VAT and Environmental Taxes: Implications for UK Companies

Environmental taxes used to sit at the edge of financial reporting for many UK companies. They were relevant to energy-intensive manufacturers, landfill operators, packaging producers, importers and a handful of specialist sectors. That position has changed. Packaging reform, energy costs, waste rules and supply-chain pricing now touch a much wider group of businesses than the obvious high-emission industries.

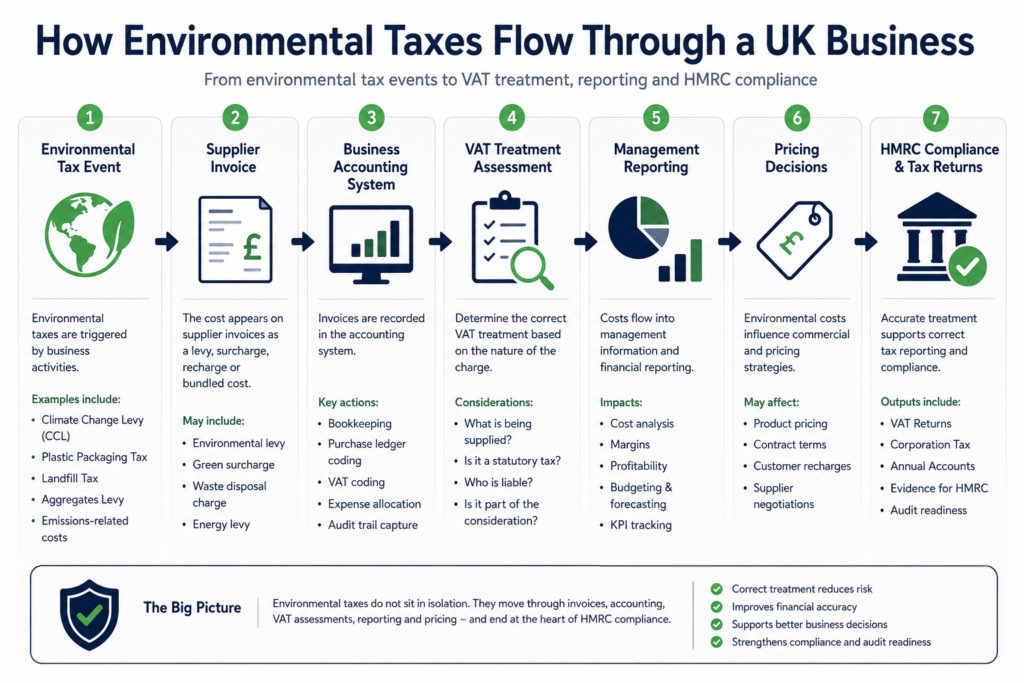

VAT adds another layer because environmental charges do not always sit neatly outside the VAT system. Some are statutory taxes with their own rules. Others are commercial charges, supplier recharges, levies or bundled costs that affect the VAT treatment of an invoice. The practical difficulty is not simply knowing that environmental taxes exist. It is understanding where they appear in the accounting records, how they flow through pricing, what HMRC expects to see, and where a company can unintentionally misstate VAT, margins or tax figures.

For UK directors and finance teams, the useful question is not only “Are we VAT compliant?” or “Do we pay an environmental tax?” It is: do our VAT, bookkeeping, management reporting and tax processes properly capture the environmental costs already moving through the business?

The growing overlap between VAT and environmental taxation

VAT is a transaction tax. Environmental taxes are separate regimes designed to influence behaviour, fund environmental objectives or price the environmental impact of certain activities. They are different in purpose, but they often meet in the same place: invoices, contracts, imports, supply chains, cost recharges and accounting systems.

UK companies may encounter environmental taxes and related charges through several routes, including:

- Climate Change Levy on taxable supplies of electricity, gas and certain solid fuels to business users;

- Plastic Packaging Tax where plastic packaging components fall within the UK rules and do not meet the required recycled plastic content;

- Landfill Tax on taxable disposals of waste at landfill sites;

- Aggregates Levy on commercially exploited aggregate;

- emissions-related costs embedded in logistics, manufacturing or energy contracts;

- waste disposal and recycling charges passed through by suppliers;

- environmental compliance costs included in product pricing or service fees.

The VAT issue depends on the nature of the charge. A statutory environmental tax may have a different treatment from the underlying taxable supply. A supplier may also pass on a cost as part of its price, in which case the VAT treatment may follow the supply rather than the label used on the invoice. That distinction is where errors often begin.

Why the distinction matters in practice

A finance team may see a line on an invoice labelled “environmental levy”, “green surcharge”, “waste tax”, “carbon charge” or “packaging charge” and assume it has a fixed VAT treatment. It rarely works like that. Labels are helpful, but they do not determine the tax position. HMRC will look at what is actually being supplied, who is liable for the charge, whether the amount is a statutory tax, and whether it forms part of the consideration for a taxable supply.

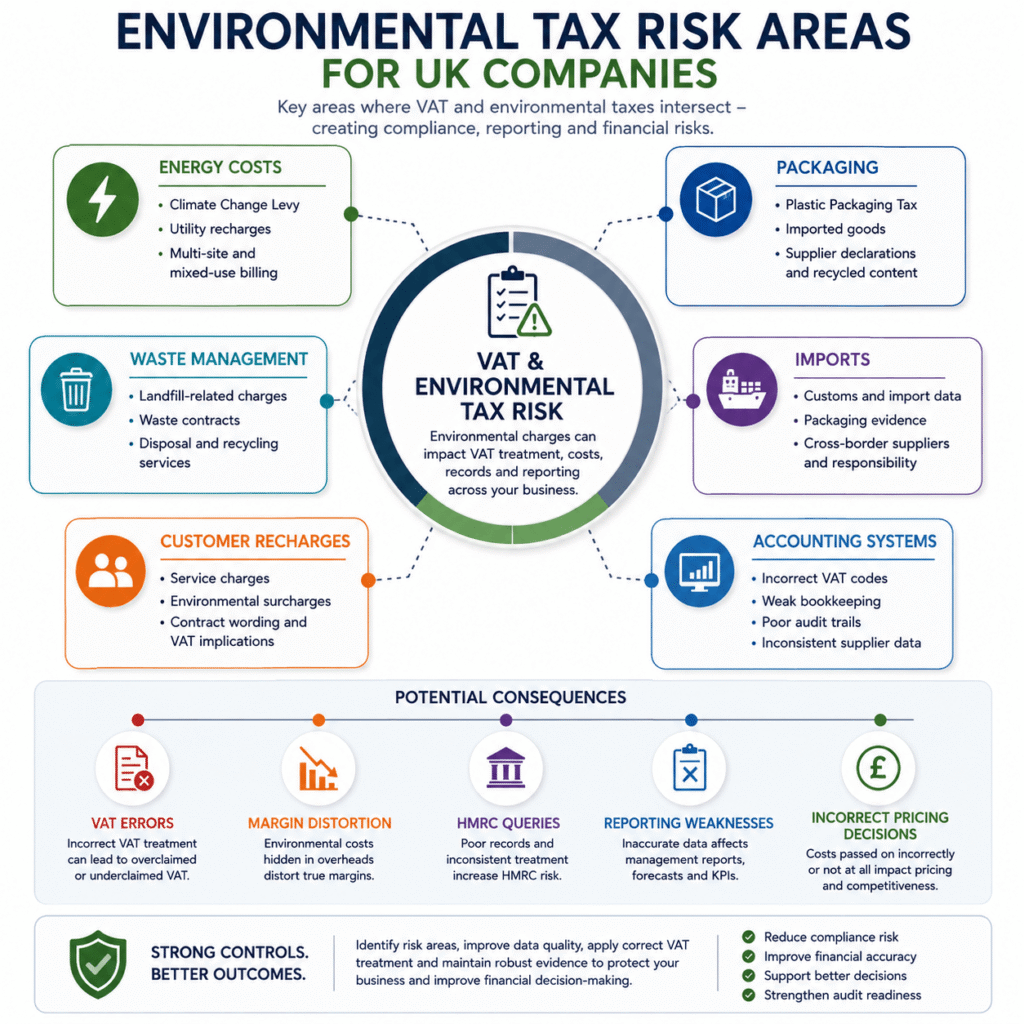

That matters because small classification errors can distort several areas of a company’s records. Input VAT may be overclaimed or underclaimed. Supplier costs may be coded inconsistently. Customer invoices may show VAT incorrectly. Gross margins may be unreliable where environmental charges are absorbed into cost of sales. The Corporation Tax position may also depend on accounting data that separates tax, duty, commercial recharge and operational cost properly.

The effect is rarely dramatic on a single transaction. The risk builds through repetition. A monthly energy invoice, a recurring waste contract, a packaging supply chain or a high-volume import process can multiply the same misunderstanding across the year.

Where UK companies usually encounter the issue

The most visible cases are energy, waste, packaging and construction materials. These areas generate frequent invoices, operational pressure and a mixture of statutory and commercial language that can confuse non-specialist staff.

Energy supplies and Climate Change Levy

Climate Change Levy, often shortened to CCL, applies to certain taxable supplies of energy products to business and public sector users. It commonly appears on commercial electricity and gas bills. VAT and CCL interact because the energy supply itself has a VAT treatment, while CCL is a separate environmental levy charged under its own rules.

Errors usually arise when businesses treat the whole energy bill as one undifferentiated cost, especially where there are multiple sites, mixed-use premises, reduced-rate considerations, landlord recharges or exemption evidence. A small office with a straightforward electricity bill may not face much complexity. A property company, manufacturer, hospitality group or business operating from shared premises may need more careful analysis.

Landlords and managing agents should be particularly cautious. Recharging energy or utilities to tenants is not always a simple reimbursement. The VAT treatment may depend on the lease, the nature of the supply, how costs are apportioned and whether the recharge is part of a wider property supply. Environmental levies embedded in the original utility bill can become difficult to interpret once they are recharged through service charge accounts.

Waste disposal, recycling and Landfill Tax

Landfill Tax applies to taxable disposals of material at landfill sites. Most trading companies are not landfill operators, but they may still bear the cost indirectly through waste management invoices. A waste contractor may include disposal costs, transport, handling, recycling services and landfill-related charges in one invoice.

The VAT treatment depends on the supply made by the contractor, not simply on the fact that environmental tax is somewhere in the cost base. A waste management service is generally a taxable supply for VAT purposes, even if the contractor’s own cost structure includes environmental taxes. If an invoice splits statutory tax from service charges, the accounting treatment needs to follow the legal and commercial reality rather than a rough assumption.

Operationally, this is where bookkeeping processes become significant. If waste invoices are posted to a single nominal code without reviewing VAT treatment, a business may not notice inconsistent supplier approaches, missing VAT invoices, incorrect VAT rates or unusual recharges. The issue is not only compliance. Poor coding weakens cost analysis, especially for companies trying to measure sustainability-related expenditure.

Plastic Packaging Tax and supply-chain visibility

Plastic Packaging Tax has made environmental taxation more relevant to importers, manufacturers, distributors, retailers and e-commerce businesses. The tax applies to certain plastic packaging components manufactured in or imported into the UK where the recycled plastic content is below the statutory threshold, subject to detailed rules and exemptions.

For VAT purposes, the complication often sits in pricing and documentation. If a supplier increases product prices because it bears Plastic Packaging Tax, that increase may form part of the consideration for the supply. If a charge is separately itemised, the business still needs to understand whether it is a statutory tax passed through in a specific way or a commercial pricing adjustment. The invoice wording alone is not enough.

Importers face an additional challenge because responsibility may sit with the business bringing goods into the UK, even where packaging decisions were made overseas. Procurement, logistics and finance teams may each hold part of the information. One team may know the supplier, another may handle customs documentation, and another may process the purchase invoices. Unless the process is joined up, the company can miss registration obligations, misread supplier charges or fail to maintain adequate evidence of recycled content.

Aggregates Levy and construction supply chains

Aggregates Levy applies to the commercial exploitation of aggregate in the UK. Construction companies may not always be directly liable for the levy, but they can encounter it through material pricing, supplier invoices, subcontractor costs and project budgets.

Aggregates, skip hire, waste disposal and site clearance can all sit close together in construction accounting. If supplier invoices bundle labour, plant, materials, environmental charges and waste costs without clear breakdowns, finance teams may struggle to apply VAT and CIS compliance processes accurately. The same invoice can affect VAT coding, CIS treatment, project profitability and management reporting.

The misconception that environmental taxes are “just overheads”

A recurring weakness in SME finance systems is treating environmental taxes as ordinary overhead noise. That may be workable for a very small number of immaterial transactions, but it becomes unreliable as soon as environmental charges affect pricing, VAT recovery, import procedures, customer contracts or management accounts.

There are three common misconceptions.

- Assuming all environmental charges are outside the scope of VAT. Some statutory taxes may be outside the scope in their own right, but commercial recharges and embedded costs can still be part of a VATable supply.

- Assuming the supplier’s invoice is always correct. Suppliers can make mistakes, especially where they use generic invoice descriptions or automated billing systems.

- Assuming the issue belongs only to the tax function. In reality, the information often starts in procurement, operations, logistics, facilities management or commercial teams before it reaches the accounts team.

The last point is easy to underestimate. Environmental cost data rarely arrives in a neat tax file. It arrives through energy bills, waste contracts, packaging specifications, construction site costs, supplier terms and import paperwork. If those documents are not captured properly at bookkeeping stage, the VAT return may be technically produced on time while still relying on weak underlying information.

VAT treatment depends on what the payment is really for

The central VAT question is deceptively simple: what is the consideration for the supply? If an environmental amount is part of the price paid for goods or services, it may follow the VAT liability of that supply. If it is a tax imposed by statute and collected in a particular capacity, the analysis may differ. If it is a disbursement, reimbursement, compensation, penalty or contractual recharge, each category has its own VAT considerations.

HMRC does not generally accept that businesses can choose the VAT treatment by naming a line item creatively. A “green fee” added by a supplier may simply be extra consideration for the supply. A “waste levy” may be part of a taxable waste management service. A “carbon surcharge” in a logistics contract may be a commercial price adjustment. Conversely, some statutory charges should not be treated as VATable merely because they appear on the same invoice as taxable supplies.

This is why VAT reviews often focus less on the headline tax and more on the contract, invoice flow and accounting entries. The legal structure of the transaction matters. So does how the amount is communicated to the customer, whether the supplier acts as principal or agent, and whether the business has evidence to support the VAT position taken. Where the issue sits within UK tax services more broadly, the VAT answer still needs to be grounded in the transaction facts.

Examples that show the practical difference

Consider a wholesaler receiving goods from a UK supplier. The invoice includes a separate “packaging environmental charge”. The accounts assistant posts the full net amount as purchases and claims VAT on the VAT shown. If the supplier has treated the charge as part of the taxable supply and VAT is correctly charged, the posting may be fine. But if the supplier has itemised a statutory tax incorrectly, or the company later recharges the amount to customers without understanding its nature, the error may move downstream.

Now take a property company that pays a commercial electricity bill and recharges tenants through a service charge. The original bill includes CCL and VAT. The tenant recharge is prepared from a spreadsheet maintained outside the accounting system. If the recharge is treated as a pure reimbursement without considering the VAT position under the lease, the landlord may undercharge or overcharge VAT. The environmental levy is not the only issue; it exposes a wider weakness in the service charge process.

A third example is an importer of packaged consumer goods. The commercial team negotiates overseas supply terms, the logistics team handles import documentation, and finance posts purchase invoices. Plastic Packaging Tax responsibility may not be visible from the purchase invoice alone. If nobody is collecting packaging weight and recycled-content evidence, the business may discover the issue only after volumes have increased. By then, reconstructing records can be slow, especially where suppliers are outside the UK and specifications have changed over time.

For a manufacturer, the issue may be energy usage and product costing. Climate Change Levy, higher utility costs and supplier surcharges may be spread across several production lines. If the costs are not allocated properly, one product may appear more profitable than it really is while another carries costs it did not create.

How environmental taxes flow through pricing and management reporting

Environmental taxes can change the economics of a product or service without being obvious in the headline accounts. A packaging importer may see supplier prices rise. A manufacturer may face higher energy costs. A construction business may absorb waste disposal charges. A logistics-heavy business may see fuel and emissions-related surcharges become routine.

If these costs are not separated and monitored, they may be mistaken for general inflation. That can lead to poor pricing decisions. A company might increase prices across the board when the cost pressure actually sits in one product category. Or it may fail to increase prices where environmental charges are directly linked to a particular customer contract.

The VAT angle matters because customer pricing is usually considered net of VAT for business-to-business transactions but VAT-inclusive for many consumer-facing sales. Environmental charges embedded in the price can affect the VAT-inclusive amount paid by the customer, the net revenue retained by the business and the perceived affordability of the product.

This is where management accounts become more than a reporting formality. Regular cost analysis can show whether environmental charges are increasing, whether VAT recovery appears consistent, and whether customer pricing is keeping pace with supplier cost changes.

The record-keeping burden is often underestimated

Environmental taxes tend to require evidence. VAT also requires evidence. Where the two overlap, a company needs records that explain both the amount and the treatment.

For VAT, the business needs valid VAT invoices, correct VAT coding, evidence for input tax recovery and clear audit trails from source documents to the VAT return. For environmental taxes, the evidence may include energy usage, waste transfer records, packaging component data, recycled plastic content, import volumes, exemption certificates, supplier declarations or contract terms. The exact records depend on the tax and sector, but the principle is consistent: the accounting entry should be supported by something more robust than a vague invoice description.

This can place pressure on bookkeeping systems. A chart of accounts that was adequate when environmental charges were immaterial may no longer provide enough detail. If all waste, energy, packaging and logistics surcharges are posted into broad overhead codes, management may struggle to answer basic questions:

- Which sites or product lines carry the highest environmental cost?

- Are supplier surcharges statutory, contractual or discretionary?

- Has VAT been recovered consistently?

- Are costs being passed on to customers correctly?

- Do records support the treatment used in VAT and tax filings?

Good bookkeeping is not just tidy administration here. It is the foundation for defensible VAT returns, reliable management accounts and informed pricing decisions.

Corporation Tax, annual accounts and reporting quality

Environmental taxes and related costs generally feed into the profit and loss account, but their presentation and deductibility depend on the nature of the expense and the wider tax rules. A properly incurred business cost may be deductible for Corporation Tax, while penalties or non-business items may require different treatment. The key point is that Corporation Tax work depends heavily on the quality of the accounts beneath it.

If VAT has been incorrectly treated, or if environmental charges have been posted inconsistently, the year-end accounts may need adjustment. That can affect taxable profits, management information and director understanding of business performance. Annual accounts may satisfy statutory filing requirements, but they provide limited operational insight if environmental costs are buried in broad expense categories.

Companies House filings will not usually disclose the detail of VAT or environmental tax treatment. Even so, statutory accounts depend on the integrity of accounting records. HMRC filings, VAT returns and Corporation Tax returns depend on the same underlying systems. Where environmental tax exposure is material, directors should view cost visibility as part of financial governance rather than a niche compliance exercise.

Warning signs that the current process may be weak

Certain patterns suggest the company’s VAT and environmental tax treatment may need closer review:

- environmental charges are posted to miscellaneous overhead codes without review;

- different suppliers apply VAT differently to similar-looking charges;

- customer recharges are prepared manually outside the accounting system;

- energy, waste or packaging costs have risen but management reports do not explain why;

- imported goods include packaging, but nobody retains packaging weight or recycled-content evidence;

- construction invoices combine labour, materials, waste and surcharges with limited breakdown;

- staff assume that anything described as a “tax” or “levy” has no VAT consequences;

- VAT return preparation relies heavily on default software codes with little invoice review.

None of these points proves that the VAT treatment is wrong. They indicate that the process may not be strong enough to support the treatment confidently.

Software helps, but it does not decide the tax position

Cloud accounting systems and digital VAT tools have improved record keeping, but they can also create false comfort. A default VAT code applied to a supplier account may repeat the same error indefinitely. Optical character recognition may capture invoice totals while missing the significance of a separate environmental line. Automated bank feeds may speed up posting but do not interpret contract terms.

Making Tax Digital has encouraged more structured VAT processes, yet the quality of the VAT return still depends on the quality of the underlying coding and review. Automation is useful where rules are clear and data is reliable. It is less reliable where the issue depends on whether a charge is statutory, contractual, a disbursement, a recharge or part of the consideration for a wider supply.

For that reason, companies should treat automation as a control tool rather than a substitute for tax judgement. The most effective systems combine good software configuration with periodic human review of high-risk cost categories.

How to build a workable internal approach

A sensible review does not need to begin with a full technical investigation of every environmental tax. It can start with the transactions already passing through the business.

Finance teams should look at recurring supplier invoices for energy, waste, packaging, logistics, imports and site services. They should identify line items labelled as levies, surcharges, environmental fees, compliance charges or taxes. The next step is to check how those lines are coded for VAT and whether the treatment is consistent across suppliers and periods.

For companies with imports or manufactured products, procurement records may be as important as finance records. Packaging specifications, supplier declarations and shipment data can determine whether environmental tax obligations exist. If that information sits outside the accounts function, the company needs a process for bringing it into tax and reporting decisions.

Customer contracts also deserve attention. If environmental charges are passed on, the contract should make clear what the customer is paying for and how price adjustments work. Ambiguous wording can create VAT uncertainty and commercial disputes. This is particularly relevant in long-term contracts where costs may change during the term.

A workable internal process might include:

- separate nominal codes for significant environmental cost categories, rather than burying them in general overheads;

- VAT code checks for recurring suppliers that apply levies, surcharges or environmental charges;

- review of contracts where environmental costs are passed on to customers;

- retention of supplier evidence for packaging, imports, energy usage or waste disposal where relevant;

- periodic review of management accounts to identify unusual cost movements;

- coordination between finance, procurement and operations before new environmental initiatives or supplier arrangements are launched;

- documented reasoning for VAT treatment where the position is not obvious.

The aim is not perfection for its own sake. It is to create a record that a competent person can follow later. If HMRC asks about a VAT return, or if directors ask why margins changed, the business should be able to explain the treatment without reconstructing the position from scattered emails.

Sector differences are significant

The implications vary widely by sector. A professional services company may mainly see the issue through energy bills and office waste contracts. A retailer may have packaging, imports, logistics surcharges and consumer pricing considerations. A manufacturer may face energy, raw materials, waste, packaging and capital investment questions. A construction company may deal with aggregates, waste disposal, CIS and VAT reverse charge interactions.

This sector variation is one reason generic checklists are limited. They can help identify possible exposure, but they cannot replace a review of the company’s actual transactions. Two businesses with similar turnover may have very different environmental tax profiles depending on their supply chain, premises, products and customer contracts.

Strategic implications beyond compliance

Environmental taxes are designed to change behaviour. That means they should not be viewed only as costs to be posted after the event. They can influence supplier selection, product design, packaging choices, energy contracts, waste strategy, customer pricing and investment decisions.

For example, Plastic Packaging Tax may encourage changes in packaging materials or supplier specifications. Energy-related costs may support investment in efficiency measures. Waste taxes and disposal charges may make recycling, segregation or process redesign commercially worthwhile. These decisions are operational, but their financial evaluation depends on accurate tax and accounting information.

Companies that capture environmental costs clearly can make better decisions. They can distinguish unavoidable statutory costs from supplier pricing choices. They can assess whether operational changes reduce tax exposure or simply move cost elsewhere. They can also explain margin changes more convincingly to directors, investors, lenders or internal stakeholders.

Key points for UK companies

VAT and environmental taxes should not be treated as separate worlds. They intersect through invoices, contracts, imports, recharges and accounting records. The VAT treatment depends on the nature of the supply and the character of the charge, not just the wording used on an invoice.

Companies should pay particular attention where environmental charges are recurring, material, passed on to customers or linked to imports and packaging. They should also review any area where operational teams hold information that finance needs for tax compliance. Weak communication between procurement, operations and accounts is one of the most common causes of avoidable errors.

Good records are central. Valid VAT invoices, clear coding, supplier evidence, contract terms and management reporting all contribute to a defensible position. Where the facts are unclear, it is better to resolve the treatment early than to correct repeated errors at year end or during an HMRC review.

A practical final perspective

VAT and environmental taxes are becoming a more visible part of UK company finance, not because every business has suddenly become an environmental tax specialist, but because environmental costs now travel through ordinary commercial systems. They appear in supplier invoices, customer pricing, imports, utility bills, waste contracts, construction costs and management accounts.

The companies most likely to handle this well are not necessarily the largest. They are the ones that notice where tax, operations and accounting meet. They question ambiguous invoice descriptions. They keep evidence before it is needed. They configure bookkeeping systems to reflect real cost behaviour. They involve finance early enough in operational decisions to prevent tax treatment becoming an afterthought.

For UK directors and finance teams, the practical priority is clear: understand the environmental charges already present in the business, decide how they should be treated for VAT and accounting purposes, and maintain records that support that decision. That approach will not remove complexity, but it makes the complexity manageable.