HMRC C79 Explained – Import VAT Certificate for VAT Reclaims

Leave your details and our team will get back to you shortly.

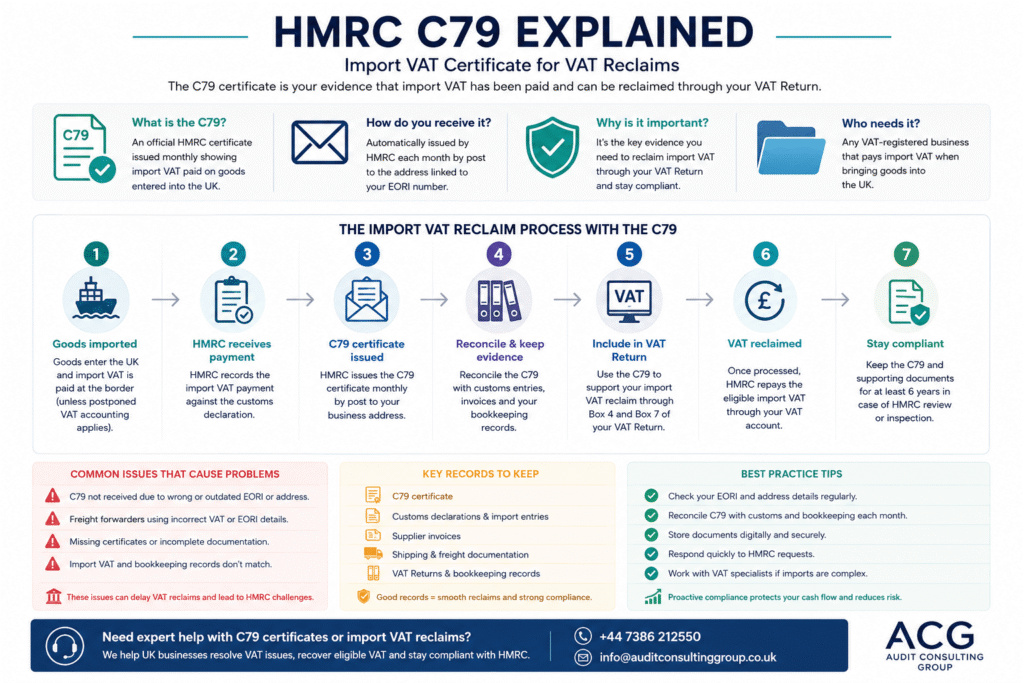

When businesses import goods into the UK, import VAT is often paid during customs clearance through freight agents, customs brokers or direct import declarations. In order to reclaim that VAT through a VAT Return, HMRC issues an official document known as the HMRC C79 certificate.

Many businesses incorrectly assume the C79 HMRC form is a reclaim application. In reality, it is not a claim form at all. The certificate acts as evidence confirming that import VAT has already been paid and may potentially be reclaimed through the VAT Return.

Without a valid HMRC C79, businesses can experience significant problems recovering import VAT correctly. Missing certificates, incorrect EORI details, poor bookkeeping reconciliation and customs reporting errors often create wider VAT compliance issues that become increasingly difficult to correct later.

Businesses importing goods regularly frequently underestimate how quickly import VAT reporting becomes operationally complex once import volume increases across multiple suppliers, freight agents and customs entries.

Need support with VAT reclaims or import VAT compliance? Our VAT Services, Tax Refunds & Reclaims and Personal Tax Filing services help businesses maintain compliant VAT records and recover eligible VAT correctly.

Quick Summary – What the HMRC C79 Actually Does

The C79 HMRC certificate acts as official proof that import VAT was paid to HMRC on imported goods entering the UK.

The certificate is usually issued monthly and contains information linked to customs declarations, VAT registration details, import references and the amount of import VAT paid during that reporting period.

Businesses normally use the information shown on the HMRC C79 form to support VAT recovery through their VAT Return.

Importantly, the certificate does not replace bookkeeping records, invoices or customs declarations. It forms part of the wider VAT evidence chain HMRC may review during compliance checks or VAT inspections.

What Is the HMRC C79 Certificate?

The C79 form VAT certificate is an official monthly document issued by HMRC to VAT-registered businesses that have paid import VAT on goods entering the UK.

The certificate confirms that import VAT has already been paid and can potentially be reclaimed through the business VAT Return. It normally includes customs entry references, VAT details, EORI information and the total import VAT paid during that reporting period.

For businesses importing goods regularly, the HMRC C79 becomes one of the most important VAT evidence documents retained within accounting records. Without it, reclaiming import VAT can become extremely difficult during HMRC reviews or VAT inspections.

Who Normally Receives a C79 HMRC Certificate?

The C79 HMRC form is usually issued to the VAT-registered importer listed on the customs declaration.

In practice, this means the certificate is connected to the VAT number and EORI number used when the goods entered the UK. Problems often appear when freight forwarders or customs agents accidentally use incorrect details during import processing. In those situations, businesses may discover the certificate was issued to the wrong entity or not issued correctly at all.

This is one of the main reasons importers should review customs documentation carefully instead of assuming freight paperwork has been processed accurately automatically.

How Import VAT and the C79 Work Together

When goods are imported into the UK, import VAT is often charged during customs clearance unless postponed VAT accounting is being used.

Once HMRC confirms the VAT payment, the business may later receive a C79 form HMRC certificate confirming the import VAT amount linked to those customs entries. The business can then use that certificate as supporting evidence when reclaiming VAT through the VAT Return.

In reality, the process is often more complicated than businesses initially expect because several different systems and parties may be involved at the same time. Freight forwarders, customs brokers, bookkeeping records, customs declarations and VAT reporting systems all need to align correctly for the reclaim process to remain smooth and compliant.

This is why import VAT reconciliation often becomes increasingly difficult once businesses begin importing goods regularly from multiple overseas suppliers.

Situations Where Businesses Usually Need the HMRC C79

Many businesses only realise how important the HMRC C79 certificate is once they attempt to reclaim VAT and discover supporting evidence is missing.

The certificate is commonly required when preparing VAT Returns, reconciling import VAT against customs declarations, reviewing freight documentation or responding to HMRC compliance checks.

Businesses also often need historical C79 certificates during bookkeeping cleanup projects, VAT audits or situations where import records no longer reconcile correctly across accounting systems.

For companies importing goods regularly, missing certificates can eventually create substantial VAT recovery problems if reporting systems are not properly organised.

Special Cases Businesses Often Encounter

Import VAT reporting is not always straightforward.

One common issue occurs when freight forwarders accidentally process imports using incorrect VAT or EORI details. This can prevent the correct business from receiving the HMRC C79 certificate entirely.

Another frequent area of confusion involves postponed VAT accounting. Some businesses expect to receive a traditional C79 form VAT certificate even though VAT has instead been accounted for through postponed VAT accounting statements.

We also regularly see businesses struggling with customs declarations that no longer match bookkeeping records, outdated addresses linked to EORI registrations or missing certificates discovered years later during VAT reviews.

These situations often become far more difficult to resolve once import activity increases and bookkeeping records become fragmented across multiple systems.

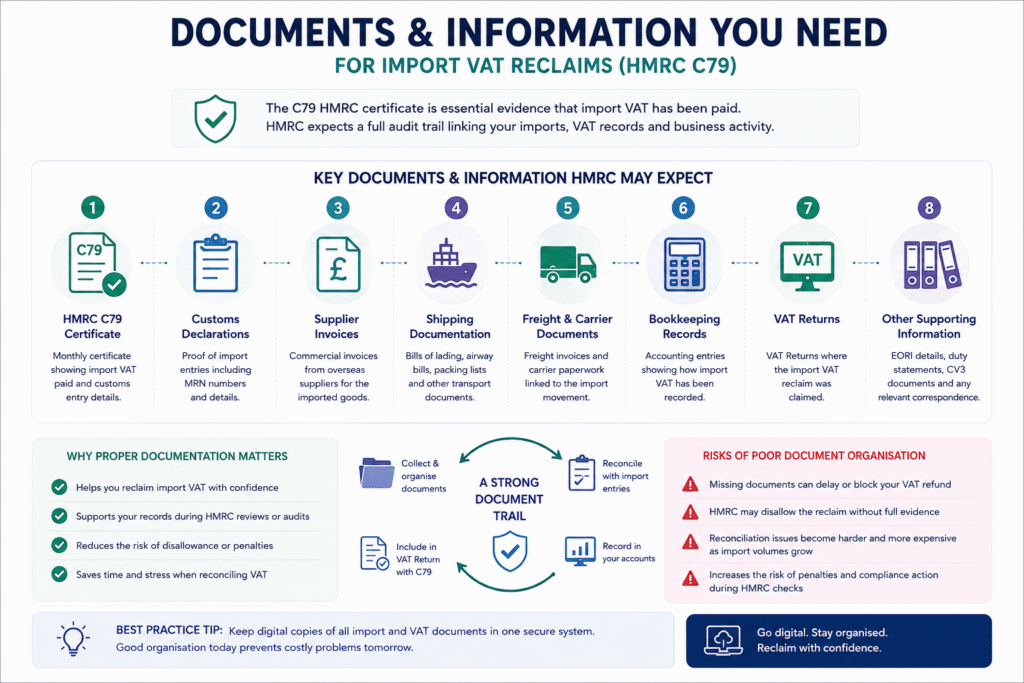

Documents and Information Businesses Usually Need

Businesses dealing with import VAT reclaims usually require far more than just the C79 HMRC certificate itself.

HMRC may also expect supporting records showing how import VAT connects to actual business activity and VAT reporting. This often includes customs declarations, supplier invoices, shipping documentation, bookkeeping records, VAT Returns and freight paperwork linked to the import entries.

Businesses importing goods frequently should ideally maintain organised digital accounting records rather than relying on paper files or fragmented spreadsheets spread across several systems.

Once import volumes increase, poor document organisation can quickly create reconciliation problems that become extremely time-consuming to correct retrospectively.

Common Mistakes and HMRC Risks

One of the biggest misconceptions surrounding the HMRC C79 form is assuming VAT can still be reclaimed without proper supporting evidence.

HMRC expects businesses to maintain a clear audit trail linking customs declarations, bookkeeping records, VAT Returns and import VAT evidence together consistently.

Problems often appear when businesses lose certificates, use incorrect EORI details, reclaim VAT using incomplete records or allow bookkeeping systems to become inconsistent over time.

In larger businesses importing goods regularly, these issues may remain unnoticed for months or even years before eventually appearing during HMRC compliance checks or VAT inspections.

Once reporting inconsistencies accumulate across customs entries and accounting systems, reconstructing the full VAT evidence chain retrospectively becomes significantly more difficult.

Why HMRC VAT Problems Escalate

Import VAT problems rarely begin as major compliance failures.

More often, they start with relatively small reporting inconsistencies that gradually become harder to correct over time.

For example, businesses may initially miss a single certificate, rely on incomplete freight paperwork or fail to reconcile import VAT correctly inside bookkeeping systems. As import activity increases, these gaps create larger reporting inconsistencies between customs records, VAT Returns and accounting systems.

Once HMRC begins reviewing import VAT evidence, businesses without organised records often struggle to reconstruct the full audit trail retrospectively.

This is one of the main reasons businesses importing goods regularly benefit from maintaining structured VAT reporting systems from the beginning rather than waiting until compliance issues appear.

How the VAT Reclaim Process Usually Works

The VAT reclaim process involving the HMRC C79 normally begins after import VAT has already been paid during customs clearance.

Once the certificate is received, businesses usually reconcile the import VAT amount against customs entries, bookkeeping records and freight documentation before including the reclaim within the relevant VAT Return.

The reclaim itself is typically reflected through Box 4 for input VAT recovery and Box 7 for purchases and expenses where applicable.

However, businesses should remember that the reclaim process is not simply about entering figures into a VAT Return. HMRC may still request supporting documentation later, particularly where import activity is substantial or bookkeeping records contain inconsistencies.

Online Systems, HMRC Records and Import Software

Although the traditional C79 HMRC certificate is still normally issued by post, import VAT reporting now interacts with several digital accounting and customs systems simultaneously.

Businesses importing regularly often rely on cloud bookkeeping software, customs declaration systems, freight forwarding platforms and digital VAT reconciliation tools to manage reporting more efficiently.

As import volumes increase, fragmented bookkeeping records can quickly create operational and compliance problems. This is especially common where customs declarations, VAT Returns and accounting systems are not properly integrated together.

For growing businesses importing internationally, maintaining accurate digital import VAT records becomes increasingly important for both VAT recovery and long-term compliance management.

What Businesses Often Underestimate About Import VAT

Many businesses assume import VAT administration is relatively straightforward until they begin dealing with missing certificates, customs discrepancies or delayed VAT recovery.

One of the biggest risks is poor record organisation.

Businesses importing goods regularly may accumulate substantial reclaimable VAT across dozens or hundreds of customs entries. Once bookkeeping systems become fragmented, businesses can quickly lose visibility over which VAT amounts were reclaimed, which certificates are missing and whether customs declarations still match accounting records correctly.

By the time these issues become visible, VAT reconciliation often becomes significantly more difficult and time-consuming.

Real Business Scenarios

Electronics Importer – Manchester

A UK electronics importer regularly importing products from China discovered several months of import VAT could not be reconciled properly because customs declarations and bookkeeping records no longer matched consistently.

After reviewing the business records, we identified missing import references, incorrect freight documentation and delayed bookkeeping reconciliation.

Result: over £12,000 of import VAT was successfully reconciled and reclaimed correctly through revised VAT reporting.

Retail Business – London

A retail company failed to receive several C79 HMRC forms because the address linked to the EORI registration had not been updated after relocation.

As a result, VAT recovery was delayed and import bookkeeping records became increasingly inconsistent internally.

Outcome: replacement certificates were obtained, VAT records were corrected and the business restored organised import VAT reporting systems.

Construction Supplier – Birmingham

A construction materials supplier importing goods regularly through freight agents experienced ongoing reconciliation problems because import entries were processed under inconsistent customs references.

We reviewed VAT records, customs documentation and bookkeeping systems before restructuring the import VAT reconciliation process.

Result: reporting accuracy improved significantly and the business gained clearer visibility over import VAT recovery across future VAT periods.

Ongoing VAT Compliance and Future Filings

Businesses importing goods regularly should view the HMRC C79 certificate as part of a wider VAT compliance system rather than an isolated form.

As import activity grows, businesses often require ongoing VAT reconciliation, digital bookkeeping support, customs record organisation and stronger VAT review processes to maintain accurate reporting consistently.

Maintaining organised import VAT systems early usually reduces the risk of larger VAT recovery and compliance problems developing later.

Why Businesses Choose Audit Consulting Group

At Audit Consulting Group, we help businesses manage import VAT records, reconcile C79 certificates and maintain organised VAT reporting systems designed for ongoing HMRC compliance.

We support businesses dealing with missing certificates, VAT reclaim problems, freight documentation issues, bookkeeping inconsistencies and wider customs reporting problems.

Our team understands that import VAT reporting is not simply about submitting forms. It requires accurate bookkeeping, organised documentation and clear visibility across customs records, VAT Returns and accounting systems.

FAQ – HMRC C79

Can I reclaim VAT without the C79 certificate?

Normally, HMRC expects businesses to hold the C79 HMRC certificate as supporting evidence when reclaiming import VAT through VAT Returns.

How do I request a duplicate C79?

Businesses can request replacement certificates directly through HMRC guidance here:

Request replacement C79 certificates

Is the C79 available online?

Traditional C79 certificates are generally issued by post rather than downloaded directly online.

What happens if customs entries use the wrong EORI number?

Incorrect EORI information can create VAT reclaim problems because the certificate may not be issued to the correct entity.

Can Audit Consulting Group help with missing C79 forms and VAT reconciliation?

Yes. We help businesses review import VAT records, reconcile VAT reporting issues and organise supporting documentation for HMRC compliance purposes.

Need Help Resolving HMRC C79 or Import VAT Problems?

Import VAT problems can become expensive surprisingly quickly once businesses lose visibility over customs records, bookkeeping systems and VAT evidence.

At Audit Consulting Group, we help UK businesses organise import VAT reporting, resolve C79 issues and maintain compliant VAT reclaim processes that support long-term financial control.

Whether you need help with missing certificates, VAT reconciliation, customs documentation or ongoing VAT compliance support, our team is ready to assist.

Speak with Audit Consulting Group today.

Official HMRC guidance:

https://www.gov.uk/guidance/get-your-import-vat-certificates

HMRC C79 VAT Certificate Services Cost & Pricing in the UK

Get professional support with HMRC C79 certificates, import VAT reconciliation and VAT reclaim reporting in the UK. We help businesses organise VAT evidence, review import VAT records and maintain HMRC-compliant reporting processes for ongoing VAT recovery.

Service Cost Estimation

Select the service category below to calculate the estimated cost of either accounting & tax services or forms and submissions.

Select Required Services / Forms

Select one or more services/forms to receive an accurate cost estimate. You can adjust your selection at any stage.

How would you like to engage our services?

Please select whether you require a one-off service or ongoing monthly support.

Contract Duration

Your cost estimate

Apply now and get 10% OFF

Submit your request today and receive an exclusive 10% discount on your selected service.

All prices are estimates. To receive a personalised quote, please fill out the form or contact us.

Ready to get started?

Get professional support from experienced UK accountants