First-Year Tax Planning for UK Startups: A Practical Guide

The first year of a UK startup is rarely tidy. Founders are usually dealing with product decisions, early customers, funding conversations, supplier problems, hiring choices and cash pressure at the same time. Tax planning can easily become something to revisit “once the business is properly trading”. That is often the first mistake.

First-year tax planning is not only about reducing a tax bill. For a startup, it is about building a reliable financial base: knowing which taxes may apply, keeping records that can survive scrutiny, understanding director responsibilities, avoiding avoidable penalties, and making decisions that do not create tax problems six or twelve months later.

The practical challenge is that tax obligations do not wait until a business feels established. HMRC, Companies House, payroll reporting, VAT thresholds, Corporation Tax, Self Assessment and record-keeping rules can all become relevant before a founder has had time to formalise internal processes. A startup does not need a complicated tax strategy from day one, but it does need a clear tax framework.

Leave your details and our team will get back to you shortly.

Why first-year tax planning starts before the first tax bill

New founders often think tax planning begins when profits appear. In reality, some of the most important tax decisions happen earlier: choosing a business structure, separating business and personal money, deciding how directors will be paid, setting up bookkeeping, understanding VAT exposure, and keeping evidence for expenses, investment and asset purchases.

These early choices affect how the business reports income, claims costs, pays tax, remunerates founders and manages cash. They can also affect investor confidence. A startup with unclear records, mixed personal spending and late filings may still have a promising product, but its financial credibility is weaker.

Good tax planning in the first year should help answer practical questions such as:

- Should the business operate as a sole trader, partnership or limited company?

- When does the startup need to register with HMRC?

- What records must be kept from the first transaction?

- How should founder pay be structured?

- Could VAT registration become necessary sooner than expected?

- Does the business need payroll from the start?

- Which expenses are genuinely allowable for tax purposes?

- What Corporation Tax, Self Assessment or Companies House deadlines apply?

The answers are rarely identical for every startup. A software company with pre-revenue development costs will have a different risk profile from an e-commerce seller approaching the VAT threshold, a consultancy with early profits, or a construction-related startup affected by CIS rules.

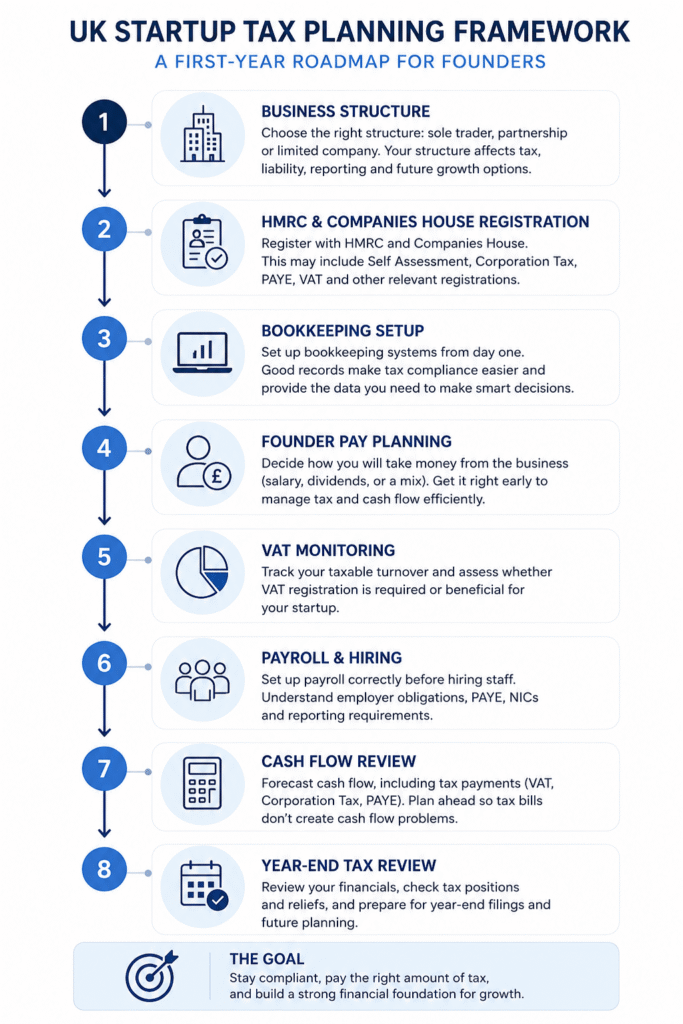

The first decision: business structure and tax consequences

For many UK startups, the first tax planning decision is the legal and tax structure. Some founders begin as sole traders because it is simple. Others incorporate a limited company early because they want limited liability, share ownership, investor readiness or a clearer distinction between the founder and the business.

A sole trader structure is usually easier to administer at the beginning. Income and expenses are reported through Self Assessment, and the individual is taxed on business profits. However, the founder and the business are legally the same person, which can create limitations as the venture grows or takes on commercial risk. Founders testing a business before incorporation should still understand self-employed registration requirements so early trading is not left outside the tax record.

A limited company is a separate legal entity. It pays Corporation Tax on taxable profits, files accounts and a confirmation statement with Companies House, and has directors with statutory responsibilities. Directors may receive salary, dividends, reimbursed expenses or a combination, but each route has different tax and reporting implications.

The limited company route is not automatically better. It can be more tax-efficient in some circumstances, especially where profits are retained for growth, but it also brings more administration. Poorly maintained company records can quickly undermine any theoretical tax advantage.

First-year planning should therefore consider not only the current tax position, but also how the business expects to grow. A founder planning to raise investment, issue shares, hire staff or work with larger corporate clients may need a different structure from someone testing a small side venture.

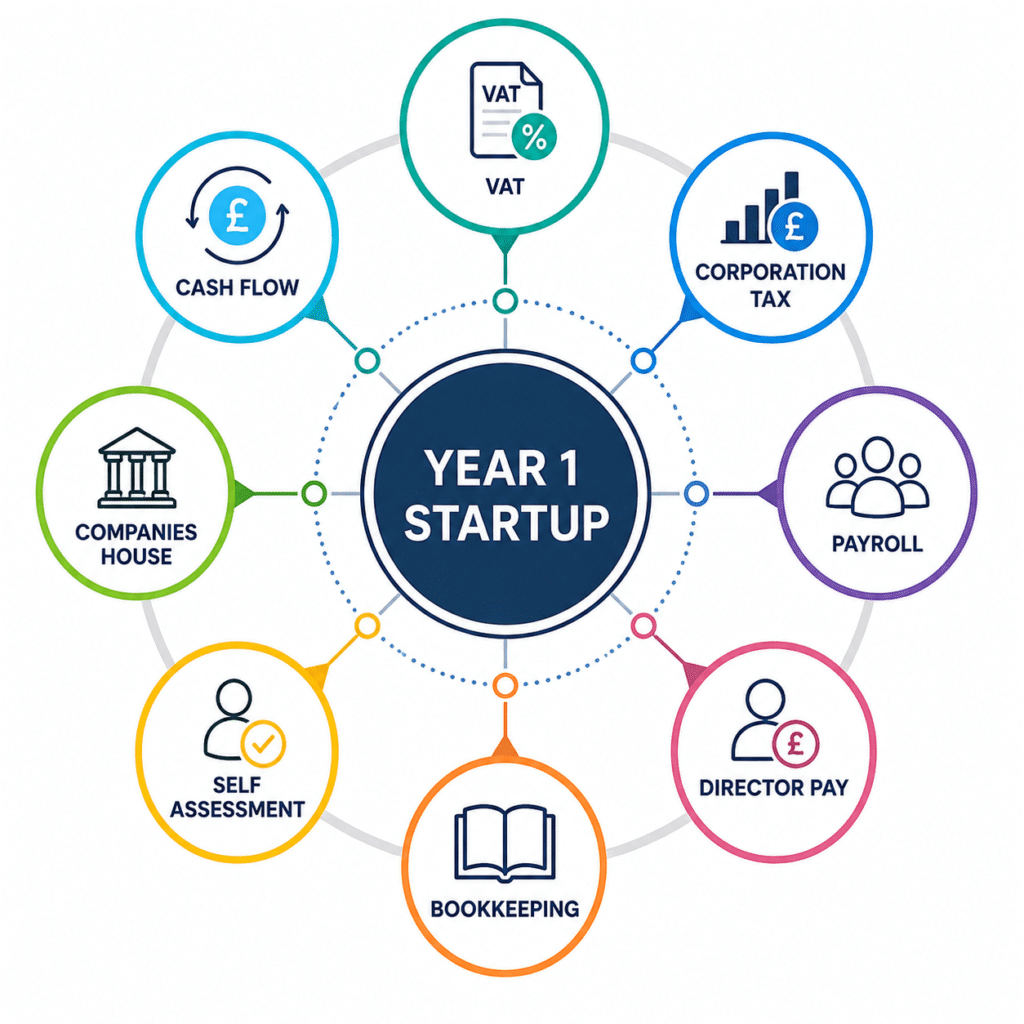

HMRC registration is not a single event

One common misunderstanding is that “registering the business” deals with everything. In practice, several registrations may be relevant, depending on the structure and activities of the startup.

A self-employed individual normally needs to register for Self Assessment. A limited company must be registered with Companies House and then deal with Corporation Tax registration. If the company pays employees or directors through salary, PAYE registration may be required. If taxable turnover exceeds the VAT registration threshold, or if voluntary registration makes sense commercially, VAT must be considered. Construction-sector businesses may also need to assess CIS obligations.

Each registration carries its own reporting rhythm. Self Assessment follows the personal tax year. Corporation Tax is linked to the company’s accounting period. PAYE submissions are usually made in real time through Real Time Information. VAT returns follow the VAT period. Companies House filings have their own deadlines, separate from HMRC.

This is where startups often lose control. The founder remembers one deadline but misses another. Or they assume the accountant can reconstruct everything later, even though invoices, receipts, bank explanations and payroll decisions were never properly documented.

Bookkeeping is the foundation of startup tax planning

Tax planning without bookkeeping is guesswork. A startup may have clever projections, but if actual income and costs are not recorded correctly, the business cannot understand its tax position, cash runway or filing obligations.

In the first year, bookkeeping should capture more than bank transactions. It should explain what the transaction was for, whether it was business-related, whether VAT applies, whether the cost is allowable for tax, whether it relates to an asset, and whether it should be treated differently in the accounts.

Typical first-year records include:

- sales invoices and customer receipts;

- supplier invoices and purchase receipts;

- bank statements and payment records;

- loan agreements or founder funding records;

- share capital and investment documentation;

- payroll records and director salary details;

- mileage and travel evidence;

- software subscriptions and equipment purchases;

- VAT evidence where VAT is charged or reclaimed.

Good records are not only useful for tax returns. They help founders see whether gross margins are real, whether pricing is sustainable, whether cash is being absorbed by stock, whether contractors are becoming a fixed cost, and whether the business can afford to hire.

A surprisingly common issue is the founder who uses one bank account for everything during the “testing” phase. By the time the business grows, personal spending, startup costs, director withdrawals and customer receipts are mixed together. The cleanup can take longer than setting up basic bookkeeping properly at the start.

Corporation Tax planning for first-year limited companies

For limited company startups, Corporation Tax is usually one of the central first-year concerns. The company pays Corporation Tax on taxable profits, not simply on cash in the bank. This distinction matters. A business may have cash because it received investment or a loan, but that does not necessarily mean it has taxable profit. Equally, a business may have taxable profit even if cash is tight because customers are slow to pay.

Corporation Tax planning in the first year should focus on understanding taxable profit, allowable expenses, capital expenditure, losses and timing. Early losses may be available for relief, but the treatment depends on the facts. Development costs, equipment, software, professional fees and pre-trading expenses should be reviewed carefully rather than assumed to be automatically deductible in the way the founder expects.

The company must also file a Company Tax Return with HMRC and accounts with Companies House. These are connected but not identical obligations. Companies House accounts are public documents, while the Corporation Tax return provides HMRC with tax computations and supporting figures.

For first-year companies, accounting periods can cause confusion. The company’s first accounts may cover a period that differs from the Corporation Tax accounting period, especially if the first period is longer than twelve months. This can lead to more than one Corporation Tax return for the first set of accounts. Founders are often unaware of this until filing deadlines approach.

Founder pay: salary, dividends and the cash discipline problem

Paying founders is one of the areas where first-year tax planning becomes practical rather than theoretical. A director of a limited company cannot simply treat company money as personal money. Withdrawals need to be classified properly: salary, dividend, expense reimbursement, director’s loan or another form of payment.

Salary may require PAYE reporting and can affect National Insurance. Dividends can only be paid from available distributable profits and require appropriate company records. Director’s loan accounts need careful monitoring because overdrawn balances can create tax consequences for both the director and the company.

The issue is not only tax efficiency. It is cash discipline. A founder who withdraws money irregularly without understanding the classification may leave the company short of funds for VAT, payroll taxes, Corporation Tax or suppliers. The accounts may later show that what felt like “taking some money out” was actually an overdrawn director’s loan or an unlawful dividend.

Early planning should set a realistic approach to founder remuneration. In some startups, low or no salary may be sensible while cash is being reinvested. In others, a modest salary and later dividends may be appropriate. The right answer depends on profits, cash flow, personal tax position, National Insurance, other income, shareholder arrangements and future funding plans. More developed limited companies may also need to consider corporate tax planning where retained profits, investment timing and director remuneration interact.

VAT: the threshold is not the only issue

VAT is often treated as a problem for later, once sales are higher. That can be risky. A startup must monitor taxable turnover against the VAT registration threshold on a rolling basis, not just at the end of the year. Fast-growing sales, a successful launch or a large contract can bring VAT into scope earlier than expected.

Voluntary VAT registration may also be worth considering in some cases, particularly where the startup sells mainly to VAT-registered businesses and has significant input VAT on costs. But voluntary registration can be unattractive for businesses selling to consumers, where VAT may make pricing less competitive if it cannot be passed on comfortably.

VAT planning should look at customer type, pricing, margins, input VAT, cross-border transactions, digital services, marketplace sales and administrative capacity. The commercial question is often as important as the tax question: can the startup absorb VAT, charge it, reclaim it correctly and file returns accurately?

The first-year mistake is usually not failing to understand VAT theory. It is failing to monitor turnover and pricing in real time. By the time the founder notices, the business may have crossed the threshold and may need to deal with registration, backdated VAT issues or pricing adjustments.

Payroll and hiring: tax planning before the first employee starts

Hiring creates another layer of tax and compliance. Once a startup employs staff, it may need PAYE registration, payroll software or payroll support, Real Time Information submissions, pension auto-enrolment assessment, payslips and proper employment records.

Even where the first worker is a founder-director, payroll may still be relevant if salary is paid. For contractors and freelancers, the business must consider whether the relationship is genuinely self-employed or whether employment status risks exist. In some sectors, off-payroll working rules, agency arrangements or CIS rules can add further complexity.

Payroll errors in the first year can be expensive to fix because they often involve repeated submissions. Incorrect tax codes, late FPS filings, unpaid PAYE, missing pension assessments or casual arrangements with workers can create administrative pressure at the worst possible time.

A practical first-year payroll plan should clarify who is being paid, under what arrangement, how often, through which system, and what evidence supports the treatment. Startups often move quickly, but HMRC and employment compliance still expect the records to make sense.

Allowable expenses: where founders overclaim and underclaim

Startup founders frequently misunderstand business expenses in both directions. Some claim costs that are not properly allowable. Others fail to claim legitimate costs because they do not have records or assume small items are not worth tracking.

An expense is not allowable simply because it helped the founder feel ready to trade. The cost must normally be incurred wholly and exclusively for business purposes, though some expenses have specific rules or mixed-use treatment. Travel, home working, mobile phones, subscriptions, equipment, client entertainment, training and clothing are areas where assumptions often go wrong.

Pre-trading expenses also need care. Costs incurred before the business formally starts trading may be deductible in some circumstances if they meet the relevant conditions, but the timing, nature of the cost and business structure matter.

The better approach is to record costs properly and review treatment rather than make rough decisions at the year end. This protects the business in two ways: it avoids careless overclaims, and it reduces the chance of missing legitimate reliefs.

Self Assessment does not disappear just because there is a company

Directors and shareholders sometimes assume that incorporation removes personal tax reporting. That is not always the case. A director may still need to file a Self Assessment tax return depending on income, dividends, benefits, other earnings, rental income, overseas income or HMRC requirements.

Dividends are particularly relevant for founder-shareholders. The company may pay Corporation Tax on its profits, but dividends received by individuals have their own personal tax treatment. Salary and dividends are taxed differently, and the combined position should be reviewed rather than treated as separate decisions.

For founders who begin self-employed and later incorporate, the first year can involve both Self Assessment and company reporting. The transition needs careful record-keeping so income and expenses are allocated to the correct period and structure.

Companies House obligations are part of tax planning, not an afterthought

Companies House does not collect Corporation Tax, but company filing obligations still matter for tax planning. Accounts filed at Companies House create a public record. Confirmation statements keep company information up to date. Changes to directors, shareholders, registered office, share capital or persons with significant control may need to be recorded correctly.

A startup preparing for investment, lending or due diligence cannot afford messy statutory records. Investors and lenders may review Companies House filings before they look at detailed management information. Inconsistencies between shareholder agreements, accounts, confirmation statements and internal records can raise questions that delay transactions.

For first-year companies, the discipline is simple but often neglected: keep statutory records aligned with the commercial reality of the business. If shares are issued, directors change, or ownership arrangements evolve, the paperwork should not be left until the next funding round.

Cash flow is where tax planning becomes visible

A startup can be profitable on paper and still struggle to pay tax. This is especially common where cash is tied up in stock, customers pay late, upfront costs are high, or the company has reinvested heavily.

First-year tax planning should include cash reservations. The business should estimate Corporation Tax, VAT, PAYE and personal tax exposure before the deadlines arrive. These estimates do not need to be perfect, but they should be realistic enough to prevent the founder from mistaking tax money for available spending cash.

Cash planning becomes particularly important where the business collects VAT from customers or deducts PAYE from employees. Those amounts are not normal trading profit. They are liabilities that will need to be paid over to HMRC.

A useful habit is to review tax exposure monthly or quarterly, not only once a year. This gives founders time to adjust dividends, spending, pricing, hiring or investment decisions before cash pressure becomes acute.

Where first-year startups usually go wrong

The most damaging tax mistakes in the first year are often ordinary administrative failures rather than sophisticated planning errors. They happen because the founder is moving quickly and assumes the finance function can be tidied later.

- Leaving bookkeeping too late: reconstructing months of activity from bank statements is slower, less accurate and more expensive than maintaining records as the business trades.

- Mixing personal and business money: this creates confusion around expenses, director withdrawals, capital introduced and taxable income.

- Ignoring VAT until a threshold is crossed: turnover must be monitored continuously, especially in fast-growth or seasonal businesses.

- Taking dividends without checking profits: dividends need distributable profits and proper documentation.

- Missing separate filing systems: HMRC and Companies House deadlines are not the same, and different taxes follow different cycles.

- Using contractors casually: worker status, CIS and payroll obligations should be assessed before payment routines become embedded.

- Not preserving evidence: a bank transaction alone may not prove what was bought, why it was business-related or whether VAT can be reclaimed.

None of these issues means the startup is badly run. They are typical symptoms of a young business where operations have outpaced administration. The risk is allowing them to continue until they become expensive to correct.

A practical first-year tax planning workflow

A workable first-year tax process does not need to be elaborate. It needs to be consistent. The aim is to create enough structure that the founder can make decisions with current information rather than historic estimates.

The first step is to confirm the business structure and registration position. This includes HMRC registration, Companies House incorporation where relevant, PAYE, VAT and any sector-specific obligations such as CIS.

The second step is to set up bookkeeping from the first transaction. A dedicated business bank account, accounting software, document capture and a clear chart of accounts can prevent most early record problems. The system should identify income, direct costs, overheads, capital expenditure, taxes owed, loans, shareholder funds and director transactions.

The third step is to decide how founders and staff will be paid. This should be documented and reviewed as profits and cash flow change. A startup may begin with one approach and adapt later, but undocumented withdrawals are rarely helpful.

The fourth step is to monitor tax-sensitive triggers. These include VAT turnover, payroll changes, dividend capacity, taxable profit, director loans, major asset purchases, funding receipts and approaching filing deadlines.

The fifth step is to schedule review points. A quarterly review is often enough for a very early-stage business, while startups with payroll, VAT, stock, funding or rapid growth may need more frequent management accounts. The review should not only ask “what tax is due?” but “what decisions are we making now that will affect tax later?”

Different startup models, different tax pressure points

Not all startups face the same first-year tax risks. A consulting startup may become profitable quickly with low overheads, making Income Tax or Corporation Tax planning relevant early. A technology startup may have significant development costs and little revenue, making loss treatment, investment records and R&D-related evidence more important. An online seller may need to watch VAT, stock records, import costs and marketplace data. A construction-related startup may need to address CIS before the first subcontractor payment.

Startups with external investment have additional documentation needs. Funds received from investors are not normal trading income, but share issues, loan notes, SEIS or EIS considerations, cap tables and legal documentation must be handled carefully. Poor records can create problems later even where the tax position was manageable at the time.

Startups with international activity should be especially cautious. Overseas customers, suppliers, remote workers, digital services, imports, exports and foreign platforms can introduce VAT, payroll, withholding tax or permanent establishment questions. These are not always urgent from day one, but they should be identified early enough to avoid accidental non-compliance.

What founders should review before the first year end

The first year end should not be the first serious look at tax. By then, many options may be limited and missing records may be hard to recover. A pre-year-end review gives the business time to correct errors, organise documentation and understand the likely tax position.

Useful review questions include:

- Are all income streams recorded and reconciled to bank receipts?

- Are expenses supported by invoices, receipts or clear evidence?

- Have director withdrawals been classified correctly?

- Is the company able to support any dividends paid?

- Has VAT turnover been monitored on a rolling basis?

- Are payroll filings complete and consistent with actual payments?

- Are pre-trading costs and capital purchases identified separately?

- Are Companies House records accurate and up to date?

- Is there enough cash reserved for tax liabilities?

- Have any losses, reliefs or timing issues been reviewed before filing?

This review is less about finding clever tax savings and more about preventing avoidable surprises. For a young business, certainty and clean records can be as valuable as marginal tax efficiency.

Tax planning should support the business, not distort it

There is a temptation for new founders to chase tax efficiency before the business model is stable. That can lead to over-engineered structures, awkward remuneration arrangements or decisions made for tax reasons that do not fit the commercial reality.

Good first-year tax planning is proportionate. It recognises the stage of the business. It protects compliance, keeps cash visible, avoids careless mistakes and leaves room for growth. It should not force a startup into complexity before the benefits justify the administration.

The strongest approach is usually to build a reliable finance routine early: clean bookkeeping, sensible registration decisions, regular reviews, documented founder pay, VAT monitoring and clear separation between personal and business money. From that base, wider tax services may become relevant as profits, staff, investment and risk increase, but the first priority is a tax position the business can explain.

Key takeaways for UK startup tax planning

- First-year tax planning begins with structure, registrations, records and cash discipline, not only the final tax return.

- Limited companies must manage Corporation Tax, Companies House filings, director pay and statutory records as separate but connected responsibilities.

- Self-employed founders need to plan for Self Assessment, National Insurance and accurate business expense records.

- VAT should be monitored before the threshold is reached, especially where sales grow quickly or pricing is sensitive.

- Payroll obligations can apply earlier than expected, including for director salaries and first hires.

- Founder withdrawals need proper classification; company money is not personal money.

- Reliable bookkeeping is the practical foundation for every tax decision in the first year.

- Regular review points help prevent tax liabilities from becoming cash flow shocks.

A first year that is easier to explain is usually easier to manage

Tax planning for a UK startup is not about predicting every future outcome. The first year will involve changes, incomplete information and decisions made under pressure. The aim is to keep the business explainable: to HMRC, to Companies House, to investors, to lenders, to co-founders and to the founders themselves.

If the records show what happened, why it happened and how it was treated, the startup has a stronger foundation. Tax returns become less stressful. Cash planning becomes more realistic. Funding conversations become cleaner. Directors can make decisions with fewer unknowns.

The startups that handle first-year tax well are not always the ones with the most complex planning. They are usually the ones that put basic financial discipline in place early enough for the business to grow without dragging unresolved compliance issues behind it.