VAT Treatment of Subscriptions and Digital Services: What UK Businesses Need to Understand

Recurring revenue has become one of the defining features of the modern digital economy. Software companies build subscription-based platforms, training providers sell ongoing access to educational content, creators launch paid memberships, and professional service firms increasingly package expertise into monthly plans rather than one-off engagements.

Commercially, the model is attractive. Subscription revenue can improve cash-flow visibility, strengthen customer retention and create more predictable growth patterns. From a VAT perspective, however, recurring payments often create a misleading impression that the underlying tax treatment must also be straightforward.

In reality, some of the most complex VAT questions facing modern businesses emerge from products that appear deceptively simple on the surface. A monthly subscription collected automatically through a payment gateway may involve multiple jurisdictions, different customer types, varying place of supply rules and evidence requirements that are rarely considered during the initial stages of growth.

One pattern that frequently appears during VAT reviews is that businesses focus heavily on customer acquisition, product development and recurring revenue metrics while VAT assumptions remain largely unchanged from the day the business launched. For a period of time, this often causes no visible issues. The complications tend to emerge later, usually when the business expands internationally, approaches VAT registration thresholds, attracts investment or undergoes a more detailed financial review.

By the time the issue becomes visible, the challenge is rarely the VAT return itself. The challenge is reconstructing historical customer data, transaction evidence and reporting decisions that were never designed with future compliance requirements in mind.

This is why understanding the VAT treatment of subscriptions and digital services is no longer relevant only to accountants. For many businesses, it has become part of the operational architecture that supports sustainable growth.

Why Digital Revenue Creates VAT Challenges Traditional Businesses Never Faced

Historically, VAT systems evolved around physical goods and conventional service delivery. A supplier sold products within a particular territory, invoices were issued directly to customers and the location of the transaction was generally obvious.

Digital business models have changed those assumptions.

A SaaS company based in the UK can acquire customers across Europe, North America and Asia before employing its first member of staff. A membership platform can generate recurring revenue from dozens of countries within weeks of launch. An online course provider can scale internationally without opening offices, employing local teams or establishing a physical presence in the markets where customers are located.

Commercial barriers have become significantly lower. Compliance expectations have not disappeared alongside them.

HMRC and tax authorities around the world have increasingly focused on ensuring that digital supplies are taxed appropriately, regardless of whether a transaction involves physical delivery. As a result, businesses operating entirely online often encounter VAT questions that would rarely arise in traditional local service businesses.

This is particularly relevant for:

- SaaS companies;

- software developers;

- subscription platforms;

- membership communities;

- online course providers;

- digital publishers;

- app developers;

- cloud service providers;

- digital product sellers;

- content subscription businesses;

- e-learning platforms;

- online marketplaces.

Although these business models appear different commercially, they often encounter remarkably similar VAT challenges as revenue grows.

Why the Word “Subscription” Tells You Almost Nothing About VAT Treatment

One of the most persistent misconceptions in this area is the belief that subscriptions represent a distinct VAT category.

One of the most persistent misconceptions in this area is the belief that subscriptions represent a distinct VAT category.

They do not.

A subscription describes how a customer pays. It does not determine what is being supplied.

This distinction sounds obvious, yet it sits behind a significant number of VAT misunderstandings.

Consider the following examples:

- a Netflix subscription;

- a software licence billed monthly;

- a cloud storage platform;

- a digital newspaper subscription;

- a professional membership organisation;

- a recurring coaching programme;

- a subscription-based legal support service;

- a monthly bookkeeping support package.

All involve recurring payments. Yet the underlying supplies differ significantly.

For VAT purposes, the starting point is not how often payment is collected. The starting point is identifying what the customer is actually purchasing.

Businesses are often surprised to discover that two subscription models generating identical recurring revenue can produce very different VAT outcomes because the nature of the supply differs.

This becomes particularly important where subscriptions combine multiple components.

A modern membership platform may include:

- recorded educational content;

- software tools;

- downloadable resources;

- live webinars;

- private communities;

- expert Q&A sessions;

- implementation support;

- consulting access.

Commercially, this may be presented as a single product.

From a VAT perspective, understanding what customers are primarily paying for can become considerably more important than the billing frequency itself.

What HMRC Generally Considers a Digital Service

Although individual circumstances always matter, digital services are generally characterised by electronic delivery and a significant degree of automation.

Examples commonly include:

- software subscriptions;

- cloud-hosted applications;

- downloadable software;

- mobile applications;

- online databases;

- streaming platforms;

- digital publications;

- website hosting services;

- automated online tools;

- downloadable media;

- digital memberships;

- automated course libraries.

One factor that frequently influences VAT analysis is the degree of human involvement required to deliver the service.

An automated software platform generally presents a different VAT profile from a consultant providing bespoke advice through video meetings, even if both businesses operate entirely online.

Similarly, a self-paced educational library may be viewed differently from a programme built primarily around live instructor-led delivery.

A recurring observation during compliance reviews is that businesses often focus on how a product is marketed while HMRC is more interested in how the product is actually delivered.

The distinction matters because the VAT treatment frequently depends on the substance of the supply rather than the commercial language used to describe it.

The Hidden Complexity of Hybrid Subscription Models

Many modern digital products sit somewhere between purely automated digital services and traditional professional services.

These hybrid models have become increasingly common.

A membership platform may include software access, educational content and live support. A SaaS product may incorporate consulting services. An online learning platform may combine automated lessons with monthly workshops and personalised feedback.

From a growth perspective, these blended offerings can be extremely effective.

From a VAT perspective, they often require a more careful assessment than founders initially expect.

One recurring issue is that businesses continue applying the VAT assumptions created for the original version of a product long after the product itself has evolved.

A service that began as a simple software subscription may gradually incorporate training, implementation support, advisory services and premium account management. The commercial offer changes significantly, yet the VAT treatment remains based on assumptions made several years earlier.

By the time somebody revisits those assumptions, substantial transaction volumes may already exist.

This is one reason periodic VAT reviews often identify issues that were not created by deliberate errors but by gradual product evolution.

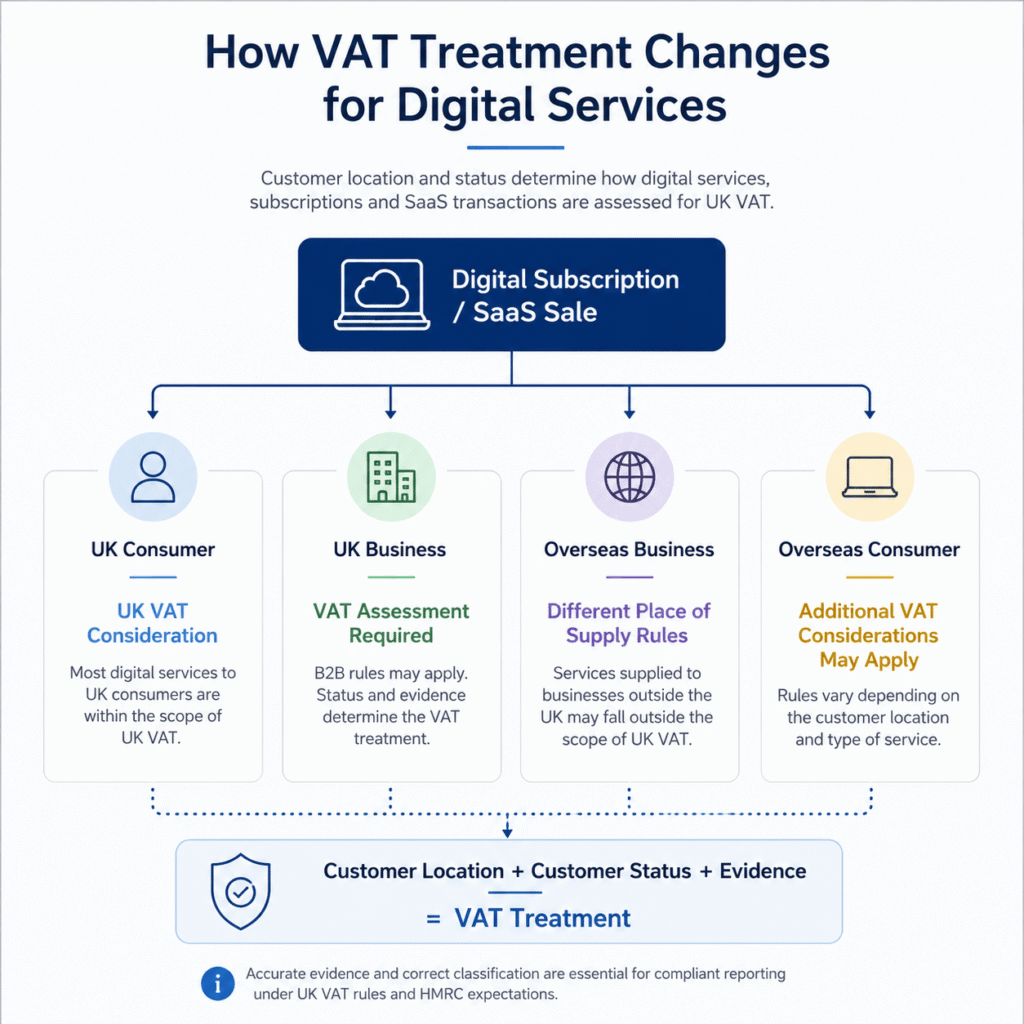

Why Customer Location Often Matters More Than Businesses Expect

One of the biggest conceptual adjustments for digital businesses is recognising that VAT is not always determined solely by where the supplier is based.

Many founders naturally assume that because their company operates from the UK, every sale should primarily be analysed through a UK VAT lens.

Digital services frequently require a broader perspective.

A UK business may have customers in:

- England;

- Scotland;

- Wales;

- Northern Ireland;

- Ireland;

- Germany;

- France;

- Spain;

- the United States;

- Canada;

- Australia;

- Singapore.

Commercially, those customers may all subscribe through the same checkout page.

From a VAT perspective, the analysis may differ significantly.

This is where customer onboarding processes become far more important than many businesses initially realise.

HMRC expects businesses to retain sufficient evidence supporting the VAT treatment adopted. During a compliance review, assumptions are considerably less persuasive than documented evidence.

A business may believe it knows where customers are located. The stronger question is whether it can demonstrate how that conclusion was reached if challenged several years later.

B2B and B2C Customers: Why Similar Transactions Can Produce Different VAT Outcomes

One of the most important distinctions in digital VAT is whether the customer is acting as a business or as a private consumer.

At first glance, the transaction may appear identical.

Two customers purchase the same software subscription. They select the same pricing plan. They access the same platform. They generate the same monthly revenue.

From a commercial perspective, they look identical.

From a VAT perspective, they may not be.

This distinction becomes particularly important when digital services are supplied across borders. In many situations, the VAT treatment depends not only on where the customer is located but also on whether that customer is purchasing in a business capacity.

One recurring issue encountered during VAT reviews is that businesses collect enough information to process a payment but not enough information to support the VAT treatment applied to the transaction.

When the business is small, this often goes unnoticed. As subscription revenue grows and international sales increase, weaknesses in customer classification become far more visible.

HMRC is generally less interested in how a customer was labelled internally and more interested in the evidence supporting that classification.

For businesses supplying digital services internationally, customer onboarding processes often need to capture:

- customer country;

- business name where relevant;

- VAT registration details;

- billing address information;

- supporting transaction evidence;

- additional indicators of customer status.

The objective is not administrative complexity. The objective is ensuring that the VAT treatment adopted can be supported if questioned later.

Customer Evidence: The Area Most Businesses Underestimate

If there is one area that consistently surprises business owners during VAT reviews, it is the importance of evidence.

Founders often know where they believe customers are located.

The challenge is demonstrating that conclusion several years later when records are reviewed.

HMRC generally expects businesses to maintain sufficient evidence supporting the VAT position adopted. This becomes particularly relevant where customer location influences how transactions are treated.

A recurring pattern during compliance reviews is that businesses rely heavily on assumptions that seemed reasonable at the time:

- the customer used a local payment card;

- the email address looked genuine;

- the customer selected a particular country during checkout;

- the platform appeared to capture location data automatically.

Unfortunately, assumptions can become difficult to defend if supporting records are incomplete.

Businesses are often surprised to discover that information available today may no longer be available several years later. Platform providers change reporting structures. Customer records are deleted. Systems are migrated. Historical data becomes harder to access.

By the time an issue becomes visible, reconstructing transaction evidence can be considerably more difficult than collecting it correctly at the point of sale.

Common forms of supporting evidence may include:

- billing addresses;

- customer declarations;

- VAT registration details;

- payment card information;

- IP address records;

- platform-generated reports;

- business registration information.

The precise evidence required depends on the circumstances, but the broader lesson remains consistent: customer location should be supported by records rather than assumptions.

Place of Supply Rules: The Question That Changes the Entire Analysis

Few areas of VAT generate more confusion than place of supply rules.

Few areas of VAT generate more confusion than place of supply rules.

In practice, they are often responsible for changing the answer to what initially appears to be a simple VAT question.

A founder may ask:

“Do I need to charge VAT on this subscription?”

The answer frequently depends on where the supply is treated as taking place.

This is why identical products can create different VAT outcomes depending on who purchases them and where those customers belong.

Consider a software company based in Manchester selling a £49 monthly subscription.

The software remains identical.

The checkout process remains identical.

The customer experience remains identical.

However, the VAT analysis may differ depending on whether the customer is:

- a UK consumer;

- a UK business;

- a company established in Germany;

- a private customer in France;

- a business customer in Australia;

- a company based in the United States.

This is one of the reasons international growth often exposes weaknesses that remain invisible while a business serves only domestic customers.

The business model may scale globally long before VAT processes are designed to support global transactions.

One observation frequently made during VAT reviews is that many businesses become international accidentally. Their marketing remains focused on the UK, yet customers begin subscribing from multiple countries simply because digital products are accessible globally.

The business grows internationally without intentionally building international compliance processes.

That disconnect is where many VAT challenges begin.

Brexit Did Not Eliminate VAT Considerations for EU Customers

Several years after Brexit, one misconception still appears regularly.

Some businesses assume that because the UK left the European Union, VAT considerations for EU customers largely disappeared.

The reality is considerably more nuanced.

Brexit altered the framework, but it did not remove the need to understand how digital supplies are treated when customers are located in EU countries.

In practice, many UK businesses continue acquiring EU customers without realising how quickly international VAT considerations can become relevant.

A software platform launched for UK customers may discover after twelve months that:

- 12% of users are located in Germany;

- 7% are located in France;

- 5% are located in Spain;

- additional customers are spread across multiple EU jurisdictions.

Commercially, this often feels like a success story.

From a compliance perspective, it introduces additional questions that may not have existed when the business first launched.

A recurring issue is that businesses frequently monitor customer acquisition metrics in extraordinary detail while paying very little attention to customer geography.

Marketing dashboards may provide precise conversion rates and acquisition costs. Yet management may struggle to produce a reliable breakdown of customer locations for VAT purposes.

As digital businesses scale internationally, customer geography becomes increasingly important from both a commercial and compliance perspective.

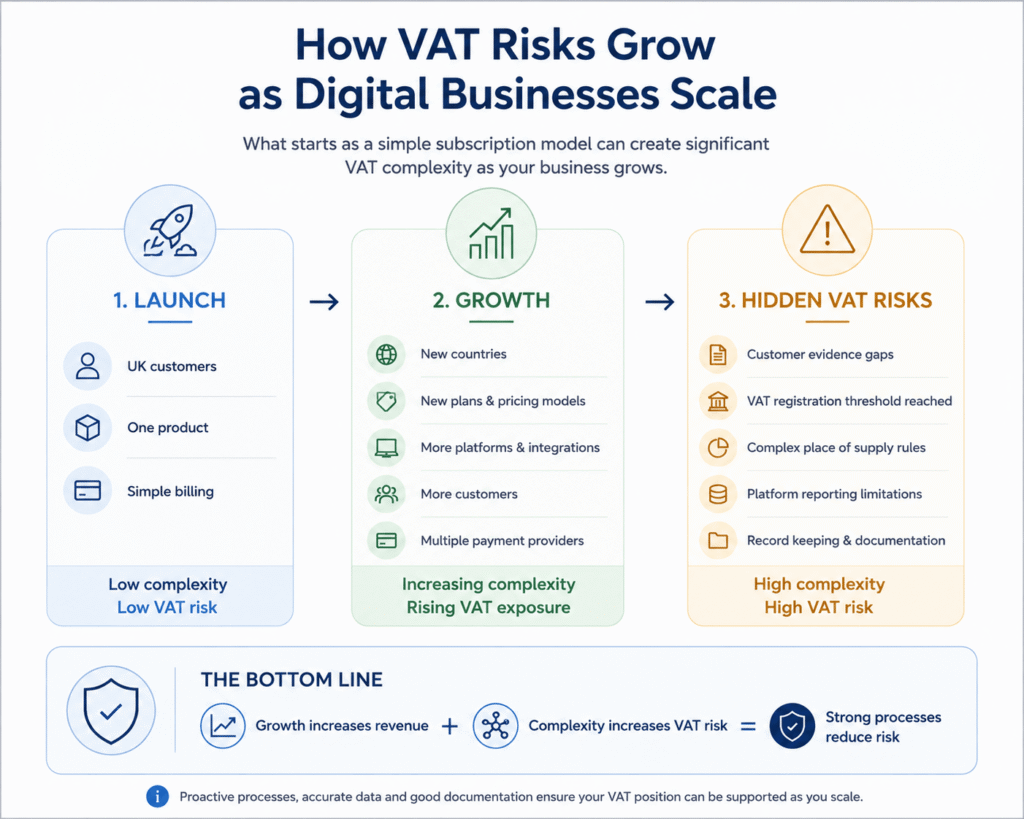

Why SaaS Businesses Frequently Encounter VAT Complexity Earlier Than Expected

SaaS companies occupy a particularly interesting position because several factors that drive growth also increase VAT complexity.

Many SaaS businesses:

- serve customers internationally from day one;

- operate entirely online;

- offer recurring subscriptions;

- provide multiple pricing tiers;

- combine software with support services;

- accept payments globally;

- serve both businesses and consumers.

Each of these characteristics can influence VAT treatment.

One pattern that frequently emerges is that product development moves faster than compliance processes.

A SaaS platform launches with one subscription plan.

Later it introduces:

- annual plans;

- enterprise packages;

- onboarding services;

- implementation support;

- premium consulting;

- training programmes;

- API usage fees.

Commercially, these additions make perfect sense.

From a VAT perspective, they can gradually alter the nature of the overall offering.

The difficulty is that tax treatment often remains based on assumptions created when the original product launched.

By the time somebody revisits those assumptions, thousands of transactions may already exist.

This is why periodic VAT reviews often identify issues that were not caused by mistakes in a traditional sense. The business simply evolved faster than the underlying compliance framework.

In many cases, founders are surprised to discover that the greatest VAT risks do not arise from complex legislation. They arise from perfectly reasonable operational decisions made during periods of rapid growth.

Membership Platforms and Online Communities: Where VAT Questions Become Less Obvious

Membership businesses frequently sit in one of the most misunderstood areas of digital VAT.

At first glance, the model appears straightforward. A customer pays a recurring fee and receives access to a platform.

The complexity usually emerges when somebody asks a simple question:

“What exactly is the customer paying for?”

Many membership platforms include far more than access to digital content.

A single subscription may provide:

- recorded educational materials;

- live training sessions;

- private communities;

- networking opportunities;

- downloadable resources;

- expert support;

- group coaching;

- software tools.

From the customer’s perspective, this is one product.

From a VAT perspective, understanding the principal nature of the supply may require a much deeper analysis.

One recurring issue seen during compliance reviews is that businesses continue describing themselves as “membership platforms” long after their offering has evolved into something significantly broader.

The label remains unchanged while the actual customer experience changes substantially.

HMRC is generally more interested in the substance of the arrangement than the marketing terminology used to describe it.

This is one reason businesses should periodically review not only how products are sold but also how they are delivered in practice.

Merchant of Record Models: One of the Most Common Areas of Confusion

The rise of global subscription platforms has made Merchant of Record models increasingly popular.

Many businesses view these arrangements as a solution to international tax complexity.

In some circumstances, they can significantly simplify administration.

However, one misconception appears repeatedly during VAT reviews:

“The platform handles payments, so the VAT issue is solved.”

Unfortunately, the situation is rarely that simple.

Businesses often use terms such as:

- payment processor;

- marketplace;

- reseller;

- Merchant of Record;

- billing platform.

As though they are interchangeable.

They are not.

One of the most expensive assumptions a digital business can make is believing that another party is responsible for VAT without fully understanding the contractual structure behind the transaction.

During compliance reviews, businesses are often surprised to discover that the platform they believed was handling VAT was performing a much narrower function.

A recurring warning sign appears when management cannot clearly answer questions such as:

- Who is the legal supplier?

- Who issues invoices?

- Who collects VAT?

- Who remits VAT?

- How are transactions reported?

- What documentation supports the accounting treatment?

If those questions produce uncertainty, additional review is often warranted.

The misunderstanding usually begins long before any VAT return is submitted. It begins when commercial assumptions are allowed to replace contractual analysis.

VAT Registration: Why Subscription Businesses Can Reach the Threshold Faster Than Expected

Subscription businesses often experience a different growth pattern from traditional businesses.

Revenue accumulates.

Each new customer contributes recurring income. Existing customers continue generating revenue month after month.

As a result, taxable turnover can increase gradually while remaining largely invisible from an operational perspective.

One observation that frequently emerges during VAT registration reviews is that founders monitor:

- monthly recurring revenue;

- customer acquisition costs;

- customer lifetime value;

- retention rates;

- churn percentages.

Yet many spend comparatively little time monitoring VAT registration exposure.

The result is that VAT registration obligations can arrive sooner than management expects.

Businesses are often surprised to discover that the operational impact of registration extends well beyond filing returns.

Registration may affect:

- pricing strategy;

- cash flow;

- customer communication;

- subscription profitability;

- invoicing procedures;

- reporting systems;

- financial forecasting.

One recurring pattern is that businesses treat VAT registration as a compliance milestone when, in reality, it often becomes a commercial milestone as well.

Businesses approaching registration thresholds frequently benefit from reviewing their position before decisions become urgent. This is particularly relevant where subscription pricing was originally developed without considering future VAT implications.

Pricing Decisions Can Create Long-Term VAT Problems

Few areas illustrate the connection between commercial decisions and VAT more clearly than pricing.

At launch, many digital businesses focus understandably on market penetration and customer acquisition.

Pricing is often designed to maximise adoption rather than optimise long-term tax efficiency.

That approach can work extremely well during the early stages of growth.

The difficulty emerges later.

One recurring issue seen during subscription business reviews is that pricing models were created before VAT registration was expected.

Years later, the business discovers that:

- customers expect existing pricing to continue;

- contracts limit pricing flexibility;

- competitive pressure restricts increases;

- profit margins are narrower than anticipated.

At that point, VAT becomes more than a reporting issue.

It becomes a margin issue.

This is why experienced advisers often view VAT as part of broader commercial planning rather than a standalone compliance exercise.

The strongest businesses tend to consider tax consequences alongside pricing strategy, growth planning and profitability objectives rather than treating each area separately.

VAT Number Verification: A Small Process With Large Consequences

For businesses supplying digital services internationally, VAT numbers often form part of the customer onboarding process.

What many businesses underestimate is how much reliance may eventually be placed on those records.

A VAT number entered during checkout can influence the VAT treatment applied to a transaction.

Yet one recurring problem is that businesses collect VAT numbers without implementing any meaningful validation process.

The assumption is simple:

“If the customer entered a VAT number, it must be correct.”

Unfortunately, VAT reviews frequently demonstrate otherwise.

Numbers may be:

- invalid;

- outdated;

- incorrectly entered;

- unrelated to the customer;

- unsupported by additional business evidence.

The issue may remain invisible for years.

However, if a VAT position depends on business customer status, weaknesses in verification procedures can become significantly more important.

This is one reason many growing digital businesses introduce VAT verification processes before transaction volumes become difficult to manage retrospectively.

Bookkeeping Problems Usually Appear Long Before VAT Problems

One of the most valuable observations from VAT reviews is that VAT issues rarely originate inside VAT returns.

They usually begin much earlier.

Most commonly, they begin inside bookkeeping systems.

Subscription businesses generate large volumes of recurring transactions. As volumes increase, there is often pressure to simplify reporting.

Revenue may be imported as summary totals. Platform reports may be aggregated. International transactions may be grouped together.

Initially, this appears efficient.

Over time, however, transaction visibility often deteriorates.

A single revenue figure may conceal:

- UK consumer sales;

- UK business sales;

- EU customer subscriptions;

- international B2B supplies;

- refunds;

- chargebacks;

- discounts;

- platform fees;

- marketplace transactions.

The challenge is not bookkeeping complexity itself.

The challenge is ensuring that financial records continue reflecting commercial reality.

One of the most common discoveries during compliance reviews is that management possesses excellent visibility over sales performance but limited visibility over how individual transactions are classified within financial records.

That disconnect can eventually affect VAT reporting, management accounts and wider financial reporting processes.

Making Tax Digital: Why Digital Records Matter More Than Software

Many discussions around Making Tax Digital focus primarily on software.

In practice, software is only part of the picture.

The strongest MTD frameworks are built on reliable records rather than software alone.

For subscription businesses, the challenge often involves connecting multiple systems:

- billing platforms;

- payment gateways;

- subscription management systems;

- accounting software;

- reporting tools.

A recurring misconception is that adopting compatible software automatically solves compliance concerns.

In reality, poor-quality data flows through software just as efficiently as good-quality data.

One pattern frequently encountered during VAT reviews is that businesses have invested heavily in technology while paying relatively little attention to how data moves between systems.

By the time discrepancies appear, identifying the original source can be surprisingly difficult.

Strong MTD compliance generally relies upon:

- accurate transaction categorisation;

- consistent record keeping;

- clear audit trails;

- reliable reconciliations;

- documented VAT policies;

- effective internal controls.

Technology supports compliance. It does not replace it.

The Most Common VAT Mistakes Subscription Businesses Make

Despite the variety of digital business models, the same VAT mistakes appear repeatedly.

The products may differ. The industries may differ. The technology stacks may differ.

The underlying compliance failures are often remarkably similar.

Treating Every Customer the Same

One of the most common issues is applying a single VAT assumption to an increasingly diverse customer base.

What began as a UK-focused subscription business may gradually acquire:

- international consumers;

- EU businesses;

- US companies;

- enterprise customers;

- reseller arrangements.

The business evolves while the VAT treatment remains unchanged.

During compliance reviews, this is frequently one of the first areas examined because customer classification often influences multiple aspects of VAT treatment simultaneously.

Assuming Technology Solves Compliance Automatically

Modern platforms automate many tasks.

However, automation should never be confused with accountability.

A recurring misconception is that because a system can calculate VAT, the underlying VAT treatment must automatically be correct.

In reality, technology relies on assumptions, configurations and data quality.

If those assumptions are incorrect, automation can scale mistakes just as efficiently as it scales good processes.

Collecting Information Without Verifying It

Businesses frequently collect customer data but rarely review its reliability.

VAT numbers are gathered.

Addresses are entered.

Countries are selected.

The information is stored.

Yet no meaningful validation process exists.

By the time weaknesses become visible, large volumes of transactions may already depend upon that information.

Viewing VAT as a Reporting Exercise

Perhaps the most important mistake is treating VAT as something that happens at quarter end.

In reality, VAT decisions are often made long before returns are submitted.

They are made when:

- products are designed;

- customers are onboarded;

- platforms are selected;

- pricing models are created;

- transactions are recorded.

VAT returns simply reflect those earlier decisions.

When problems emerge, they usually originate upstream.

Real-World Scenario: The Growing SaaS Company

Consider a SaaS business that launches with a single subscription plan aimed at UK companies.

The VAT treatment appears straightforward.

After eighteen months, the business has:

- customers across Europe;

- customers in North America;

- multiple pricing tiers;

- enterprise contracts;

- annual subscriptions;

- implementation services;

- premium support packages.

Commercially, the business has been successful.

Operationally, the environment has changed completely.

One observation that frequently emerges in situations like this is that compliance processes often remain remarkably similar to those used on the day the business launched.

The business has become significantly more sophisticated.

The underlying VAT framework has not.

This is rarely caused by negligence.

More often, growth simply happens faster than internal processes evolve.

Real-World Scenario: The Membership Platform

A membership platform launches with recorded educational content.

Over time it adds:

- live workshops;

- community access;

- private coaching;

- downloadable resources;

- expert support sessions.

Each addition improves the customer experience.

Each addition strengthens retention.

Each addition increases perceived value.

Yet each addition may also influence the nature of the supply.

One recurring lesson from these situations is that product evolution and VAT analysis should not be treated as separate conversations.

The more a digital product changes, the more important it becomes to revisit assumptions that may have been entirely appropriate several years earlier.

Operational Risks That Typically Appear During Growth

Digital businesses rarely encounter VAT difficulties because somebody deliberately ignored compliance obligations.

Far more commonly, problems emerge because operational growth outpaces internal visibility.

Warning signs often include:

- rapid international expansion;

- multiple payment providers;

- new subscription models;

- additional currencies;

- marketplace sales;

- platform migrations;

- incomplete documentation;

- inconsistent reporting procedures.

Individually, none of these developments are unusual.

Together, they can create a level of complexity that did not exist when the original VAT framework was established.

Businesses are often surprised to discover that VAT risks tend to accumulate gradually rather than appearing suddenly.

By the time a problem becomes obvious, its underlying causes may have existed for years.

Why VAT and Corporation Tax Records Must Tell the Same Story

VAT and Corporation Tax operate under different rules, but both rely on accurate financial information.

Where transaction records are inconsistent, the effects often extend beyond VAT reporting.

Weaknesses may influence:

- management accounts;

- revenue reporting;

- profitability analysis;

- forecasting decisions;

- year-end accounts preparation;

- Corporation Tax calculations.

One pattern frequently observed during financial reviews is that businesses maintain excellent commercial reporting while the accounting records supporting those reports contain significantly less detail.

The stronger the alignment between operational systems, bookkeeping records and tax reporting, the easier it becomes to support compliance decisions across multiple areas simultaneously.

This is one reason VAT should rarely be viewed in isolation from wider financial reporting and Corporation Tax considerations.

What a Strong VAT Framework Looks Like

The strongest subscription businesses rarely rely on individual VAT decisions.

Instead, they develop repeatable processes capable of supporting growth.

While every business is different, effective frameworks often include the following components.

Product Mapping

Clearly documenting what is supplied, how it is delivered and how individual offerings relate to one another.

Customer Classification

Understanding who customers are, where they are located and whether they are acting in a business or consumer capacity.

Evidence Collection

Retaining records capable of supporting VAT treatment decisions long after transactions occur.

Platform Governance

Understanding the responsibilities of payment processors, marketplaces and Merchant of Record providers.

Financial Integration

Ensuring accounting systems reflect the commercial reality of transactions rather than simplified summaries.

Periodic Review

Reassessing VAT assumptions as products, customers and markets evolve.

Reliable Reporting Processes

Producing VAT returns from structured records rather than attempting to reconstruct information retrospectively.

The businesses that experience the fewest VAT difficulties are rarely those with the most complex software. More often, they are the businesses with the clearest processes.

Questions Business Owners Should Ask Before Scaling Further

As subscription revenue grows, management should periodically revisit several practical questions.

- Do we still understand the nature of every product we supply?

- Can we clearly identify business and consumer customers?

- Do we know where customers are located?

- Can we support that conclusion with evidence?

- Have our products changed since the original VAT assessment?

- Do our platforms perform the functions we believe they perform?

- Can our bookkeeping records support VAT reporting decisions?

- Would an external reviewer understand our VAT treatment from the records available?

- Have international sales altered our compliance exposure?

- Are our reporting processes capable of supporting continued growth?

These questions become increasingly valuable as businesses move beyond the startup phase and begin operating at greater scale.

Key Takeaways

Subscriptions are not a VAT category. They are a payment model.

Digital services are not automatically simple from a VAT perspective simply because they are delivered online.

The VAT treatment of subscriptions and digital services depends on factors such as:

- the nature of the supply;

- customer status;

- customer location;

- place of supply considerations;

- platform arrangements;

- evidence quality;

- record-keeping processes.

Businesses that address these areas early generally find it easier to support sustainable growth without creating avoidable compliance challenges later.

Most importantly, VAT should not be viewed as a quarterly reporting exercise. It is an operational framework that begins with product design and continues through customer onboarding, billing, bookkeeping and reporting.

Final Expert Perspective

The digital economy has fundamentally changed how businesses generate revenue.

Software subscriptions, memberships, online education platforms and recurring digital services have created opportunities that were almost unimaginable a generation ago.

At the same time, they have introduced compliance considerations that traditional business models rarely faced.

One of the clearest observations from years of VAT reviews is that the most significant problems rarely arise because legislation is exceptionally complicated.

More often, they arise because commercial growth moves faster than the systems designed to support it.

The strongest businesses recognise that VAT is not merely an accounting obligation.

It is part of the infrastructure that supports scalable growth.

When customer onboarding, transaction records, subscription platforms, bookkeeping systems and reporting procedures operate together coherently, VAT compliance becomes significantly easier to manage.

When those elements evolve independently, complexity accumulates quietly until somebody eventually asks questions the records cannot answer.

For UK businesses operating subscription models, SaaS platforms, membership communities and other digital service offerings, understanding VAT is ultimately about more than avoiding mistakes.

It is about ensuring that growth is supported by a framework capable of keeping pace with the business itself.