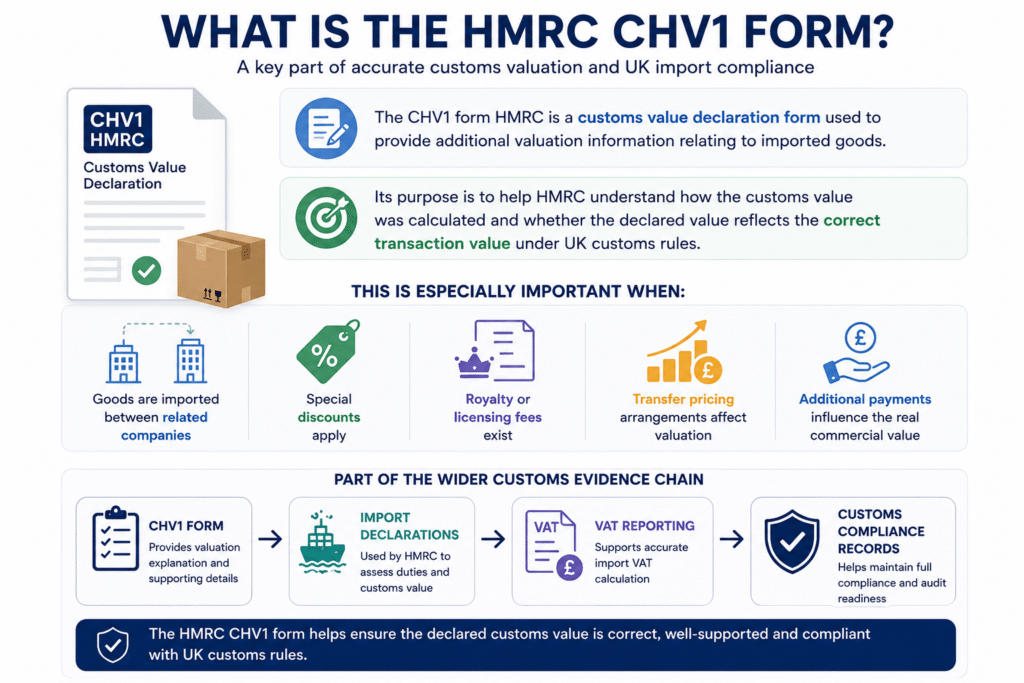

What Is the HMRC CHV1 Form?

The CHV1 form HMRC is a customs value declaration form used to provide additional valuation information relating to imported goods.

Its purpose is to help HMRC understand how the customs value was calculated and whether the declared value reflects the correct transaction value under UK customs rules.

This becomes especially important where goods are imported between related companies, special discounts apply, royalty or licensing fees exist, transfer pricing arrangements affect valuation, or additional payments influence the real commercial value of the imported goods.

In practice, the HMRC CHV1 form forms part of the wider customs evidence chain supporting import declarations, VAT reporting and customs compliance records.

Why Customs Valuation Matters More Than Many Businesses Realise

Many businesses initially assume customs value simply means the invoice price shown by the supplier.

In reality, customs valuation can become significantly more complex once businesses begin importing through group companies, overseas manufacturers, distributors or structured supply chains.

HMRC may review whether the declared value reflects genuine market value, whether additional charges should have been included, whether a relationship between buyer and seller affected pricing, and whether royalties, commissions, freight or insurance costs were treated correctly.

Small valuation inconsistencies can eventually create larger customs problems once import volume increases. Businesses importing regularly often underestimate how quickly valuation errors accumulate across multiple customs entries and VAT periods.

Who Normally Needs the HMRC CHV1?

The HMRC CHV1 is most commonly used by businesses importing goods from outside the UK where valuation is not completely straightforward.

This often includes businesses importing from related overseas companies, companies operating under transfer pricing arrangements, importers paying royalties or licence fees, businesses receiving discounted or non-market pricing, and companies with complex freight, insurance or commission structures.

For growing importers, customs valuation often becomes more important as supply chains become increasingly international and commercially complex.

Situations Where HMRC Commonly Requests Additional Valuation Information

HMRC may request a CHV1 form HMRC where customs declarations raise questions about how import values were calculated.

This often happens when declared values appear unusually low, related companies are involved in the transaction, commercial invoices do not fully explain the valuation method, or pricing structures include commissions, royalties or other adjustments.

Importers sometimes assume these requests automatically mean wrongdoing. In reality, HMRC may simply require additional evidence before accepting the declared customs value.

The problem is that businesses without organised documentation or a clear valuation methodology often struggle to respond effectively once HMRC enquiries begin.

Related-Party Imports and Transfer Pricing Risks

One of the most common reasons businesses require the HMRC CHV1 form is because imports take place between related companies.

For example, a UK subsidiary importing goods from an overseas parent company may operate under pricing structures influenced by transfer pricing policies, internal agreements or group-wide commercial arrangements.

HMRC may want to understand whether the relationship influenced the declared customs value and whether additional adjustments should be included. This is where customs valuation and corporation tax transfer pricing can overlap operationally.

These situations require careful documentation because the declared customs value must still be defensible for import duty and VAT purposes, even where group pricing policies exist.

Customs Valuation Adjustments Businesses Often Miss

One of the biggest customs valuation mistakes businesses make is assuming the supplier invoice alone determines the customs value.

In reality, HMRC may also review additional costs connected to the import transaction, including freight, insurance, commissions, licensing arrangements, royalties, packing costs, tooling charges or other commercial payments connected to the goods.

Where these adjustments are ignored, import duty and VAT may be underdeclared. That can create future HMRC exposure, especially if the same valuation method has been used repeatedly across multiple shipments.

Documents and Information Businesses Usually Need

Businesses preparing a CHV1 HMRC form normally require significantly more than a supplier invoice.

HMRC often expects supporting evidence showing how the customs value was calculated and whether all relevant commercial factors were included properly. This may involve commercial invoices, purchase contracts, shipping documentation, freight invoices, insurance records, royalty agreements, transfer pricing documentation and customs declarations.

For businesses importing goods regularly, organised digital customs records are far safer than fragmented spreadsheets, emails or paper files spread across different departments.

Common Mistakes and HMRC Customs Risks

Many customs valuation problems begin with relatively small reporting mistakes that gradually become larger compliance issues.

We regularly see businesses declaring only the invoice value without reviewing possible adjustments, failing to disclose related-party relationships, omitting royalty or licence fee information, submitting incomplete supporting documents, or using inconsistent customs valuation methods across different imports.

Once import activity increases, these inconsistencies can accumulate across multiple customs entries and VAT periods.

In larger businesses, customs valuation problems often remain hidden until HMRC begins reviewing historical import activity during customs audits or compliance checks.

Why HMRC Challenges Customs Values

HMRC does not automatically accept every declared customs value without review.

Where import values appear inconsistent, unusually low or commercially unclear, HMRC may request additional supporting evidence through customs valuation enquiries.

Common triggers include related-party imports, significant discounts, complex licensing arrangements, inconsistent invoices, missing valuation evidence or differences between customs declarations and bookkeeping records.

Once customs valuation questions arise, businesses without organised documentation often struggle to reconstruct the full valuation methodology retrospectively.

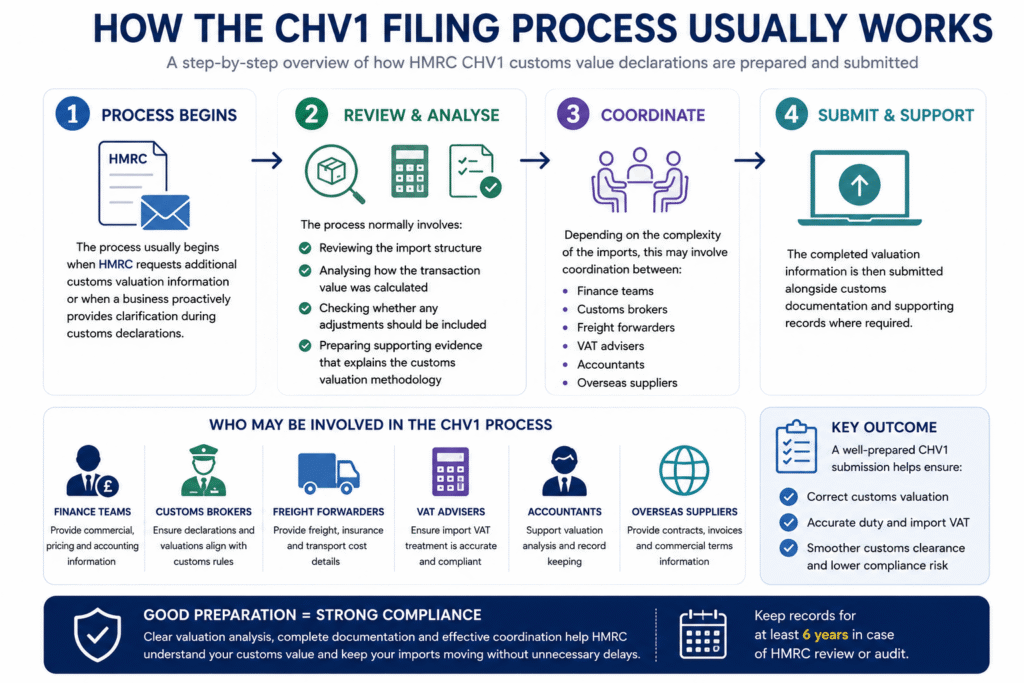

How the CHV1 Filing Process Usually Works

The filing process for the HMRC CHV1 usually begins when HMRC requests additional customs valuation information or where a business proactively provides clarification during customs declarations.

The process normally involves reviewing the import structure, analysing how the transaction value was calculated, checking whether any adjustments should be included, and preparing supporting evidence that explains the customs valuation methodology.

Depending on the complexity of the imports, this may involve coordination between finance teams, customs brokers, freight forwarders, VAT advisers, accountants and overseas suppliers.

The completed valuation information is then submitted alongside customs documentation and supporting records where required.

HMRC Rules, Audits and Record Retention

Businesses dealing with customs valuation should maintain organised import records for at least six years in case HMRC later reviews historical imports.

HMRC may request evidence showing how customs values were calculated, which costs were included, how related-party pricing was assessed, whether supporting contracts and invoices exist, and how bookkeeping records reconcile to customs declarations.

For importers processing large shipment volumes, poor document organisation can create serious operational pressure once HMRC reviews begin.

Online Systems, CDS and Customs Software

Modern customs reporting increasingly relies on digital customs systems and bookkeeping integration.

Businesses importing goods regularly often work across CDS customs systems, cloud bookkeeping software, freight forwarding platforms, digital VAT reporting systems, inventory tools and ERP platforms.

Once customs records become fragmented across several disconnected systems, valuation reconciliation becomes far more difficult operationally.

For growing importers, maintaining structured digital customs records is increasingly important for both VAT recovery and customs compliance management.

Related VAT and Customs Services

Businesses dealing with HMRC CHV1 issues often also require support with import VAT reconciliation, VAT Returns, customs record organisation and wider HMRC compliance matters.

Audit Consulting Group can also assist with VAT services, import VAT reviews, tax compliance support, customs bookkeeping, HMRC enquiry support and related-party reporting where customs valuation overlaps with wider business tax matters.

This is important because customs valuation problems rarely stay isolated. They often connect to VAT records, accounting systems, supplier contracts and future HMRC compliance exposure.

What Businesses Often Underestimate About Customs Valuation

Many businesses underestimate how quickly customs valuation becomes operationally sensitive once import activity scales.

The issue is rarely limited to customs duty alone. Incorrect customs values can affect import VAT calculations, cash flow forecasting, supply chain timing, bookkeeping reconciliation, profitability reporting and future HMRC audit exposure.

By the time customs inconsistencies become fully visible, historical reconciliation can become extremely time-consuming and expensive to correct retrospectively.

Why Customs Problems Escalate Over Time

Most customs valuation problems do not begin as serious compliance failures.

More commonly, businesses initially rely on incomplete documentation, simplified valuation assumptions or inconsistent customs processes that appear manageable at lower import volumes.

As imports increase, those inconsistencies spread across multiple customs entries, suppliers and reporting periods.

Eventually, businesses may discover that historical imports were undervalued, royalty costs were excluded incorrectly, customs declarations do not reconcile properly, or HMRC requires retrospective evidence for several years of import activity.

At that stage, reconstructing historical customs valuation evidence often becomes significantly more difficult operationally.

Strategic Customs and VAT Guidance

Businesses importing goods regularly should treat customs valuation as part of a wider tax and compliance strategy rather than simply an administrative customs requirement.

Import VAT, customs declarations, bookkeeping systems and transfer pricing structures often interact far more closely than businesses initially realise.

Professional customs valuation support can help businesses reduce customs dispute risk, improve import VAT accuracy, maintain organised customs evidence, reduce future HMRC audit exposure and improve reconciliation between customs and accounting records.

Real Importer Scenarios

Electronics Importer – Manchester

A UK electronics distributor importing goods from its overseas parent company received HMRC questions regarding customs values declared across several shipments.

After reviewing the import structure, we identified inconsistencies between transfer pricing documentation and customs valuation methods.

Result: revised valuation support was prepared, customs evidence was organised correctly and the business avoided wider customs escalation.

Fashion Retailer – London

A retail importer using overseas manufacturers failed to include royalty-related payments within customs valuation calculations.

During a customs review, HMRC requested additional supporting evidence explaining the pricing structure and valuation methodology.

Outcome: documentation was reconstructed, customs reporting corrected and future import processes strengthened significantly.

Construction Supplier – Birmingham

A construction materials importer struggled with inconsistent freight and insurance treatment across customs declarations submitted by different freight agents.

We reviewed customs records, bookkeeping systems and valuation methodology before implementing a more structured customs reporting process.

Result: customs reconciliation improved substantially while the business gained clearer operational visibility across future imports.

Ongoing Customs Compliance and Future Filings

Businesses importing goods regularly should view the HMRC CHV1 form as part of a wider customs compliance framework rather than a one-off declaration.

As import activity grows, businesses often require ongoing customs valuation review, VAT reconciliation support, import documentation management, customs bookkeeping alignment, HMRC enquiry support and future customs compliance monitoring.

Maintaining organised customs systems early usually reduces the risk of larger customs and VAT problems developing later.

Why Businesses Choose Audit Consulting Group

At Audit Consulting Group, we help UK businesses prepare accurate CHV1 HMRC forms, organise customs valuation records and maintain compliant import reporting systems.

We support businesses dealing with customs valuation disputes, import VAT inconsistencies, related-party import structures, freight and customs reconciliation issues, HMRC customs enquiries and ongoing customs compliance management.

Our team understands that customs valuation is not simply about filling out forms. It requires operational understanding of imports, VAT reporting, bookkeeping systems and customs evidence management.

FAQ – HMRC CHV1 Form

Is the HMRC CHV1 required for all imports?

No. The HMRC CHV1 is generally required where customs valuation is more complex or where HMRC requests clarification regarding the declared customs value.

Can the CHV1 form be submitted online?

The CHV1 HMRC form is generally submitted alongside customs documentation or as part of HMRC customs correspondence where required.

How long should customs valuation records be retained?

Businesses should normally retain customs valuation records and supporting documentation for at least six years.

What happens if customs values were declared incorrectly?

Incorrect customs values can lead to additional import duty, VAT adjustments, penalties or wider HMRC customs investigations.

Can Audit Consulting Group help prepare HMRC CHV1 forms?

Yes. We assist businesses with customs valuation analysis, CHV1 preparation, import documentation review and HMRC customs compliance support.

Need Help with HMRC CHV1 Customs Valuation Issues?

Customs valuation problems can become expensive surprisingly quickly once businesses lose visibility over import pricing, customs records and VAT reporting.

At Audit Consulting Group, we help businesses prepare compliant customs value declarations, resolve valuation problems and maintain organised customs reporting systems designed for long-term HMRC compliance.

Whether you need help with related-party imports, customs valuation disputes, import VAT reconciliation or ongoing customs compliance support, our team is ready to assist.

Speak with Audit Consulting Group today.

HMRC CHV1 Customs Value Declaration Services Cost UK

Get professional support preparing HMRC CHV1 customs value declarations, reviewing import VAT exposure and maintaining compliant customs valuation records in the UK. We help businesses organise customs evidence, resolve valuation issues and reduce HMRC customs compliance risk.

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants