How UK SMEs Can Use Flat-Rate VAT Schemes Effectively

The Flat Rate VAT Scheme is often presented as a simpler way for smaller businesses to handle VAT. That is true, but only up to a point.

For some UK SMEs, the scheme can make VAT reporting easier, reduce administrative friction and provide a more predictable relationship between turnover and VAT payments. For others, it can quietly become more expensive than standard VAT accounting, particularly once the business starts buying more goods, investing in equipment or falling within HMRC’s Limited Cost Trader rules.

The problem is that the scheme looks simple from the outside. A business charges VAT to customers, applies a fixed percentage to VAT-inclusive turnover, and pays that amount to HMRC. The difficult part is not the calculation itself. The difficult part is knowing whether the calculation still makes commercial sense for the business as it operates now.

A consultancy with low VATable costs may see a useful benefit. An e-commerce business with stock purchases may lose valuable input VAT recovery. A contractor who used the scheme successfully several years ago may now be caught by the 16.5% Limited Cost Trader rate. A growing company may discover that the scheme made sense when turnover was modest but no longer fits after recruitment, software investment, subcontractor costs or new premises.

That is why the better question is not simply, “Is the Flat Rate VAT Scheme worth it?”

The better question is: does the scheme produce the right VAT outcome for this specific business model, cost base and stage of growth?

Why the Flat Rate VAT Scheme is still misunderstood

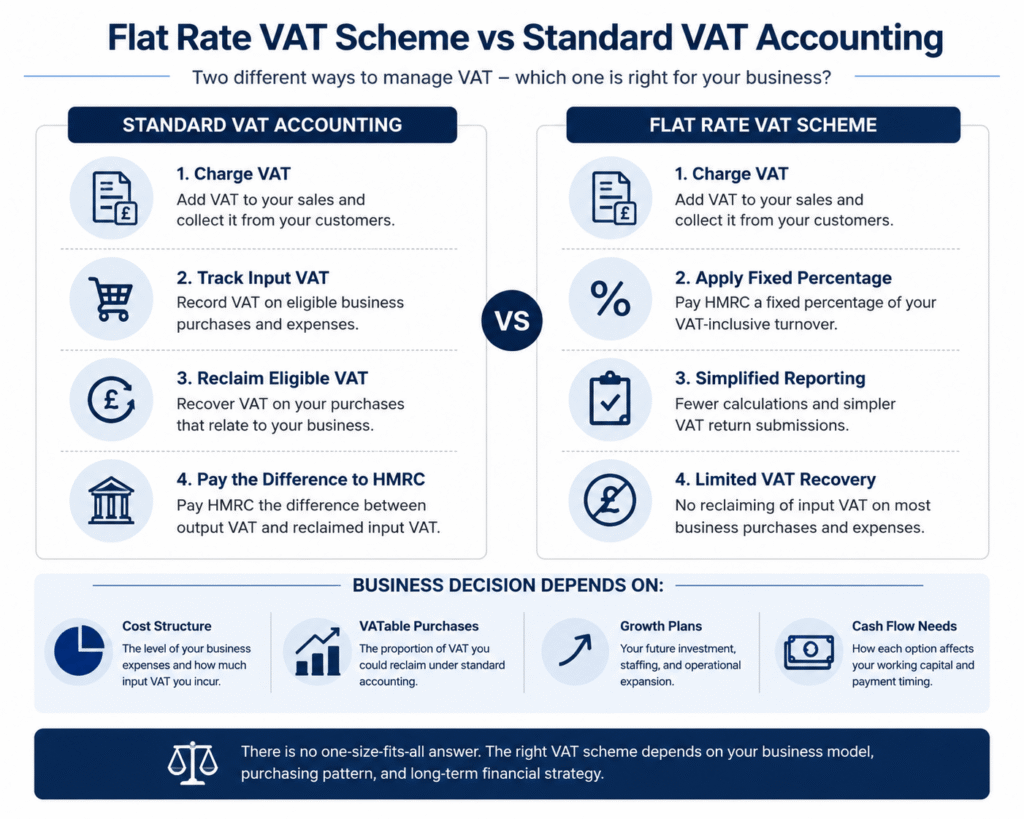

The Flat Rate VAT Scheme was designed by HMRC to simplify VAT accounting for smaller VAT-registered businesses. Instead of calculating output VAT on sales and deducting input VAT on most purchases, an eligible business applies a fixed flat-rate percentage to its VAT-inclusive turnover.

HMRC currently states that a business may be able to join the scheme if its VAT taxable turnover is £150,000 or less, excluding VAT. The scheme is not open-ended: businesses generally need to leave if their turnover exceeds the relevant exit threshold, commonly £230,000 including VAT, subject to HMRC rules and the timing of the review.

The administrative appeal is clear. The business still charges VAT at the normal rate where required, but the amount it pays to HMRC is calculated using a sector-based percentage. HMRC’s own guidance also makes clear that businesses usually cannot reclaim VAT on purchases while using the scheme, except for certain capital assets over £2,000.

That last point is where many poor decisions begin.

Some directors focus on the difference between the 20% VAT charged to customers and the lower flat-rate percentage paid to HMRC. That can create the impression that the scheme automatically produces a saving. In reality, the benefit depends on what the business gives up in input VAT recovery.

The scheme is therefore not just a VAT filing choice. It is a commercial judgement about revenue, expenditure, margins, record-keeping, growth plans and the type of costs the business actually incurs.

How the calculation works in practice

Under standard VAT accounting, a business usually charges VAT on taxable sales, records VAT paid on eligible purchases, and pays the difference to HMRC through its VAT return.

Under the Flat Rate VAT Scheme, the business applies its flat-rate percentage to gross turnover. Gross turnover means the VAT-inclusive amount, not the net invoice value.

For example, if a business invoices a customer £10,000 plus VAT, the customer pays £12,000 in total. If the business uses a 12% flat rate, the calculation is applied to £12,000:

£12,000 × 12% = £1,440 payable to HMRC

The business has charged £2,000 of VAT to the customer, but under the Flat Rate Scheme it pays £1,440 to HMRC. The difference may look like a benefit, but the business must also consider the VAT it can no longer reclaim on most purchases.

If the same business has very low VATable costs, the scheme may still be attractive. If it has purchased equipment, stock, materials or other VATable inputs, standard VAT accounting may produce a better result.

The first-year discount can help, but it should not drive the whole decision

Newly VAT-registered businesses may receive a 1% discount on their flat-rate percentage during the first year of VAT registration. This can make the scheme look particularly attractive at the point when a business first crosses the VAT registration threshold.

The discount is useful, but temporary. A decision based entirely on the first-year rate can become misleading once the reduction ends.

A better approach is to model both positions: the first-year outcome and the normal ongoing outcome. If the scheme only works because of the temporary discount, the business should know that before relying on it as a long-term VAT strategy.

Where the scheme can work well

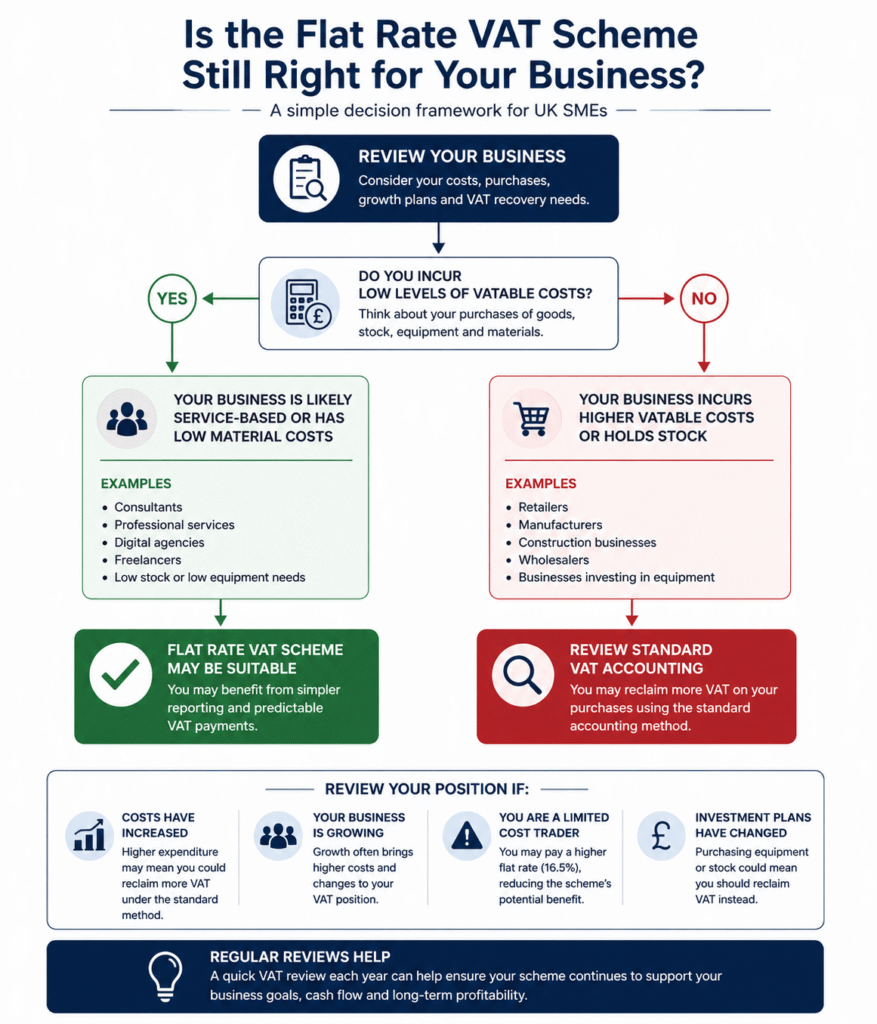

The Flat Rate VAT Scheme tends to work best where the business has limited VATable purchases and generates most of its value through labour, expertise, advice or intellectual work.

That is why it is often considered by consultants, advisers, marketing professionals, design studios, IT specialists, trainers and certain contractors. These businesses may have relatively few goods-related purchases compared with turnover.

The key phrase is “may have”. Sector alone is never enough.

A small digital consultant working from home with limited expenses may have a very different VAT outcome from a growing agency buying software, outsourcing delivery work, investing in paid media tools and using freelancers or subcontractors. Both may describe themselves as digital businesses, but their cost structures are not the same.

In practice, the scheme is most likely to be worth reviewing where:

- the business has low VATable purchases;

- most value comes from professional time or expertise;

- stock, materials and equipment costs are modest;

- cash-flow forecasting benefits from a simpler VAT calculation;

- the business is not affected by the Limited Cost Trader rate;

- standard VAT input recovery would not be substantial.

Even then, the numbers should be reviewed rather than assumed.

Where the scheme often becomes expensive

The scheme often becomes less attractive for businesses that regularly buy goods, stock, materials or capital items. These businesses may lose more in input VAT recovery than they gain from the flat-rate calculation.

That can affect retailers, e-commerce businesses, wholesalers, manufacturers, hospitality operators, trades, construction businesses and companies investing heavily in equipment or infrastructure.

An online retailer, for example, may purchase inventory, packaging, fulfilment materials, storage services and operational equipment. Under standard VAT accounting, input VAT on many of those purchases may reduce the VAT payable to HMRC. Under the Flat Rate VAT Scheme, that recovery is usually not available in the same way.

The same issue can arise during growth phases. A business may have benefited from the scheme when costs were low, then gradually become less suited to it as it hires staff, leases premises, invests in systems or increases supplier spend.

This is one of the most common practical problems with the scheme: the original decision may have been sensible, but nobody revisits it after the business changes.

The Limited Cost Trader rules are often the turning point

The Limited Cost Trader rules are one of the main reasons the Flat Rate VAT Scheme became less attractive for many service-based businesses.

HMRC treats a business as a limited cost business if its spending on relevant goods is less than either 2% of its turnover, or £1,000 a year where costs are more than 2%. Businesses caught by these rules generally use the higher 16.5% flat rate.

This matters because many service businesses spend money on things that do not necessarily count as relevant goods for the test. Software subscriptions, professional fees, subcontractor costs, rent, travel and many services may be real business costs, but they do not always help the business avoid Limited Cost Trader status.

That distinction surprises many directors. A business can feel expensive to run and still be treated as low-cost for Flat Rate VAT purposes if most of its costs are services rather than qualifying goods.

The result can be commercially significant. At 16.5% of VAT-inclusive turnover, the Flat Rate Scheme may offer little advantage once lost input VAT recovery is considered.

For example, on VAT-inclusive turnover of £120,000, the 16.5% rate produces a VAT payment of:

£120,000 × 16.5% = £19,800

That needs to be compared against the business’s likely position under standard VAT accounting, including input VAT recovery. Without that comparison, the business may be using the scheme out of habit rather than benefit.

What Practitioners Often See After Two or Three Years on the Scheme

One pattern appears repeatedly among growing SMEs. The business joins the Flat Rate VAT Scheme, experiences a straightforward first year, becomes comfortable with the reporting process and then stops reviewing whether the arrangement still makes commercial sense.

Nothing appears wrong. VAT returns are submitted on time. HMRC compliance obligations continue to be met. Bookkeeping remains manageable.

The problem is that the business itself may no longer resemble the business that originally joined the scheme.

A company that started with one director may now employ staff. A consultancy may have added subcontractors. A digital agency may have invested heavily in software platforms and specialist tools. An online retailer may have expanded product ranges and inventory levels.

None of those developments automatically mean the Flat Rate Scheme is wrong. They simply mean the original assumptions deserve another look.

In practice, some of the most successful SMEs review VAT arrangements at the same time they review pricing, margins, staffing costs and growth plans. VAT becomes part of financial management rather than a separate compliance exercise.

The Cash Flow Question Is Often More Important Than the VAT Question

Business owners frequently focus on how much VAT they pay to HMRC. That matters, but it is not always the most important consideration.

Business owners frequently focus on how much VAT they pay to HMRC. That matters, but it is not always the most important consideration.

Cash flow often has a greater influence on day-to-day decision-making.

A predictable VAT liability can make budgeting easier. Directors may find it simpler to forecast quarterly obligations when VAT payments are linked directly to turnover through a flat-rate percentage.

However, predictability has a cost if substantial input VAT recovery is being sacrificed.

Imagine two businesses with identical turnover. One operates with minimal overheads. The other regularly invests in equipment, software, stock and infrastructure.

The second business may experience tighter cash flow despite similar revenue because unrecovered VAT remains embedded within operating costs.

That distinction rarely appears in simple online explanations of the scheme, yet it often becomes obvious when reviewing management accounts over a longer period.

The VAT calculation itself may look efficient. The broader financial picture may tell a different story.

Making Tax Digital Has Changed Part of the Original Argument

When the Flat Rate VAT Scheme was first introduced, administrative simplicity was one of its strongest selling points.

The compliance environment has changed significantly since then.

Making Tax Digital for VAT requires many VAT-registered businesses to maintain digital records and submit VAT returns through compatible software. Cloud accounting systems now automate large parts of the VAT process that previously required considerably more manual effort.

As a result, some businesses that originally joined the scheme primarily to reduce administrative work may find that modern software has narrowed the difference between the two approaches.

This does not remove the value of the Flat Rate Scheme. It simply means the commercial calculation often becomes more important than the administrative calculation.

Businesses increasingly ask:

“Does the scheme improve our VAT position?”

rather than:

“Does the scheme save us bookkeeping time?”

Those are related questions, but they can lead to different conclusions.

Common Misunderstandings That Create Poor VAT Decisions

The Scheme Always Saves Money

This remains the most common misconception.

The scheme can save money in some circumstances. In others, it can increase the effective VAT cost of operating the business.

The outcome depends on turnover, expenditure patterns, flat-rate percentages, eligibility rules and the availability of input VAT recovery under standard accounting methods.

There is no universal answer.

Only Revenue Matters

Turnover is important, but expenditure often determines whether the scheme remains beneficial.

Two businesses with identical sales figures can produce dramatically different VAT outcomes if one purchases significant goods or equipment while the other operates with minimal VATable costs.

Joining the Scheme Is a Long-Term Decision

VAT elections should not be treated as permanent.

Business conditions evolve. Markets change. Costs rise. Technology investments increase. Staffing models develop.

The right decision today may not be the right decision three years from now.

Limited Cost Trader Status Only Affects Certain Industries

This misunderstanding catches many businesses by surprise.

Limited Cost Trader status is determined by qualifying expenditure rather than how the business describes itself.

A consultancy, agency, contractor or professional services business can be affected if spending on relevant goods remains below HMRC thresholds.

The Record-Keeping Requirements Do Not Disappear

Although the Flat Rate VAT Scheme simplifies certain calculations, it does not remove record-keeping responsibilities.

Businesses still need accurate financial records, appropriate bookkeeping systems and supporting documentation.

Directors remain responsible for ensuring VAT returns are accurate and supported by reliable information.

In practice, businesses using the scheme should still maintain:

- sales records;

- VAT invoices where required;

- digital accounting records;

- bank transaction evidence;

- purchase documentation;

- records supporting VAT return submissions;

- evidence supporting eligibility for the scheme.

Weak bookkeeping can create problems regardless of the VAT method being used.

Experienced advisers often find that VAT issues are not caused by complex legislation but by incomplete records, inconsistent processes and assumptions that were never properly reviewed.

When a Business Should Consider Reviewing Its Position

There is rarely a single moment when a business should leave the Flat Rate VAT Scheme. The need for review usually develops gradually.

Certain events, however, frequently justify a closer look.

- Significant increases in turnover.

- Large equipment purchases.

- Growth in stock holdings.

- Recruitment of employees.

- Expansion into new services.

- Changes in supplier relationships.

- Investment in software platforms.

- Commercial property commitments.

- Changes in profit margins.

- Entry into new markets.

None of these automatically mean the scheme has become unsuitable.

They simply indicate that the assumptions behind the original decision may have changed enough to justify a fresh comparison.

A Simple Comparison Often Reveals More Than Complex Analysis

Businesses sometimes assume that reviewing a VAT structure requires detailed tax modelling. While sophisticated analysis can be useful, many reviews begin with a straightforward comparison.

Businesses sometimes assume that reviewing a VAT structure requires detailed tax modelling. While sophisticated analysis can be useful, many reviews begin with a straightforward comparison.

A business can estimate:

- VAT paid under the Flat Rate Scheme;

- likely VAT payable under standard accounting;

- input VAT that would be recoverable;

- future investment plans;

- changes expected over the next twelve months.

Even a high-level comparison often highlights whether the difference is material.

If the gap appears significant, a more detailed review may be worthwhile. If the difference is negligible, administrative simplicity may remain a valid reason for continuing with the scheme.

The key is making a conscious decision rather than relying on assumptions formed years earlier.

A Director’s Decision Framework: Is the Flat Rate VAT Scheme Still Right?

There is rarely a single factor that determines whether a business should remain within the Flat Rate VAT Scheme. The strongest decisions are usually based on a combination of commercial, operational and compliance considerations.

Before deciding to join, remain within or leave the scheme, directors should consider several practical questions.

- How much input VAT is currently being incurred each quarter?

- Has the business become subject to Limited Cost Trader rules?

- Are significant purchases planned during the next twelve months?

- Has turnover increased substantially since joining?

- Have operating costs changed?

- Does the business rely heavily on stock, equipment or materials?

- Would standard VAT accounting improve cash flow?

- Does the administrative simplicity still create meaningful value?

The purpose of these questions is not to reach an immediate answer. Their purpose is to identify whether the assumptions behind the current VAT structure remain valid.

Businesses often spend considerable time reviewing suppliers, pricing strategies and operating costs. VAT arrangements deserve the same periodic attention.

What Businesses Often Miss When Comparing VAT Schemes

A surprisingly common mistake is focusing exclusively on the VAT calculation itself.

In reality, VAT influences wider business decisions.

The chosen VAT method can affect:

- cash-flow forecasting;

- working capital requirements;

- pricing strategies;

- management reporting;

- budget planning;

- investment decisions;

- business profitability analysis;

- growth planning.

A VAT scheme that appears advantageous on a quarterly VAT return may look less attractive when viewed through the lens of long-term business performance.

This is particularly true for SMEs entering periods of expansion, acquisition, technology investment or operational restructuring.

VAT should support commercial objectives rather than exist separately from them.

How the Flat Rate VAT Scheme Fits Into Broader Compliance Obligations

The Flat Rate VAT Scheme changes how VAT is calculated, but it does not remove the wider responsibilities associated with running a VAT-registered business.

Businesses must still maintain accurate records, submit VAT returns on time and comply with applicable HMRC requirements.

For limited companies, directors retain responsibility for ensuring financial records remain accurate and that reporting obligations are met appropriately.

The scheme also sits alongside other compliance responsibilities that many SMEs manage simultaneously, including:

- Corporation Tax obligations;

- PAYE reporting;

- payroll administration;

- bookkeeping requirements;

- Making Tax Digital compliance;

- annual accounts preparation;

- Companies House filing obligations.

This broader context is one reason why VAT decisions should not be made in isolation. Changes to bookkeeping processes, management accounts, reporting systems and operational workflows can all influence the effectiveness of a particular VAT approach.

Why Management Accounts Often Tell the Real Story

VAT returns show what has been reported to HMRC.

VAT returns show what has been reported to HMRC.

Management accounts often reveal whether the underlying decision is working.

Businesses that regularly review management accounts can usually identify trends that are not immediately visible through VAT reporting alone.

For example:

- falling margins despite growing revenue;

- increasing expenditure patterns;

- higher software and technology costs;

- greater use of subcontractors;

- rising operational overheads;

- changing purchasing behaviour.

These developments may not create VAT compliance problems, but they can alter the commercial attractiveness of the Flat Rate Scheme.

This is why experienced advisers frequently review VAT arrangements as part of wider financial performance discussions rather than treating VAT as an isolated tax topic.

The Businesses Most Likely to Benefit from Regular VAT Reviews

Not every SME needs constant VAT analysis. However, certain businesses are more likely to benefit from periodic reviews.

These often include:

- rapidly growing businesses;

- companies approaching turnover thresholds;

- businesses making significant capital investments;

- e-commerce operations;

- contractor-led businesses;

- professional service firms affected by Limited Cost Trader rules;

- companies changing operating models;

- organisations introducing new revenue streams.

Growth tends to create complexity. Complexity tends to create new VAT considerations.

The review process does not need to be complicated, but it should be deliberate.

Key Takeaways

- The Flat Rate VAT Scheme was designed to simplify VAT administration for eligible smaller businesses.

- The scheme does not automatically save money and should not be viewed as a universal tax-saving tool.

- The value of the scheme depends heavily on expenditure patterns, business model and VAT recovery opportunities.

- Limited Cost Trader rules have significantly changed the position for many service-based businesses.

- Making Tax Digital and modern accounting software have reduced some of the historical administrative advantages.

- Business growth frequently changes whether the scheme remains commercially beneficial.

- Regular reviews are often more valuable than assumptions based on past circumstances.

- VAT decisions should support broader financial and operational objectives.

Frequently Asked Questions

What is the Flat Rate VAT Scheme?

The Flat Rate VAT Scheme is a simplified VAT accounting method that allows eligible businesses to pay a fixed percentage of VAT-inclusive turnover to HMRC instead of calculating VAT on most purchases and sales using standard VAT accounting rules.

Who can join the Flat Rate VAT Scheme?

HMRC generally allows eligible VAT-registered businesses with taxable turnover of £150,000 or less excluding VAT to join the scheme, subject to current rules and eligibility requirements.

When does a business need to leave the Flat Rate VAT Scheme?

A business will generally need to leave if it no longer meets HMRC eligibility requirements, including circumstances where turnover exceeds applicable exit thresholds.

Can VAT be reclaimed on purchases under the scheme?

In most cases, routine input VAT recovery is not available in the same way as under standard VAT accounting. Certain exceptions may apply for qualifying capital asset purchases.

What is a Limited Cost Trader?

A Limited Cost Trader is a business that spends relatively little on qualifying goods under HMRC rules. Businesses affected by these rules generally use the higher 16.5% flat-rate percentage.

Is the Flat Rate VAT Scheme suitable for consultants?

Some consultants benefit from the scheme because expenditure can be relatively low compared with turnover. However, the outcome depends on individual circumstances and cost structures.

Is the scheme suitable for e-commerce businesses?

E-commerce businesses often incur significant VATable expenditure on stock and operational costs. As a result, standard VAT accounting may sometimes provide a more favourable outcome.

Does Making Tax Digital apply to businesses using the Flat Rate VAT Scheme?

Yes. Businesses using the scheme may still need to comply with Making Tax Digital requirements where applicable, including digital record-keeping and VAT submissions.

How often should a VAT review be carried out?

Many businesses benefit from reviewing VAT arrangements whenever there are significant changes in turnover, expenditure, staffing, investment plans or business activities.

Final Perspective

The Flat Rate VAT Scheme remains a useful option for some UK SMEs, but its effectiveness depends on far more than the flat-rate percentage itself.

The Flat Rate VAT Scheme remains a useful option for some UK SMEs, but its effectiveness depends on far more than the flat-rate percentage itself.

The businesses that gain the greatest value from the scheme are often those that periodically reassess whether it still aligns with their commercial reality. Revenue changes. Cost structures evolve. Technology investment increases. New opportunities emerge.

A VAT arrangement that worked perfectly three years ago may still be the right choice today. Equally, it may no longer reflect how the business operates.

The strongest decisions tend to come from understanding the trade-offs rather than looking for a universally correct answer. The Flat Rate VAT Scheme is neither inherently good nor inherently bad. Its value depends on whether it continues to support the financial, operational and compliance needs of the business using it.