PAYE Adjustments for Multi-State or Cross-Border Employees: What UK Businesses Often Discover Too Late

Cross-border employment rarely creates problems on the first day.

The employee still appears on the UK payroll. Their salary still runs through the same software. The employment contract may still be governed by UK terms. The business still sees the arrangement as “temporary”, “hybrid” or simply “remote working from abroad for a while”.

In many cases, nothing initially looks operationally unusual.

The problems normally begin several months later.

Payroll records stop aligning properly with travel history. Foreign tax starts being deducted overseas. HR records no longer reflect actual working locations. National Insurance treatment becomes unclear. Employees ask why deductions differ between pay periods. Finance teams discover that overseas workdays were never tracked consistently in the first place.

This is usually the point where businesses realise cross-border PAYE is not simply a payroll processing issue. It is a wider employment tax, compliance and operational reporting issue that affects multiple parts of the business simultaneously.

Why Cross-Border PAYE Creates More Risk Than Many Employers Expect

Traditional PAYE systems were built around relatively stable employment patterns.

A UK-based employee works in the UK, is paid through UK payroll, and HMRC receives Real Time Information submissions that broadly reflect where duties are performed.

Cross-border employment changes that logic.

An employee may spend part of the year working overseas while remaining employed by a UK company. A director may split time across multiple jurisdictions while continuing to receive UK salary payments. A specialist employee may relocate temporarily while still performing duties connected to UK operations.

The payroll itself often continues uninterrupted.

What changes is the underlying tax and compliance reality sitting behind the payroll.

HMRC guidance makes clear that PAYE and National Insurance obligations can change depending on where duties are performed, how long overseas work continues, whether foreign tax applies, and whether social security agreements affect National Insurance treatment.

Many businesses underestimate how quickly these variables become operationally difficult once employees begin moving between jurisdictions regularly.

What Is Actually Changing Inside HMRC Payroll Compliance

One of the biggest changes in recent years is not necessarily legislation itself, but visibility.

HMRC increasingly operates within a more connected compliance environment where payroll reporting, international reporting standards, digital bookkeeping records, travel history, banking records and overseas reporting can eventually intersect.

Historically, some internationally mobile employees created relatively little scrutiny because the practical visibility of overseas working arrangements was lower.

That environment has changed significantly.

Remote working, hybrid international teams, overseas contractors transitioning into employees, founder relocation, international hiring and group-company structures have all increased the complexity of payroll compliance for UK businesses.

At the same time, many SMEs still operate payroll processes designed for fully domestic employment structures.

This creates a dangerous gap between operational reality and payroll reporting reality.

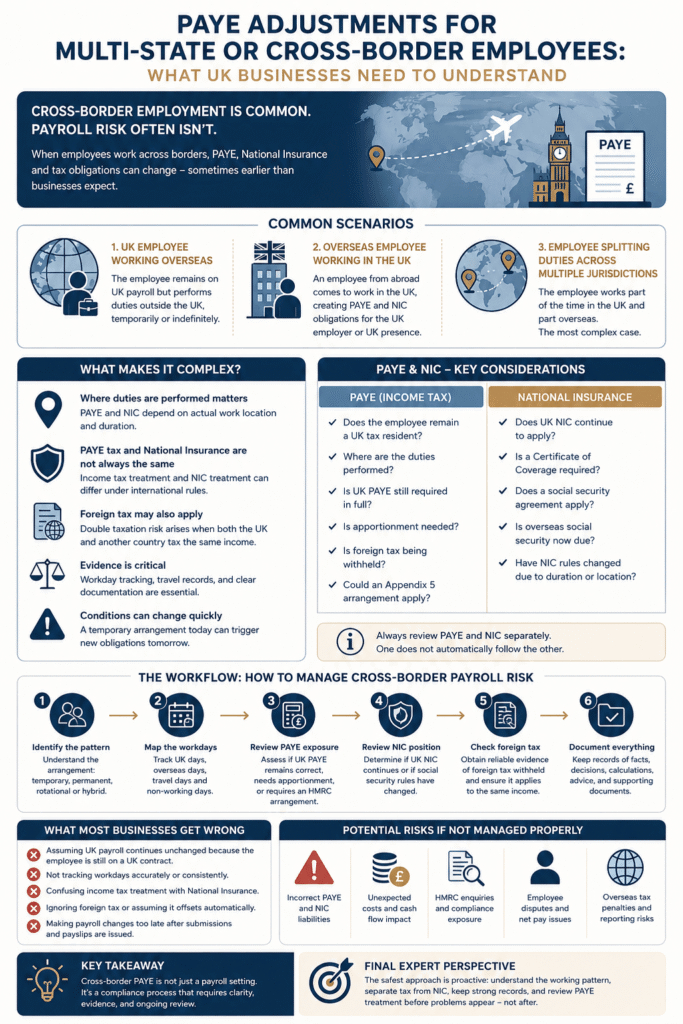

The Situations That Commonly Trigger PAYE Problems

UK Employees Working Overseas

UK Employees Working Overseas

UK Employees Working Overseas

UK Employees Working OverseasA UK employee may relocate temporarily for commercial expansion, project delivery, family reasons or flexible working arrangements. The business often assumes that because the employee remains on UK payroll, the PAYE treatment remains straightforward.

In reality, overseas workdays can affect tax exposure, National Insurance treatment and reporting obligations much earlier than expected.

Problems frequently begin when businesses fail to establish whether the overseas arrangement is temporary, rotational, indefinite or effectively permanent.

The distinction matters operationally because payroll assumptions often depend on it.

Overseas Employees Working in the UK

Businesses bringing employees into the UK from overseas sometimes incorrectly assume that foreign payroll arrangements remain sufficient simply because salary continues being paid abroad.

However, where duties are performed in the UK, PAYE obligations can still arise.

This becomes particularly sensitive when overseas parent companies, UK subsidiaries and group-company structures are involved. Payroll responsibility may not always sit where management initially assumes it does.

By the time the issue is identified internally, multiple payroll periods may already require review.

Employees Splitting Duties Across Multiple Jurisdictions

This is often where the operational complexity increases most aggressively.

The employee may spend part of the month in the UK, part overseas, and travel continuously throughout the tax year. Duties may be performed across multiple locations while salary continues flowing through a single payroll structure.

The payroll system itself may still process salary normally.

The difficulty is evidential.

Can the business clearly demonstrate where duties were performed? Are travel records consistent with payroll assumptions? Do HR records align with expense claims, calendars and overseas tax positions? Has anyone formally reviewed whether foreign withholding obligations now exist?

Many businesses only realise the gaps exist once reconciliation problems start appearing later.

Where Businesses Start Losing Control Operationally

Cross-border payroll problems rarely begin with tax calculations.

They usually begin with fragmented operational information.

HR may approve flexible overseas working informally. Payroll may never receive updated location information. Finance teams may only discover overseas working patterns after reimbursement claims or foreign tax correspondence appears months later.

Meanwhile, directors may assume that temporary overseas working arrangements do not materially affect PAYE because the employee “still works for the UK business”.

This creates a situation where the payroll itself continues functioning mechanically while the compliance foundation underneath it gradually becomes weaker.

By the time someone performs a proper review, multiple reporting periods may already be affected.

The Difference Between PAYE Risk and National Insurance Risk

One of the most misunderstood areas of international employment is the assumption that PAYE and National Insurance automatically follow the same rules.

They do not.

An employee may remain within UK National Insurance rules while overseas tax exposure changes separately. In other situations, overseas social security obligations may become relevant while UK PAYE treatment remains partially in place.

This is where businesses often oversimplify cross-border payroll into a single “international employee” category when the underlying tax and social security positions may require separate analysis.

Certificate of coverage requirements, social security agreements and overseas contribution rules can all materially affect the correct treatment.

Unfortunately, many smaller businesses only review National Insurance after discovering inconsistencies later during reconciliation or advisory reviews.

Why International Payroll Problems Escalate Quietly

International payroll problems are dangerous because they often remain operationally invisible for extended periods.

The employee still receives salary.

The payroll still processes.

Monthly submissions continue.

No immediate operational crisis appears.

Then secondary consequences begin surfacing.

Employees discover foreign tax withholding obligations. Overseas authorities request reporting information. PAYE adjustments become necessary retrospectively. Net pay inconsistencies appear. Directors realise travel records were never maintained properly. Finance teams struggle reconciling payroll with overseas reporting requirements.

At this stage, correcting the issue becomes significantly more complex than identifying it early would have been.

The Real Administrative Friction Behind Cross-Border Employees

Most businesses underestimate how much administrative discipline international payroll actually requires.

Most businesses underestimate how much administrative discipline international payroll actually requires.

The technical tax rules matter.

But the operational evidence matters just as much.

Businesses often need consistent records showing:

- where employees physically worked;

- which duties were performed in each jurisdiction;

- travel dates and workday allocation;

- whether overseas tax was deducted;

- whether UK National Insurance continued;

- whether overseas payroll obligations arose;

- how salary and bonuses were allocated across jurisdictions.

Without reliable records, payroll decisions become increasingly difficult to defend retrospectively.

This becomes especially problematic when employment arrangements evolve gradually rather than through formal secondment structures.

Practical HMRC and Payroll Scenarios Businesses Commonly Face

A growing UK consultancy allows a senior employee to work remotely from Spain for six months while continuing UK payroll unchanged. Several months later, the employee receives advice locally that Spanish tax obligations may now apply. The UK payroll team had never formally reviewed overseas workday exposure.

A UK technology company hires a specialist developer located overseas but operating closely with UK management. Salary is processed internationally, yet substantial duties are effectively connected to UK operations. Internal teams later discover the payroll structure does not fully reflect the practical working arrangement.

A founder-director regularly moves between the UK, UAE and Europe while continuing to receive UK salary payments. Travel patterns, board activity, management duties and tax residence assumptions gradually become difficult to reconcile consistently.

None of these situations necessarily begin as deliberate non-compliance.

Most begin as operational convenience.

The compliance risk develops later when documentation, payroll treatment and international working reality stop aligning properly.

What Most Companies Get Wrong About Remote International Working

The biggest misconception is assuming that remote working automatically remains “simple” if the employee remains employed by the UK company.

In practice, international remote work can affect:

- PAYE obligations;

- National Insurance treatment;

- foreign payroll exposure;

- double taxation risk;

- corporate tax presence risks;

- employment law considerations;

- benefits reporting;

- expense treatment;

- year-end reporting accuracy.

Businesses often focus only on whether salary can still be processed operationally.

The more important question is whether the wider compliance structure still reflects reality.

The Documentation and Evidence HMRC Normally Expects to Exist

Well-managed businesses usually create clearer internal payroll evidence much earlier in the process.

That often includes:

- formal overseas working approvals;

- documented travel timelines;

- workday allocation records;

- cross-border payroll reviews;

- foreign tax documentation;

- National Insurance position reviews;

- internal communication between payroll, HR and finance teams.

Importantly, these businesses usually treat international payroll as an ongoing compliance process rather than a one-time payroll adjustment.

That operational mindset alone often reduces long-term risk significantly.

How Better-Structured Businesses Usually Handle Cross-Border PAYE

Stronger businesses tend to identify international working patterns early instead of waiting for payroll inconsistencies to surface later.

Stronger businesses tend to identify international working patterns early instead of waiting for payroll inconsistencies to surface later.

They normally establish internal escalation procedures when employees relocate internationally, begin long-term overseas travel, or split duties across multiple jurisdictions.

More importantly, they understand that cross-border PAYE is rarely solved purely through payroll software.

It requires coordination between payroll, bookkeeping, finance, management, tax advisers and sometimes overseas specialists.

The businesses that manage this successfully are usually the ones that treat payroll data as part of a wider compliance ecosystem rather than an isolated monthly function.

The Wider Tax and Compliance Implications Businesses Often Overlook

PAYE is often only the visible part of the issue.

Cross-border employees can also affect:

- corporate residency analysis;

- permanent establishment exposure;

- benefits reporting;

- expense deductibility;

- director tax residency reviews;

- VAT implications;

- group-company recharge arrangements;

- year-end reporting consistency.

Many businesses initially approach international payroll as an isolated HR or payroll problem before later realising the wider tax ecosystem has also been affected.

Key Takeaways for UK Employers

Cross-border PAYE issues rarely become serious because payroll failed technically.

They usually become serious because the operational reality evolved faster than the compliance processes supporting it.

The businesses most exposed are often not those deliberately avoiding compliance, but those operating international employment arrangements without sufficient documentation, visibility or review procedures.

As international working structures become increasingly common, businesses that treat cross-border payroll as a wider strategic compliance issue will generally be far better positioned than those still approaching it as a routine payroll adjustment.

Final Expert Perspective

International employment has fundamentally changed how many UK businesses operate.

But in many organisations, payroll governance has not evolved at the same pace.

Cross-border PAYE is no longer a niche issue affecting only multinational corporations. It increasingly affects SMEs, founder-led businesses, remote-first companies, professional services firms and growing international teams.

The businesses that manage this well usually share one characteristic: they identify the compliance implications early, before payroll inconsistencies become reporting problems.

Because once international working arrangements become embedded operationally, correcting payroll treatment retrospectively is almost always more difficult, more expensive and more disruptive than structuring it properly from the beginning.

Prepared by Iryna Shmulenko, London, 2026