Guide to Partial Exemption for UK Businesses: Explaining Complex VAT Rules Clearly

VAT is often treated as a mechanical tax. A business charges VAT, receives VAT invoices from suppliers, submits returns and pays or reclaims the difference.

Partial exemption is where that simple model starts to break.

For many UK businesses, the first warning sign is not a dramatic HMRC letter. It is usually something quieter: a VAT return that no longer feels straightforward, a new income stream that does not fit the usual pattern, or an accountant asking whether certain sales are taxable, exempt, zero-rated or outside the scope of VAT.

That question matters because partial exemption can directly affect how much input VAT a business is allowed to recover.

A business may be partly exempt where it makes, or intends to make, both taxable and exempt supplies and incurs VAT on costs connected with those activities. In practical terms, this means the business may not be able to reclaim all the VAT it pays on purchases, overheads and professional costs.

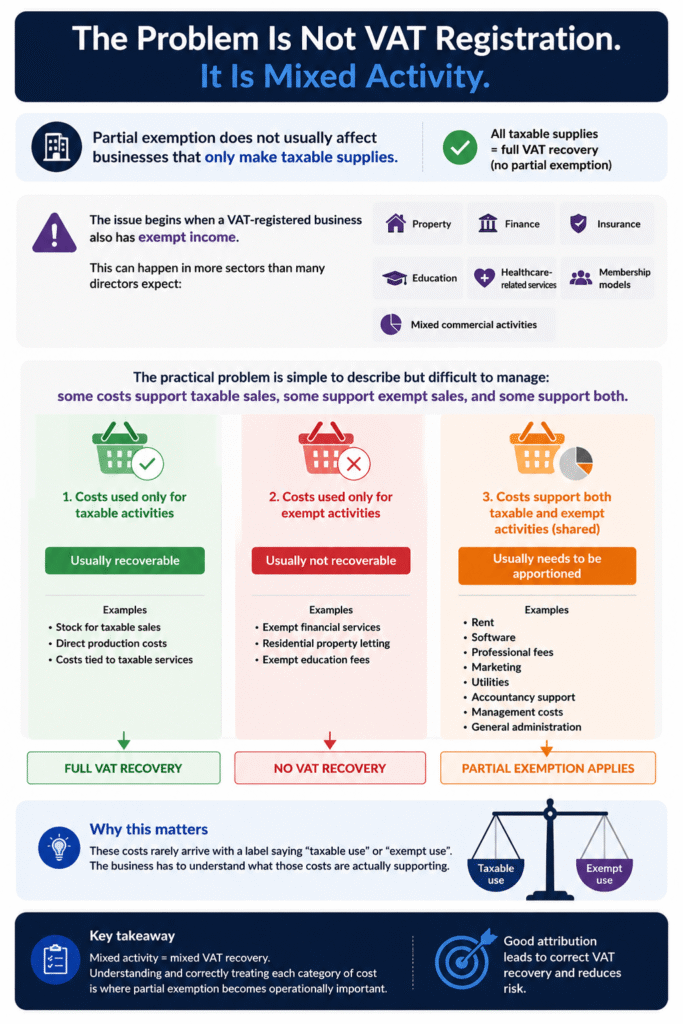

The Problem Is Not VAT Registration. It Is Mixed Activity.

Partial exemption does not usually affect businesses that only make taxable supplies.

The issue begins when a VAT-registered business also has exempt income. This can happen in more sectors than many directors expect. Property, finance, insurance, education, healthcare-related services, certain membership models and mixed commercial activities can all create VAT recovery questions.

The practical problem is simple to describe but difficult to manage: some costs support taxable sales, some support exempt sales, and some support both.

- VAT on costs used only for taxable activities is usually recoverable.

- VAT on costs used only for exempt activities is usually not recoverable.

- VAT on shared overheads usually needs to be apportioned.

That third category is where partial exemption becomes operationally important. It often includes rent, software, professional fees, marketing, utilities, accountancy support, management costs and general administration.

These costs rarely arrive with a label saying “taxable use” or “exempt use”. The business has to understand what those costs are actually supporting.

Why Exempt Income Changes the VAT Position

A common misconception is that exempt income is simply “VAT-free income”.

That is too simplistic.

Exempt supplies do not have VAT charged on them, but the business generally loses the right to recover input VAT connected with making those exempt supplies. This is why exempt income can reduce VAT recovery even when the business is fully VAT registered.

This distinction is crucial.

Zero-rated income and exempt income are not the same. A zero-rated supply is still taxable for VAT purposes, even though VAT is charged at 0%. Exempt income sits outside normal VAT recovery in a different way.

That is why partial exemption mistakes often happen when businesses group together anything with “no VAT charged” as if it were the same category.

It is not.

Where Partial Exemption Usually Appears in Real Businesses

Partial exemption is not only a large-company issue.

A small property business may rent commercial premises and also receive exempt residential rental income. A consultancy may provide standard-rated advisory work but also receive exempt finance-related income. A training provider may deliver a mixture of taxable and exempt education-related services. A growing company may add a new activity without realising that the VAT treatment of its income has changed.

In many cases, the business does not notice the problem immediately because the accounts still appear sensible. The profit and loss account may look correct. Sales may be recorded. Expenses may be categorised. Management reports may still be useful.

But the VAT recovery position may be wrong.

That is where partial exemption becomes dangerous. A bookkeeping system can show the right profit figure while still producing a VAT return that does not properly reflect taxable, exempt and mixed-use activity.

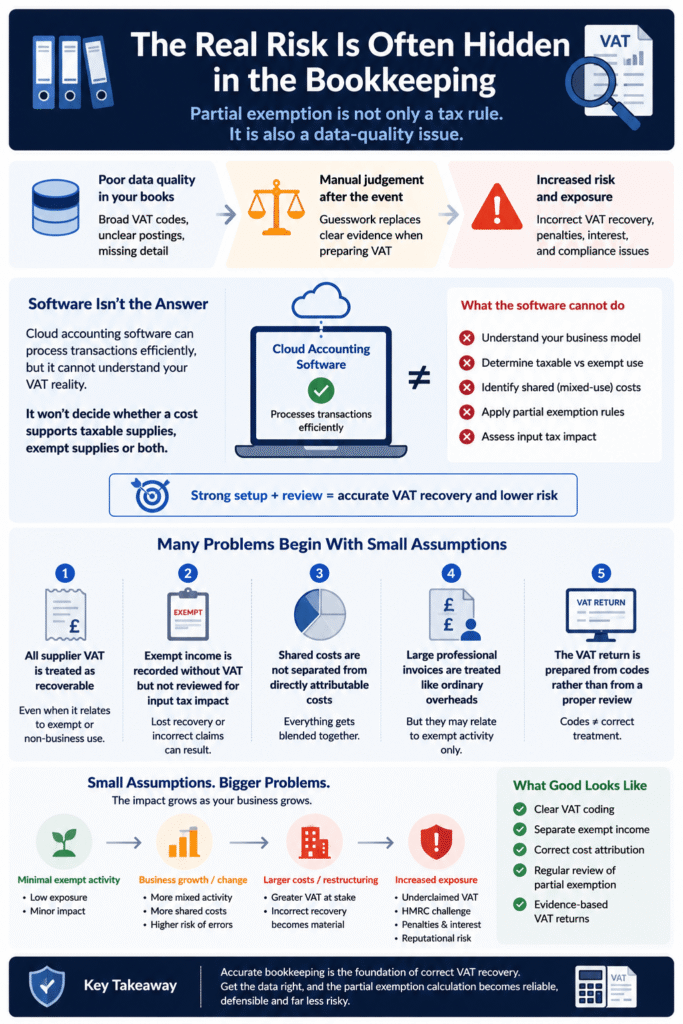

The Real Risk Is Often Hidden in the Bookkeeping

Partial exemption is not only a tax rule. It is also a data-quality issue.

If VAT codes are too broad, exempt income is not separated properly, or overheads are posted without enough detail, the VAT calculation becomes dependent on manual judgement after the event.

This is especially risky when a business uses cloud accounting software but has not built the chart of accounts around its VAT reality. The software may process transactions efficiently, but it cannot decide whether a cost supports taxable supplies, exempt supplies or both unless the setup and review process are strong enough.

Many problems begin with small assumptions:

- all supplier VAT is treated as recoverable;

- exempt income is recorded without VAT but not reviewed for input tax impact;

- shared costs are not separated from directly attributable costs;

- large professional invoices are treated like ordinary overheads;

- the VAT return is prepared from codes rather than from a proper partial exemption review.

Those assumptions may not matter much for a very small amount of exempt activity. But as the business grows, changes structure or incurs larger costs, the exposure can become more serious.

The Core Calculation: Attribution Before Recovery

Partial exemption is not just about applying a percentage.

The first step is attribution.

Input VAT needs to be identified according to what it relates to. If a cost is used only for taxable supplies, that input VAT is normally recoverable. If it relates only to exempt supplies, it is normally blocked. If it relates to both, it becomes residual input tax and must be apportioned using a partial exemption method.

Many businesses jump too quickly to the percentage calculation and miss the more important question: what is the cost actually supporting?

This matters because poor attribution can distort the final VAT recovery figure. For example, a legal invoice relating entirely to an exempt property transaction should not be treated in the same way as general accounting software used across the whole business.

The same applies to marketing, consultancy fees, software subscriptions, premises costs and finance-related advice. The VAT treatment depends on the connection between the cost and the business activity it supports.

The De Minimis Rule: Helpful, But Often Misread

The de minimis rule can allow some businesses to recover input VAT that would otherwise be restricted, provided the exempt input tax is insignificant.

In broad terms, exempt input tax may be treated as de minimis where it is no more than £625 per month on average and no more than half of total input tax incurred.

This is useful, but it is not a casual exemption from the rules.

Businesses still need to calculate exempt input tax correctly before deciding whether the de minimis test is met. The danger is assuming “we are probably below the limit” without evidence.

That assumption can be expensive if the business grows, changes activity, receives a large invoice, buys property, restructures services or starts generating more exempt income.

The de minimis rule should be treated as a test, not a shortcut.

Why the Standard Method May Not Always Reflect Reality

Many businesses use a standard partial exemption method based on the value of taxable supplies compared with total supplies.

This can work well in straightforward cases.

But sometimes it produces a result that does not reflect how the business actually uses its costs. A business may have high-value exempt income that requires little overhead support. Another business may have taxable activity that consumes most operational resources but generates lower turnover.

In those situations, the standard method may create a VAT recovery result that feels technically neat but commercially unrealistic.

That is where a special method may need to be considered. The point is not to create complexity for its own sake. The point is to make sure the VAT recovery method reflects economic and operational reality.

The Annual Adjustment Is Where Assumptions Get Tested

Partial exemption is not finished when quarterly VAT returns are submitted.

Businesses may need to complete an annual adjustment to compare provisional recovery during the year with the final position for the longer period. This is where small monthly assumptions can become visible.

For businesses with changing income patterns, seasonal activity, property transactions or irregular exempt income, the annual adjustment can materially change the VAT position.

It is also where weak records become a problem.

If the business cannot explain how input VAT was attributed, why a percentage was used, or how exempt input tax was assessed, the calculation becomes difficult to defend.

When Partial Exemption Becomes a Strategic Business Issue

Partial exemption often becomes more important when a business changes shape.

A new property transaction, a finance arrangement, a mixed service model, a restructure or a new exempt income stream can all affect VAT recovery.

The commercial decision may be correct, but the VAT impact needs to be understood before the business assumes that all input VAT remains recoverable.

This is particularly important where the business is investing in professional fees, development costs, refurbishment, software, premises or advisory support.

Losing recovery on part of those costs can affect cash flow, project budgets and profitability.

Partial exemption can also become visible during due diligence, refinancing, business sale preparation or external investment. A VAT recovery method that has never been properly documented may suddenly become a question for advisers, lenders or buyers.

That is why partial exemption should not be treated as a year-end technical adjustment. For some businesses, it is part of financial governance.

What Businesses Often Get Wrong

The most common mistake is treating partial exemption as an annual accounting clean-up.

The most common mistake is treating partial exemption as an annual accounting clean-up.

In reality, the quality of the calculation depends on how income and costs are recorded throughout the year.

Problems often appear when VAT codes are too generic, exempt sales are not separated properly, overhead costs are not reviewed, large one-off costs are treated automatically as recoverable, or directors do not tell their accountant when the business model changes.

A technical VAT issue can therefore become a systems issue.

If the bookkeeping setup cannot distinguish taxable, exempt and mixed-use activity, the VAT return becomes dependent on manual judgement after the event.

That is not where a business wants to be.

A Practical Workflow for Managing Partial Exemption

A sensible partial exemption process should not begin with the VAT return deadline.

It should begin with classification.

First, the business needs to identify its supplies: taxable, zero-rated, exempt and outside the scope where relevant. Then it needs to review purchases and overheads to decide which costs relate to taxable activity, exempt activity or mixed use.

After that, the business can calculate residual input tax, apply the correct method, test de minimis where appropriate and document the reasoning.

A good VAT file should explain:

- what income streams the business has;

- how supplies have been classified;

- how input tax has been attributed;

- which partial exemption method has been used;

- whether the de minimis test applies;

- what assumptions were made;

- whether any annual adjustment is required.

This is not paperwork for the sake of paperwork. It is evidence.

When Professional VAT Support Becomes Important

Not every business with exempt income needs a complicated VAT structure. But businesses should take partial exemption seriously where the amounts are material, the income mix is changing, or large costs are being incurred.

Professional support becomes especially important when a business is dealing with property income, finance-related activity, education or healthcare supplies, group restructuring, large capital expenditure, mixed-use overheads, or uncertainty around whether supplies are taxable or exempt.

The earlier the issue is reviewed, the easier it is to design a practical process. Waiting until several VAT periods have passed can make the review more difficult, because the business may need to reconstruct decisions from invoices, VAT codes and incomplete notes.

Partial exemption is much easier to manage when the bookkeeping, VAT treatment and advisory review are working together.

Final Expert Perspective

Partial exemption is difficult because it sits between tax law and operational reality.

Partial exemption is difficult because it sits between tax law and operational reality.

It is not enough to know that a business is VAT registered. It is not enough to have invoices with VAT on them. The real question is what the business does, what its income represents and how its costs support taxable and exempt activity.

For small businesses, the risk is usually not deliberate non-compliance. It is misunderstanding.

For growing businesses, the risk is often delay. The business model changes first. The VAT method catches up later.

A well-managed partial exemption process gives a business something more valuable than a calculation. It gives clarity: which VAT can be recovered, which VAT cannot, and where future decisions may change the position.

That clarity is what prevents a technical VAT rule from becoming a financial surprise.