HMRC Red Flags: Why Businesses Get Flagged and How to Avoid Common Compliance Mistakes

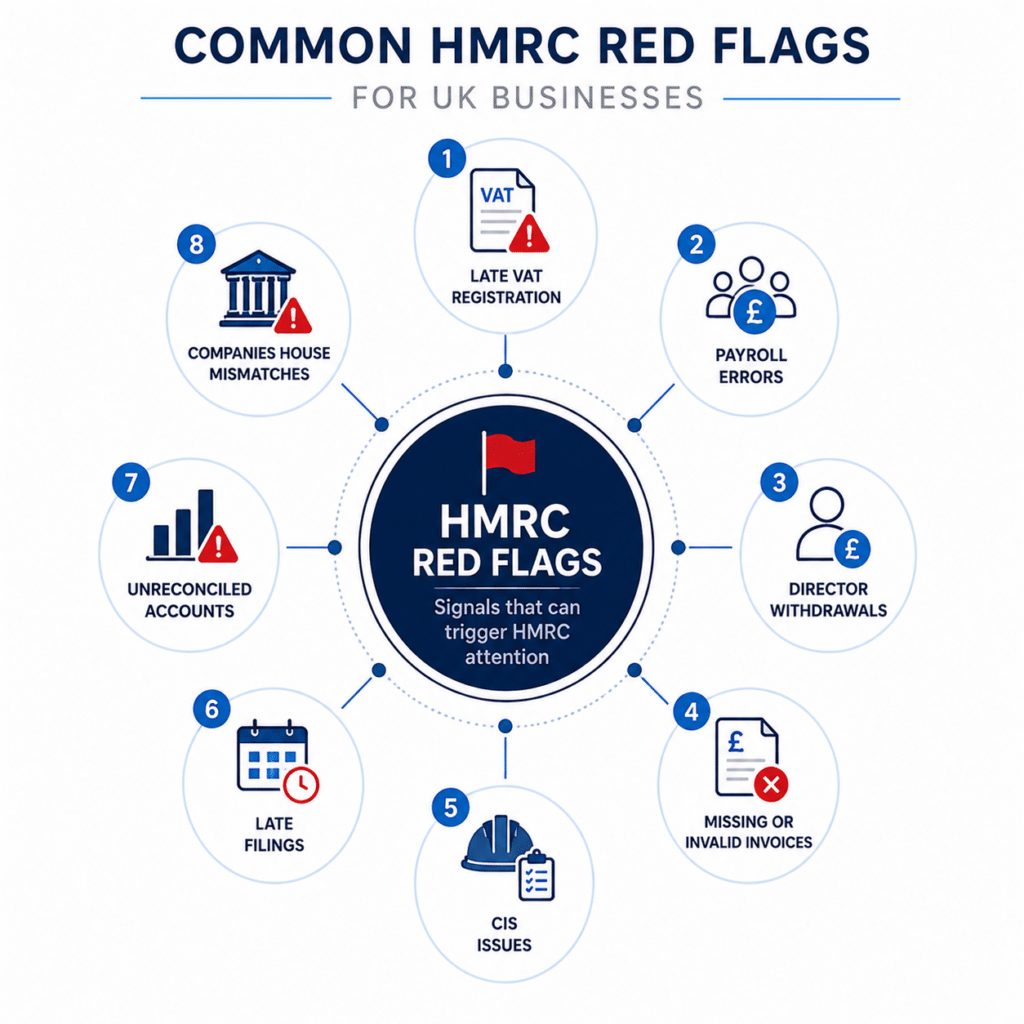

HMRC rarely needs a dramatic event to start asking questions. More often, a business is flagged because small inconsistencies accumulate: a VAT return that does not match turnover, PAYE submissions that do not reconcile with accounts, director withdrawals that have not been properly explained, CIS records that are thin, or bank activity that does not sit comfortably with the figures submitted.

For most UK businesses, the real risk is not deliberate wrongdoing. It is administrative drift. Sales grow, staff are added, cash flow becomes tighter, bookkeeping is done later than planned, and tax filings begin to rely on assumptions rather than clean records. That is often where HMRC problems begin.

This article explains the common traps that lead businesses to be flagged by HMRC, why they happen, what the practical consequences can be, and how directors, finance teams and business owners can reduce the risk of penalties, enquiries and avoidable disruption.

How HMRC tends to spot risk

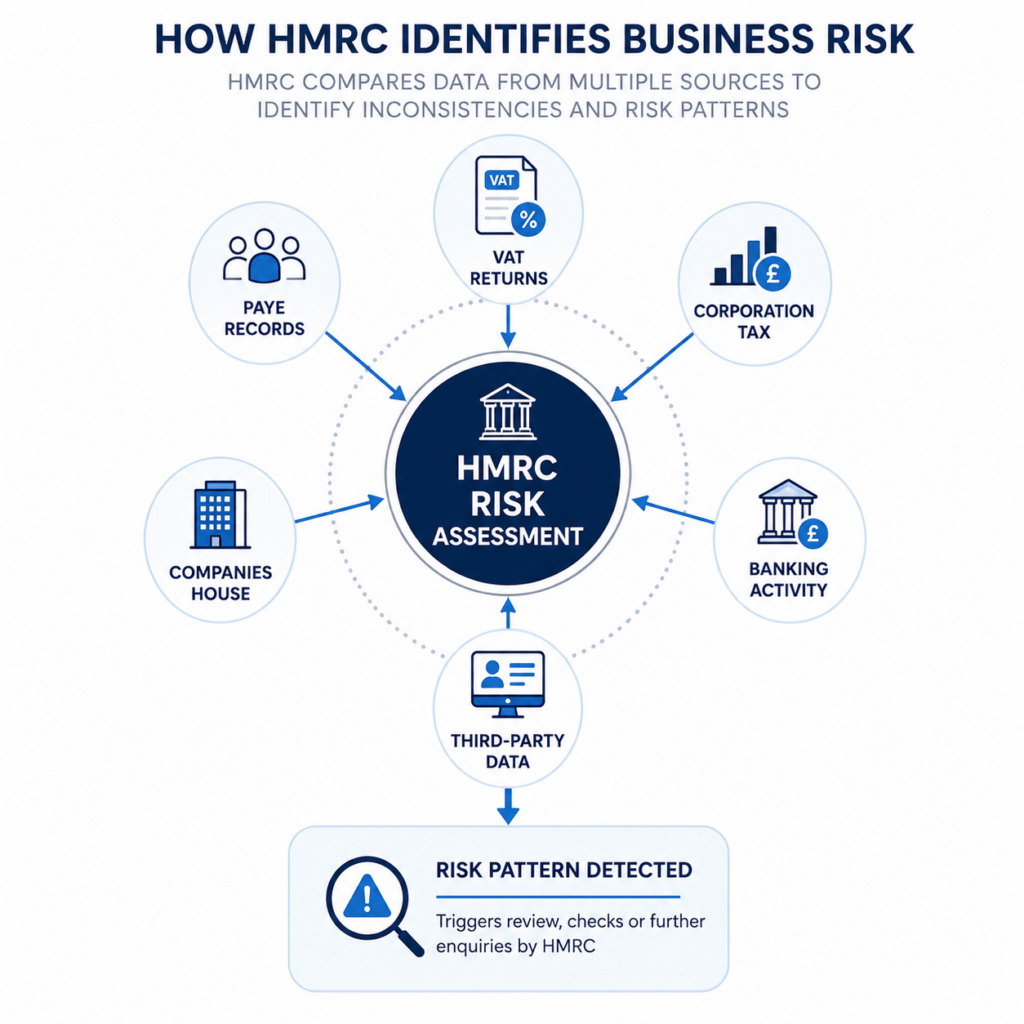

HMRC does not review every business manually in the same way. Risk is often identified through data comparison, filing history, sector patterns, third-party information and inconsistencies between different taxes. A company may appear low risk for years, then become more visible because one area no longer fits the wider picture.

Examples include VAT returns that show unusually low output tax compared with reported income, PAYE submissions that do not align with staff costs in the accounts, sudden VAT repayment claims after a long period of payments, or Corporation Tax returns that show persistent losses while the business continues to expand. None of these automatically proves an error, but they can justify further attention.

HMRC also receives and compares information from banks, payment processors, Companies House, employers, pension providers, online platforms and other government systems. The practical message is simple: tax compliance is not assessed only from the form a business submits. It is assessed against the surrounding evidence.

The problem is often mismatch, not one isolated mistake

One late filing can cause a penalty. One incorrect return can lead to an amendment. But HMRC enquiries are often driven by mismatch: the business story told by the VAT returns does not match the annual accounts; payroll records do not match the director’s personal tax position; the company’s Companies House accounts do not support what appears in the Corporation Tax return.

These mismatches are common in smaller businesses because different tasks are often handled at different times, by different people, using different information. Bookkeeping may be updated monthly, payroll weekly, VAT quarterly and year-end accounts much later. If no one is checking the full picture, errors can sit unnoticed until HMRC connects the dots.

Where the tax treatment is uncertain, or where different taxes interact, professional tax guidance can help clarify the position. The key principle is broader than outsourcing: someone needs to own the reconciliation between filings, records and commercial reality.

VAT traps that make businesses more visible

VAT is one of the easiest areas for HMRC to test because the data is frequent, structured and comparable. A business submitting VAT returns every quarter creates a regular pattern. If that pattern changes sharply, or if it does not match turnover in the accounts, HMRC may want to understand why.

Registering late for VAT

A common trap is missing the VAT registration threshold because turnover is reviewed only at year end. VAT registration is based on taxable turnover over a rolling 12-month period, not simply the accounting year. A growing business can cross the threshold months before anyone notices.

The consequence is rarely limited to completing a late form. The business may have to account for VAT from the date it should have registered, even if it did not charge VAT to customers at the time. That can turn a compliance mistake into a cash flow problem, especially for businesses selling to consumers or non-VAT-registered clients.

Businesses approaching the VAT registration threshold should review the position early. The real control is a monthly rolling turnover check, not a last-minute review after accounts are prepared.

Claiming input VAT without proper evidence

Another regular issue is reclaiming VAT from bank payments, card statements or supplier emails without valid VAT invoices. HMRC can disallow input tax if the supporting documentation is insufficient. This is particularly common where businesses rely heavily on subcontractors, online purchases, fuel costs or mixed-use expenses.

The invoice matters. It should show the supplier details, VAT number, date, description, amount and VAT charged. If the business cannot produce it during a compliance check, the reclaim may become difficult to defend.

Using the wrong VAT treatment

Errors also arise from applying the wrong VAT rate or misunderstanding exempt, zero-rated and outside-the-scope supplies. The distinction can be technical, and it matters. A business may believe it has a reasonable commercial explanation, but HMRC will usually focus on the VAT legislation and evidence.

Problems are especially common in construction, property, food, education, health-related services, cross-border services and businesses selling through digital platforms. If the VAT treatment is uncertain, it should be documented at the time rather than reconstructed after HMRC asks.

Payroll and PAYE issues that can trigger questions

Payroll is another area where HMRC receives regular data. Real Time Information submissions create a live record of salaries, tax, National Insurance and employment status. If submissions are late, amended repeatedly or inconsistent with accounts, the business can become more noticeable.

Common payroll traps include:

- paying staff before payroll has been processed;

- treating workers as self-employed without reviewing employment status properly;

- missing starters, leavers or irregular payments;

- incorrectly reporting benefits and expenses;

- failing to reconcile PAYE liabilities with payments made to HMRC;

- ignoring director payroll planning until the year end.

Employment status is a particularly sensitive area. A business may call someone a contractor, but HMRC will consider the working relationship: control, substitution, mutuality of obligation, financial risk and integration into the business. Labels and invoices do not decide the position on their own.

Payroll mistakes also affect other parts of compliance. Staff costs feed into accounts, PAYE liabilities affect cash flow, director salaries interact with dividends, and benefits may need to be reflected in personal tax reporting. A payroll error is rarely just a payroll error.

Director withdrawals, dividends and personal tax confusion

Director finances are a frequent source of HMRC risk because business owners often treat company money informally. The company’s bank account is not the director’s personal account, even if the director owns the company. Withdrawals need to be categorised correctly as salary, dividends, expense reimbursement, loan account movements or repayment of money owed.

Dividends are another area where mistakes are easy to make. A dividend should generally be supported by sufficient distributable profits and appropriate company records. If money is taken without checking profits, the accounting and tax treatment can become messy. Where withdrawals are later reclassified, the story may look weak if there is no evidence from the time.

The director’s personal tax position also has to match the company records. If dividend income appears in the company accounts but is missing from the director’s Self Assessment, or if director loan account movements are not understood, HMRC may ask questions. Directors, sole traders and landlords should keep their Self Assessment obligations aligned with the business records, rather than treating personal tax as a separate afterthought.

Corporation Tax: where year-end problems usually start

Corporation Tax errors often begin months before the return is prepared. If bookkeeping is incomplete, expenses are poorly described, director loan accounts are unreconciled, or VAT has been posted incorrectly, the year-end tax computation becomes a repair exercise rather than a compliance process.

HMRC may scrutinise Corporation Tax returns where there are unusual movements in margins, high expense claims, repeated losses, related-party transactions, large director balances or discrepancies between accounts and tax returns. Some of these may be entirely legitimate. The question is whether the business can explain them clearly and support them with records.

For example, a company may report a sharp fall in profit because it invested in equipment, hired staff and expanded into a new location. That can be a normal commercial explanation. But if the records do not show the capital expenditure properly, payroll costs are inconsistent, and invoices are missing, the explanation becomes harder to evidence.

Limited companies should treat Corporation Tax reporting as part of the year-round accounting process. The strongest discipline is not the final return itself; it is maintaining records during the year in a way that allows the return to be prepared without guesswork.

Bookkeeping traps that look minor until HMRC asks

Weak bookkeeping is rarely dramatic. It looks like duplicated supplier payments, unreconciled bank transactions, personal expenses posted to general costs, missing receipts, suspense accounts that keep growing, and software balances that no one fully trusts.

These issues matter because bookkeeping is the evidence base for tax filings. VAT returns, payroll journals, annual accounts, Corporation Tax computations, CIS records and director loan accounts all depend on accurate records. If the underlying records are unreliable, every filing built on them becomes more vulnerable.

One practical example is a business that uses accounting software but leaves bank feeds unreconciled for months. The software exists, but it is not functioning as a control. Another example is a company that uploads receipts irregularly and then estimates expense categories at quarter end. That may feel efficient at the time, but it weakens the audit trail.

Software can also create a false sense of security. Bank feeds, automated rules and receipt capture tools reduce manual work, but they do not decide whether an expense is allowable, whether VAT has been coded correctly, or whether a director’s payment should sit in the loan account. Poor handovers between bookkeepers, accountants and internal staff can make this worse: everyone assumes someone else has checked the logic.

HMRC does not expect perfection in the sense that no business ever makes an administrative error. It does expect reasonable care. The ability to show a consistent process, timely corrections and retained evidence often matters when HMRC considers penalties.

CIS and construction businesses: higher-risk patterns

Construction businesses often face greater HMRC scrutiny because CIS, VAT, payroll and subcontractor status can overlap. A contractor may be dealing with CIS deductions, VAT invoices, employment status questions, reverse charge VAT and subcontractor verification at the same time.

Common CIS traps include failing to verify subcontractors, applying the wrong deduction rate, treating labour as materials, losing deduction statements, or assuming CIS automatically proves self-employment. It does not. CIS is a tax deduction regime; it does not settle employment status for every purpose.

Construction also creates timing issues. Subcontractors may be paid quickly, paperwork may arrive late, and site managers may approve costs before the finance function has checked tax treatment. HMRC risk often appears where operational speed outruns administrative control.

Companies House filings can also affect HMRC perception

Companies House and HMRC are separate bodies, but company filings still contribute to the wider compliance picture. Confirmation statements, accounts, director details and registered office records should broadly support the tax position being reported.

Problems arise where Companies House accounts are filed late, dormant accounts are submitted while the business is visibly trading, director details are outdated, or the company’s public filings do not align with tax returns. Again, this does not automatically mean tax has been underpaid, but it can create avoidable questions.

Directors sometimes underestimate this because Companies House filings are seen as administrative rather than tax-related. In practice, poor company administration can weaken trust in the overall compliance position.

Real-world examples of how businesses get flagged

Consider a small retail business that grows quickly through online sales. The owner checks annual turnover only when preparing accounts and misses the VAT threshold during the year. By the time the issue is identified, the business should have registered several months earlier. HMRC may expect VAT from the effective registration date, and the business may not be able to recover that VAT from customers after the event.

Another example is a consultancy company where the director takes regular withdrawals but does not run payroll consistently or document dividends properly. At year end, the accountant has to reconstruct the director loan account from bank transactions. If HMRC later asks how the withdrawals were treated, the explanation depends heavily on after-the-event classification rather than contemporaneous records.

A third case is a construction company that pays subcontractors under CIS but fails to keep verification evidence and mixes labour and materials inconsistently. The monthly CIS returns appear complete, but the supporting documents do not prove the deduction decisions. If HMRC opens a compliance check, the business may struggle even where there was no intention to misreport.

A fourth example is a seasonal business whose turnover spikes in summer, then falls sharply in winter. The margin change may be commercially normal, but if stock records, staffing costs and VAT returns do not support the explanation, the fluctuation can look unusual from the outside.

These examples share the same underlying weakness: the business activity moved faster than the compliance process.

Deep expert breakdown: HMRC looks at patterns, not just forms

The strongest HMRC risk signals often come from patterns across systems. A VAT return may look acceptable on its own. Payroll may look acceptable on its own. The Corporation Tax return may appear complete. The issue appears when the same business story is told differently in each place.

That is why reconciliation matters. Turnover in VAT returns should broadly connect to sales in accounts. Payroll submissions should connect to wages, pension records and payments. CIS deductions should connect to subcontractor records. Director loan movements should connect to bank transactions and board decisions. Companies House accounts should not contradict the tax position without a clear reason.

Judgement-based areas need particular care. Employment status, VAT treatment, mixed-use expenses, director remuneration, related-party transactions and capital versus revenue expenditure often depend on facts. If the business has made a judgement, it should be able to show what facts were considered and why the treatment was chosen.

Late filings and penalties: why timing still matters

Late filing is one of the simplest ways to attract penalties and HMRC attention. VAT returns, PAYE submissions, CIS returns, Corporation Tax returns, Self Assessment returns and Companies House accounts each have their own deadlines. Missing one deadline may be manageable. Repeated lateness suggests poor control.

Penalties vary depending on the tax, the behaviour, the delay, the disclosure and the circumstances. Interest may also apply where tax is paid late. If a business receives a penalty it believes is incorrect or unfair, it should act promptly rather than ignore the notice. Information on appealing HMRC penalties can be relevant, although not every penalty can be cancelled and the strength of any appeal depends on the facts.

The better approach is prevention. A simple compliance calendar, reviewed monthly, often prevents more damage than complicated year-end fixes. The calendar should include filing dates, payment dates, payroll submission dates, VAT periods, CIS monthly deadlines, Companies House deadlines and internal cut-off dates for collecting records.

Forms, submissions and the danger of incomplete information

HMRC forms are often treated as isolated administrative tasks. That is risky. A form submitted with incomplete or inconsistent information can create future problems, particularly where it affects registrations, authorisations, VAT, payroll, Self Assessment or company tax records.

The issue is not only whether a form has been submitted. It is whether the information on that form fits the wider tax position. For example, registering for VAT with the wrong effective date can affect historic returns. Updating PAYE details late can create mismatches. Self Assessment registration delays can lead to missed filing obligations.

Businesses dealing with HMRC forms and submissions should keep copies of forms, confirmations, reference numbers and correspondence. If HMRC later queries a date, registration status or declaration, the business should not be relying on memory.

What HMRC means by reasonable care

Reasonable care is not the same as never making a mistake. HMRC generally considers what steps the business took to get things right. Did it keep records? Did it review deadlines? Did it seek clarification where the position was uncertain? Did it correct errors promptly? Did the business rely on unsupported assumptions, or was there a documented process?

This matters because penalties can depend on behaviour. An error caused despite reasonable care is treated differently from an error caused by carelessness, deliberate behaviour or concealment. The practical difference can be significant.

Reasonable care for a small owner-managed business will not look identical to reasonable care for a larger company with a finance department. HMRC should consider context. But size is not a complete defence. A small business still needs records, deadlines, reconciliations and evidence for tax positions taken.

The warning signs directors should not ignore

HMRC risk often becomes visible before an enquiry arrives. Directors and finance teams should pay attention to early signs that compliance control is weakening.

- VAT returns are being prepared from estimates rather than reconciled records.

- Bank reconciliations are more than a month behind.

- Payroll is corrected repeatedly after submission.

- Director withdrawals are not categorised during the year.

- Supplier invoices are missing for major costs.

- Companies House deadlines are being handled at the last minute.

- CIS deductions are made without retained verification evidence.

- Tax payments are regularly made late because liabilities are not forecast.

- Software rules are posting transactions automatically without review.

- Different advisers or staff hold different parts of the compliance picture with no central review.

None of these signs means an HMRC enquiry is inevitable. They do mean the business is losing its ability to explain itself clearly if questions arise.

How to reduce the chance of being flagged

Avoiding HMRC problems is less about clever tax planning and more about disciplined administration. The strongest controls are often mundane: reconcile the bank, keep invoices, review VAT thresholds, file on time, document director decisions and make sure payroll, VAT and accounts agree with each other.

A practical control framework should include:

- Monthly bookkeeping review: bank accounts reconciled, suspense items cleared and unusual transactions explained.

- VAT sense-checks: taxable turnover, VAT rates, input tax evidence and registration position reviewed regularly.

- Payroll reconciliation: PAYE submissions checked against salary payments, pension records and accounts.

- Director account review: withdrawals categorised during the year, not reconstructed after year end.

- CIS evidence control: subcontractor verification, deduction statements and invoice treatment retained consistently.

- Deadline monitoring: HMRC and Companies House obligations tracked with internal preparation dates, not just statutory deadlines.

- Year-end readiness: accounts prepared from reconciled records rather than incomplete bookkeeping.

The value of these controls is not only penalty avoidance. They also give directors better management information. A business that knows its VAT exposure, payroll liabilities, tax provision and cash position early is usually better placed to make commercial decisions.

What to do if HMRC has already made contact

If HMRC sends a notice, query or compliance check letter, the worst response is silence. The second worst response is a rushed reply based on incomplete information. Businesses should read the letter carefully, identify exactly what HMRC is asking for, check deadlines and gather evidence before responding.

Responses should be accurate, specific and supported by records. If an error is found, it is usually better to address it clearly than to defend a weak position. If more time is needed, the business should consider requesting it before the deadline expires.

Directors should also avoid treating every HMRC letter as an accusation. Some checks are routine or limited in scope. A calm, organised response often helps contain the issue. The quality of the first response can influence how the enquiry develops.

The strategic lesson: compliance is part of operations

The businesses that manage HMRC risk well usually do not treat tax as a once-a-year exercise. They treat compliance as part of operations. Sales processes affect VAT. Hiring decisions affect PAYE. Subcontractor onboarding affects CIS. Director remuneration affects payroll, dividends and Self Assessment. Company administration affects the credibility of public records.

This is why HMRC traps often appear at points of change: growth, new staff, new sales channels, property transactions, overseas customers, construction projects, director loans, company restructuring or cash flow pressure. The tax risk is not separate from the business event. It is built into it.

For directors, the question is not simply “Have we filed?” A better question is “Could we explain and evidence what we filed if HMRC asked six months from now?” That question changes behaviour. It encourages cleaner records, earlier reviews and fewer assumptions.

Key takeaways for avoiding HMRC flags and penalties

- HMRC risk often comes from inconsistencies between VAT, payroll, accounts, Self Assessment, Corporation Tax, CIS and Companies House records.

- An HMRC enquiry trigger is not the same as proof of wrongdoing or an automatic penalty.

- Late VAT registration can create a direct cash cost if VAT was not charged when it should have been.

- Input VAT claims need proper VAT invoices, not just proof of payment.

- Director withdrawals should be categorised and documented during the year.

- Payroll errors can affect accounts, PAYE liabilities, benefits reporting and personal tax.

- CIS compliance requires verification evidence, deduction records and clear labour/material treatment.

- Companies House filings should support, not contradict, the wider business position.

- Reasonable care depends on process, evidence, behaviour and timely correction.

- Good bookkeeping is the foundation of defensible tax compliance.

- If HMRC makes contact, respond carefully, accurately and within the required timeframe.

Final expert perspective

Most HMRC problems do not begin with a tax return. They begin earlier, in the ordinary habits of the business: how income is recorded, how expenses are evidenced, how directors take money, how payroll is run, how VAT is reviewed and how deadlines are managed.

The strongest protection is not panic after HMRC writes. It is a record-keeping and review process that makes the business easy to explain. Clean records do not remove every tax risk, and they do not guarantee HMRC will never ask questions. They do, however, put the business in a far stronger position if questions come.

For UK companies, sole traders and directors, that is the practical standard to aim for: not perfection, but control, evidence and consistency. Those three qualities prevent many small mistakes from becoming expensive HMRC problems.