Common VAT Mistakes by Freelancers and How to Avoid Them

This article was prepared by the Audit Consulting Group team based on practical experience supporting UK freelancers, sole traders and small businesses with VAT registration, VAT reporting, bookkeeping and compliance-related matters. The content is intended for informational purposes only and reflects common operational challenges encountered by growing businesses in the UK.

Most freelancer VAT problems do not begin with a missed deadline.

They begin much earlier.

A designer lands several larger contracts in quick succession. A consultant starts working with clients on longer retainers. A developer begins taking on projects that are larger than anything completed previously. Revenue increases, workload increases, and attention naturally shifts towards delivery.

At that stage, VAT rarely feels like the biggest priority.

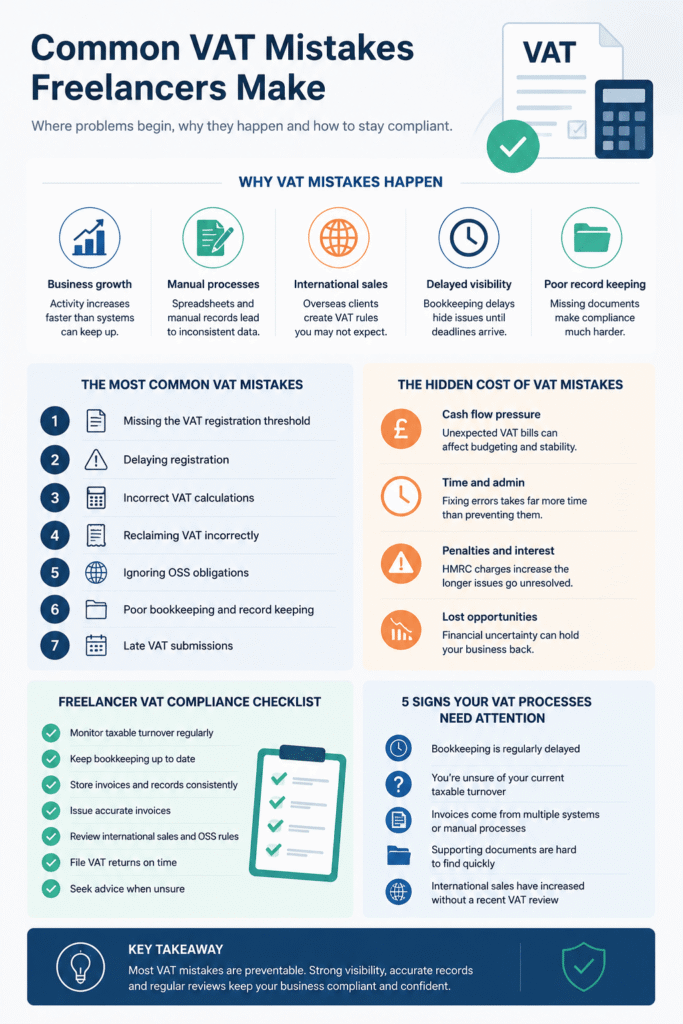

The irony is that the very period when a freelance business starts becoming more successful is often the period when VAT mistakes become most likely. Not because freelancers intentionally ignore their obligations, but because growth changes the administrative demands of a business faster than many people expect.

What worked when annual turnover was modest may no longer provide enough visibility once revenues begin moving towards VAT registration thresholds. Record-keeping habits that seemed perfectly adequate during the early stages of a business can start creating friction when VAT reporting becomes part of the picture.

Practitioners who regularly review VAT issues often notice the same pattern. The mistake itself is rarely the original problem. The real issue is usually that nobody recognised the warning signs while the problem was developing.

That distinction matters because VAT mistakes are often easier to prevent than they are to correct.

This article explores some of the most common VAT mistakes freelancers make in the UK, why those mistakes occur in practice, and how stronger business processes can reduce compliance risk before it becomes a larger administrative burden.

Why Successful Freelancers Often Encounter VAT Problems for the First Time

There is a common assumption that VAT difficulties mainly affect disorganised businesses.

Real-world experience suggests something different.

Many VAT issues appear in businesses that are growing.

A freelancer may spend years operating comfortably below the VAT registration threshold. Financial administration remains relatively straightforward. Revenue is predictable. Reporting requirements are familiar. Then growth arrives.

Growth changes everything.

More clients mean more invoices. More invoices mean more bookkeeping. More bookkeeping creates more opportunities for small inconsistencies to emerge. At the same time, the business owner usually has less spare time available to review administrative details because client work is demanding greater attention.

What makes VAT particularly challenging is that the consequences of a mistake often emerge months after the underlying issue first appears. By the time a problem becomes visible, the business may already have moved through multiple reporting periods.

For that reason, VAT compliance is often less about tax knowledge and more about operational visibility.

The businesses that avoid problems are not necessarily the businesses that know the most about VAT legislation. They are often the businesses that monitor turnover consistently, maintain reliable bookkeeping records and review changes in trading activity before compliance obligations are affected.

The Registration Threshold Is Not Usually the Real Problem

One of the most expensive freelancer VAT mistakes involves failing to recognise when registration should be considered.

Most freelancers are aware that a VAT registration threshold exists.

The threshold itself is rarely the issue.

Visibility is.

Many freelancers do not monitor taxable turnover as a dedicated business metric. Instead, they monitor cash in the bank, project pipelines, client activity and monthly revenue. While all of those measures are important, they do not necessarily provide a complete picture of when VAT obligations may be approaching.

A freelance marketing consultant might generate steady revenue throughout most of the year before securing several large contracts during a particularly successful quarter. Nothing about those individual contracts appears unusual. Viewed collectively, however, they may significantly alter the annual turnover position.

In practice, VAT thresholds are often crossed gradually rather than dramatically.

That is one reason why businesses sometimes identify the issue later than expected.

Understanding when VAT registration may become relevant requires more than reviewing annual revenue targets. It requires ongoing visibility into how turnover is developing throughout the year.

Where that visibility does not exist, VAT registration risks tend to increase.

Warning Signs Often Seen Before Registration Issues Emerge

- Monthly turnover is increasing significantly compared with previous years.

- Several large contracts have recently been secured.

- Revenue tracking relies primarily on bank balances rather than management reporting.

- Bookkeeping updates occur irregularly.

- The business owner is uncertain about current taxable turnover levels.

None of these indicators automatically mean a registration issue exists. Together, however, they frequently appear before registration-related problems are discovered.

When Delayed Registration Creates Larger Problems

Late registration is often discussed as though it were purely an administrative issue.

For many freelancers, the financial consequences can be more significant than the paperwork.

A common misunderstanding is that VAT obligations begin when a registration application is submitted. The reality can be more nuanced depending on when registration requirements arose and the circumstances involved.

This distinction becomes particularly important where invoices have already been issued, projects have already been completed and payments have already been received.

Practitioners frequently encounter situations where freelancers discover the issue retrospectively. The business owner is not trying to avoid VAT. They simply believed they still had time before registration became necessary.

By the time turnover figures are reviewed properly, the conversation changes.

The focus is no longer future compliance.

The focus becomes understanding historical exposure.

This is where VAT mistakes often begin affecting cash flow.

Revenue that appeared fully available for business use may suddenly need to support obligations that were not previously anticipated. That can create pressure even in otherwise successful businesses.

Importantly, delayed registration problems are rarely caused by a lack of effort. They are usually caused by a lack of timely information.

That is why stronger bookkeeping and financial reporting processes often prevent registration issues long before specialist VAT questions arise.

Invoice Errors Rarely Stay Isolated for Long

Once VAT registration has been addressed, attention naturally shifts towards invoicing.

This is another area where relatively small mistakes can create wider consequences.

An invoice is not simply a document sent to a client. It also becomes part of the evidence supporting bookkeeping records, VAT reporting, management information and future compliance reviews.

When invoice information is inconsistent, those downstream processes can become significantly more complicated.

Some invoice errors are obvious. Others are surprisingly difficult to identify until a VAT return is being prepared.

Examples include:

- incorrect VAT calculations;

- inconsistent treatment between clients;

- manual adjustments that are not properly documented;

- invoice records that do not reconcile with bookkeeping data;

- historical corrections that are not reflected consistently across systems.

What makes these issues problematic is that they rarely remain confined to invoicing alone.

An invoicing inconsistency often becomes a bookkeeping issue. The bookkeeping issue then becomes a reporting issue. The reporting issue can eventually become a compliance issue.

This chain reaction explains why experienced advisers frequently focus on process quality rather than individual transactions.

Reliable invoicing procedures support accurate bookkeeping, more consistent VAT filing and more dependable VAT submissions later in the reporting cycle.

When those procedures are weak, the administrative burden tends to grow over time rather than shrink.

The Problem With Reclaiming VAT Is Usually Documentation, Not Intent

Few freelancers deliberately claim VAT incorrectly.

Few freelancers deliberately claim VAT incorrectly.

Most reclaim-related problems arise because documentation standards fail to keep pace with business activity.

Early in a freelance career, expense volumes are often relatively low. Receipts are easy to locate. Purchases are memorable. Financial records remain manageable without formal systems.

As the business grows, that simplicity disappears.

Software subscriptions accumulate. Equipment purchases become more frequent. Travel costs increase. Professional services are used more regularly. What was once a handful of expenses each month can become hundreds of transactions spread across multiple platforms and suppliers.

The challenge is that VAT recovery depends on evidence.

Practitioners regularly encounter situations where freelancers know an expense occurred but cannot easily produce the supporting documentation needed months later. The expenditure itself may be entirely legitimate. The problem is proving it.

In practice, reclaim issues often begin long before a VAT return is prepared. They begin when documentation habits become inconsistent.

Businesses looking to maximise legitimate VAT reclaims and refunds typically benefit more from improving record quality than from attempting to identify additional claims.

One observation appears repeatedly across VAT reviews: businesses rarely regret maintaining stronger documentation. They frequently regret assuming they would remember where records were stored.

A Common Pattern

A freelance consultant purchases software, hardware and training resources throughout the year. Each expense is legitimate. Each expense supports business activity. However, invoices are saved across multiple inboxes, cloud folders and devices.

When VAT reporting is eventually prepared, finding the documentation becomes more difficult than recording the expenditure itself.

The challenge is not technical VAT knowledge.

The challenge is information management.

When Business and Personal Spending Become Difficult to Separate

Freelancers often operate closer to their businesses than larger organisations do.

That flexibility brings advantages. It can also create record-keeping complications.

Personal and business spending occasionally overlap. A phone may be used for both purposes. Travel may include both business and personal elements. Software may support multiple activities. Equipment may have mixed use.

The issue is not that mixed-use situations exist. The issue is that they require careful consideration and documentation.

Where separation is unclear, VAT reporting becomes more difficult. Bookkeeping reviews take longer. Supporting evidence becomes harder to assemble. Decisions that seemed straightforward when a purchase was made can become considerably less clear six or twelve months later.

One reason experienced advisers encourage stronger financial separation is not merely compliance. It is efficiency.

Businesses with clear boundaries between personal and business expenditure generally spend less time investigating historical transactions and more time focusing on productive activity.

The hidden cost of poor separation is rarely a single reporting issue. More often, it is the cumulative administrative burden created by uncertainty.

Most VAT Return Errors Start Long Before the Filing Deadline

There is a tendency to view VAT returns as standalone compliance events.

In reality, a VAT return is often the final output of months of financial activity.

By the time reporting begins, the quality of the outcome has already been heavily influenced by bookkeeping decisions made throughout the reporting period.

Missing invoices, uncategorised expenses, duplicate transactions and delayed bookkeeping updates rarely create immediate problems. They become visible when accurate figures are required.

This is why VAT reporting and bookkeeping are so closely connected.

When bookkeeping quality is strong, preparing a return is often relatively straightforward. When bookkeeping quality is inconsistent, reporting becomes an exercise in reconstruction.

Practitioners frequently observe that freelancers underestimate how quickly small bookkeeping delays accumulate. A week becomes a month. A month becomes a quarter. Eventually, VAT reporting deadlines arrive before records are fully prepared.

The result is additional pressure, additional uncertainty and additional risk of mistakes.

Example

A freelance web developer completes multiple projects during a busy quarter. Client deadlines take priority and bookkeeping updates are postponed. When reporting deadlines approach, invoices, expenses and payment records require extensive review before accurate figures can be produced.

The VAT return itself is not the source of the difficulty.

The backlog is.

This explains why businesses that maintain reliable bookkeeping processes often experience fewer VAT reporting problems than businesses that rely on periodic catch-up exercises.

Making Tax Digital Exposed Weak Processes More Than It Created New Ones

When Making Tax Digital (MTD) was introduced, many discussions focused on software.

When Making Tax Digital (MTD) was introduced, many discussions focused on software.

Software certainly matters.

However, one of the most significant lessons from MTD implementation has been that technology rarely fixes weak financial processes on its own.

Digital records can improve efficiency. They can improve visibility. They can reduce manual work. None of those benefits automatically improve data quality.

A poorly maintained bookkeeping system does not become accurate simply because it is digital.

This is why some businesses adapted to MTD relatively smoothly while others experienced ongoing difficulties. The difference often had less to do with software selection and more to do with process discipline.

Businesses that already maintained accurate records, reviewed transactions regularly and reconciled information consistently generally found the transition easier.

Businesses relying on retrospective corrections frequently discovered that MTD highlighted weaknesses which had existed for years.

Viewed through that lens, MTD is not merely a reporting requirement. It is also a visibility requirement.

It rewards businesses that maintain accurate financial information throughout the year rather than immediately before reporting deadlines.

International Work Creates VAT Questions Many Freelancers Never Previously Needed to Consider

One of the most significant changes in the freelance economy is how easy it has become to work internationally.

A consultant in Oxford may advise clients in Dublin. A designer in Manchester may serve customers throughout Europe. A developer in Bristol may sell digital products globally.

From a commercial perspective, this creates valuable opportunities.

From a VAT perspective, it introduces questions that may never have arisen previously.

Many freelancers begin operating internationally before fully appreciating how VAT treatment can differ depending on the nature of the service, the location of the customer and the reporting framework involved.

This does not mean international trading is inherently problematic.

It does mean assumptions become more dangerous.

Practitioners often encounter situations where businesses continue applying domestic thinking to transactions that require broader consideration.

For freelancers supplying qualifying services internationally, understanding areas such as VAT OSS registration and VAT OSS filing can become increasingly relevant as overseas activity expands.

The important point is not that international sales automatically create problems.

The important point is that growth into new markets often creates new compliance questions.

Questions that did not exist previously still need answers.

Why VAT Mistakes Often Become Cash-Flow Problems

Penalties receive most of the attention in discussions about VAT mistakes.

In practice, cash flow is often the more immediate concern.

Many VAT issues involve timing.

Revenue may already have been received. Expenses may already have been paid. Business decisions may already have been made based on the assumption that available funds would remain available.

When a historical VAT issue is identified, those assumptions can change.

That is one reason experienced advisers frequently view VAT as a business management issue rather than solely a tax issue.

Strong VAT processes support:

- more reliable financial forecasting;

- greater visibility over obligations;

- better cash-flow planning;

- more accurate reporting;

- reduced administrative disruption.

Weak VAT processes create the opposite effect.

Uncertainty increases. Administrative work expands. Financial visibility declines.

The underlying mistake may have been relatively small. The operational consequences often prove considerably larger.

This is why the most effective VAT strategies tend to focus on prevention rather than correction. Preventing a problem usually requires less time, less cost and less disruption than resolving one after it has already developed.

What Experienced Advisers Look for Before VAT Problems Appear

One of the most useful ways to think about VAT compliance is not to focus solely on mistakes that have already happened. A more valuable approach is identifying conditions that make mistakes more likely in the future.

In many cases, warning signs appear long before any reporting issue emerges.

A business owner may be unsure of current taxable turnover. Bookkeeping updates may be falling further behind each month. Financial records may be spread across multiple systems. International sales may be increasing without a corresponding review of VAT obligations.

None of these situations automatically indicate a compliance problem.

Collectively, however, they often suggest that financial processes are becoming less visible than they should be.

Experienced advisers frequently pay attention to process quality because process weaknesses tend to create reporting weaknesses later. By the time a VAT return highlights an issue, the underlying cause may have existed for months.

This is particularly relevant for freelancers because business growth can happen quickly. Administrative systems that worked perfectly well at one stage of development may become inadequate at the next.

The objective is not perfection. The objective is maintaining sufficient visibility to identify potential issues before they become expensive or time-consuming to resolve.

A Practical Framework for Reducing VAT Risk

While every freelance business is different, several habits consistently reduce the likelihood of VAT-related problems.

Perhaps the most important is reviewing financial information regularly rather than treating compliance as a periodic exercise.

Businesses that maintain ongoing visibility over turnover, expenses and reporting obligations generally identify issues earlier. Businesses that only review records immediately before filing deadlines often discover problems later, when available options may be more limited.

Another important consideration is recognising that VAT does not operate in isolation.

VAT reporting depends on bookkeeping.

Bookkeeping depends on record keeping.

Record keeping depends on consistent administrative processes.

When one part of that chain weakens, pressure often appears elsewhere.

For that reason, reducing VAT risk is often less about learning additional rules and more about strengthening the systems that support compliance activity throughout the year.

Businesses that maintain accurate records, review turnover regularly and address questions early are generally in a stronger position than businesses relying on retrospective corrections.

Questions Freelancers Should Ask Themselves Periodically

Several questions can help identify potential areas that may warrant further attention.

- Do I know my current taxable turnover position?

- Are bookkeeping records fully up to date?

- Can I easily locate supporting documentation for recent expenses?

- Have any significant changes occurred in my business model during the last twelve months?

- Have I started working with clients in additional countries?

- Do my invoicing processes remain appropriate for my current level of activity?

- Would I be confident explaining my records if questions arose later?

The value of these questions lies less in the answers themselves and more in the visibility they create.

Businesses rarely encounter difficulties because they asked too many compliance questions. Difficulties are more often associated with assumptions that remained unchallenged for too long.

Freelancer VAT Compliance Checklist

- Review taxable turnover regularly rather than relying on annual estimates.

- Monitor business growth that could affect VAT registration obligations.

- Maintain accurate and timely bookkeeping records.

- Store invoices and supporting documentation consistently.

- Separate business and personal expenditure wherever practical.

- Review invoice accuracy before issuing documents to clients.

- Ensure VAT reporting is based on complete financial information.

- Maintain digital records that support Making Tax Digital requirements.

- Review overseas trading activity periodically.

- Assess whether VAT OSS obligations may be relevant.

- Address uncertainties before reporting deadlines arrive.

- Review overall VAT compliance whenever significant business changes occur.

The Bigger Lesson Behind Most VAT Mistakes

Looking across the most common VAT mistakes freelancers make, a pattern begins to emerge.

Few problems start with VAT itself.

More often, they begin with visibility.

Turnover is not monitored closely enough. Documentation becomes fragmented. Bookkeeping falls behind. Business growth outpaces administrative processes. International activity expands without a corresponding review of reporting obligations.

The VAT issue is often the final symptom rather than the original cause.

This distinction is important because it changes how freelancers approach compliance.

Businesses that focus exclusively on deadlines may still encounter difficulties. Businesses that focus on maintaining accurate financial information throughout the year generally place themselves in a stronger position.

Reliable processes make compliance easier. Weak processes make compliance harder.

That principle applies whether a freelancer is approaching VAT registration for the first time, preparing regular returns, reviewing international sales activity or assessing broader VAT compliance obligations.

Final Perspective

Freelancers often assume VAT becomes relevant only when a reporting deadline approaches.

In reality, VAT compliance is shaped by decisions made throughout the year.

How revenue is monitored. How records are maintained. How invoices are issued. How business growth is reviewed. How new opportunities are assessed.

Those operational decisions frequently determine whether VAT remains a manageable administrative responsibility or develops into a larger compliance challenge later.

The encouraging reality is that most common VAT mistakes are preventable.

They are not usually prevented by memorising more regulations. They are prevented by creating stronger visibility over how the business operates.

For freelancers whose activities involve VAT registration, reporting, reclaims, compliance reviews or international transactions, understanding the broader VAT landscape is often just as important as understanding any individual rule. A well-structured approach to VAT services and compliance management can help ensure that business growth does not unintentionally create avoidable reporting challenges in the future.